Question: Question 3 - VaR Simulation (5 Marks) A Financial Institution has written 20 European Call Options on one stock and 45 European Put Options

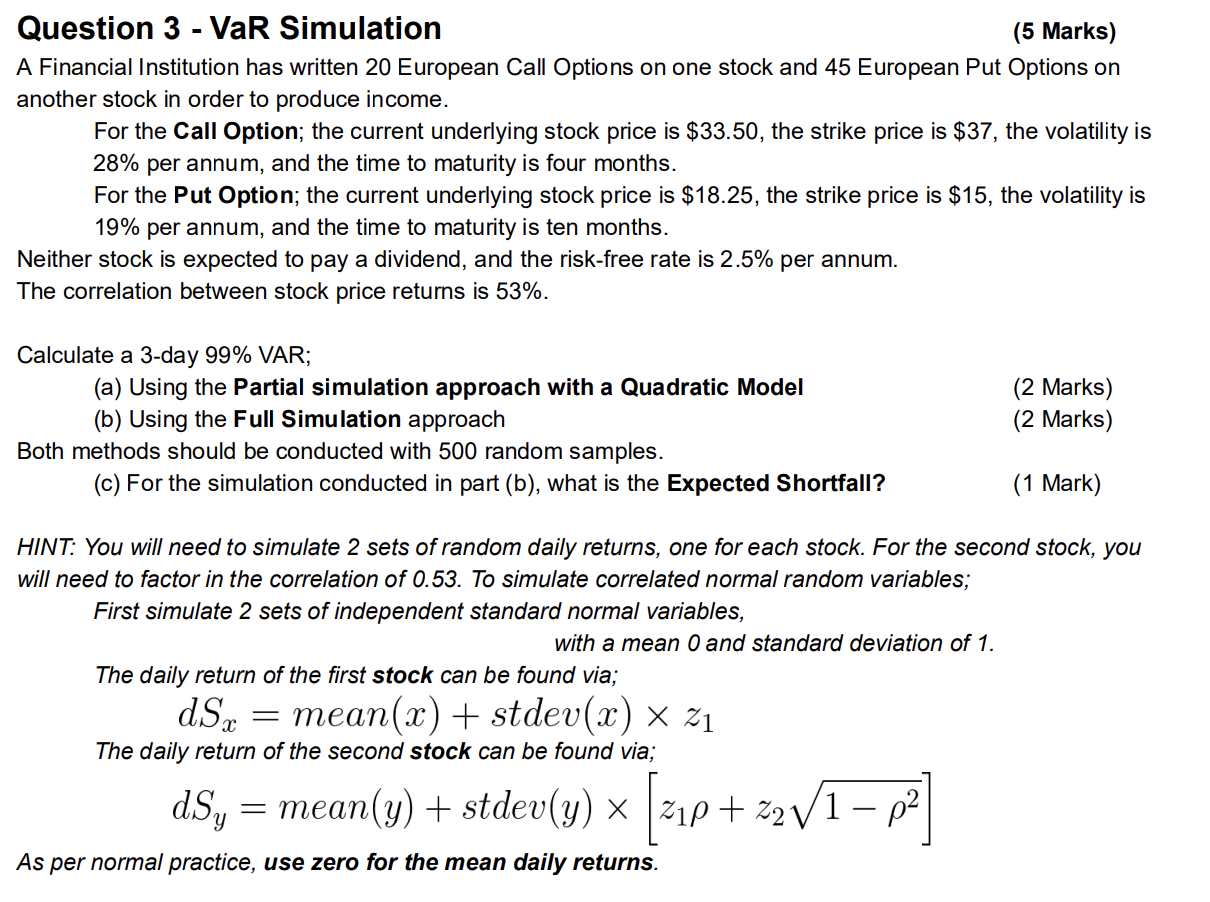

Question 3 - VaR Simulation (5 Marks) A Financial Institution has written 20 European Call Options on one stock and 45 European Put Options on another stock in order to produce income. For the Call Option; the current underlying stock price is $33.50, the strike price is $37, the volatility is 28% per annum, and the time to maturity is four months. For the Put Option; the current underlying stock price is $18.25, the strike price is $15, the volatility is 19% per annum, and the time to maturity is ten months. Neither stock is expected to pay a dividend, and the risk-free rate is 2.5% per annum. The correlation between stock price returns is 53%. Calculate a 3-day 99% VAR; (a) Using the Partial simulation approach with a Quadratic Model (b) Using the Full Simulation approach Both methods should be conducted with 500 random samples. (c) For the simulation conducted in part (b), what is the Expected Shortfall? (2 Marks) (2 Marks) (1 Mark) HINT: You will need to simulate 2 sets of random daily returns, one for each stock. For the second stock, you will need to factor in the correlation of 0.53. To simulate correlated normal random variables; First simulate 2 sets of independent standard normal variables, with a mean 0 and standard deviation of 1. The daily return of the first stock can be found via; dSx mean(x) + stdev(x) Z1 = The daily return of the second stock can be found via; dSy = mean(y) + stdev(y) 1p+Z2V [zip + z 2 1 = p] As per normal practice, use zero for the mean daily returns.

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts