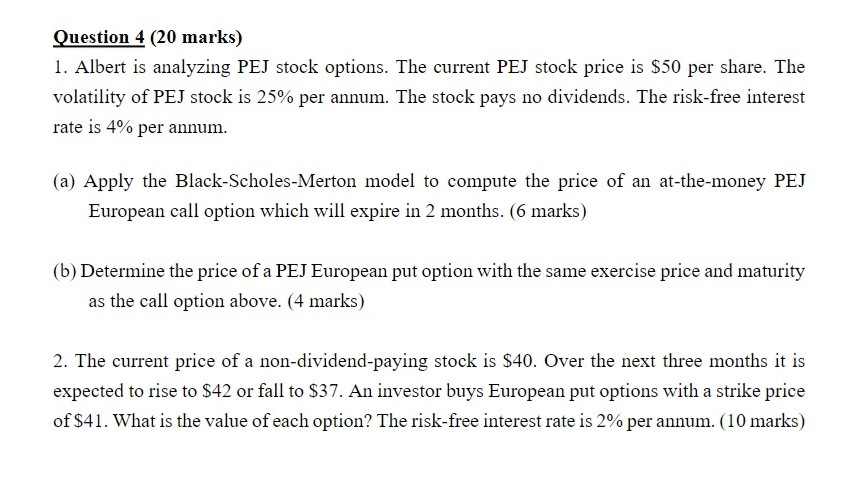

Question: Question 4 (20 marks) 1. Albert is analyzing PEJ stock options. The current PEJ stock price is $50 per share. The volatility of PEJ stock

Question 4 (20 marks) 1. Albert is analyzing PEJ stock options. The current PEJ stock price is $50 per share. The volatility of PEJ stock is 25% per annum. The stock pays no dividends. The risk-free interest rate is 4% per annum. (a) Apply the Black-Scholes-Merton model to compute the price of an at-the-money PEJ European call option which will expire in 2 months. (6 marks) (b) Determine the price of a PEJ European put option with the same exercise price and maturity as the call option above. (4 marks) 2. The current price of a non-dividend-paying stock is $40. Over the next three months it is expected to rise to $42 or fall to $37. An investor buys European put options with a strike price of $41. What is the value of each option? The risk-free interest rate is 2% per annum. (10 marks)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts