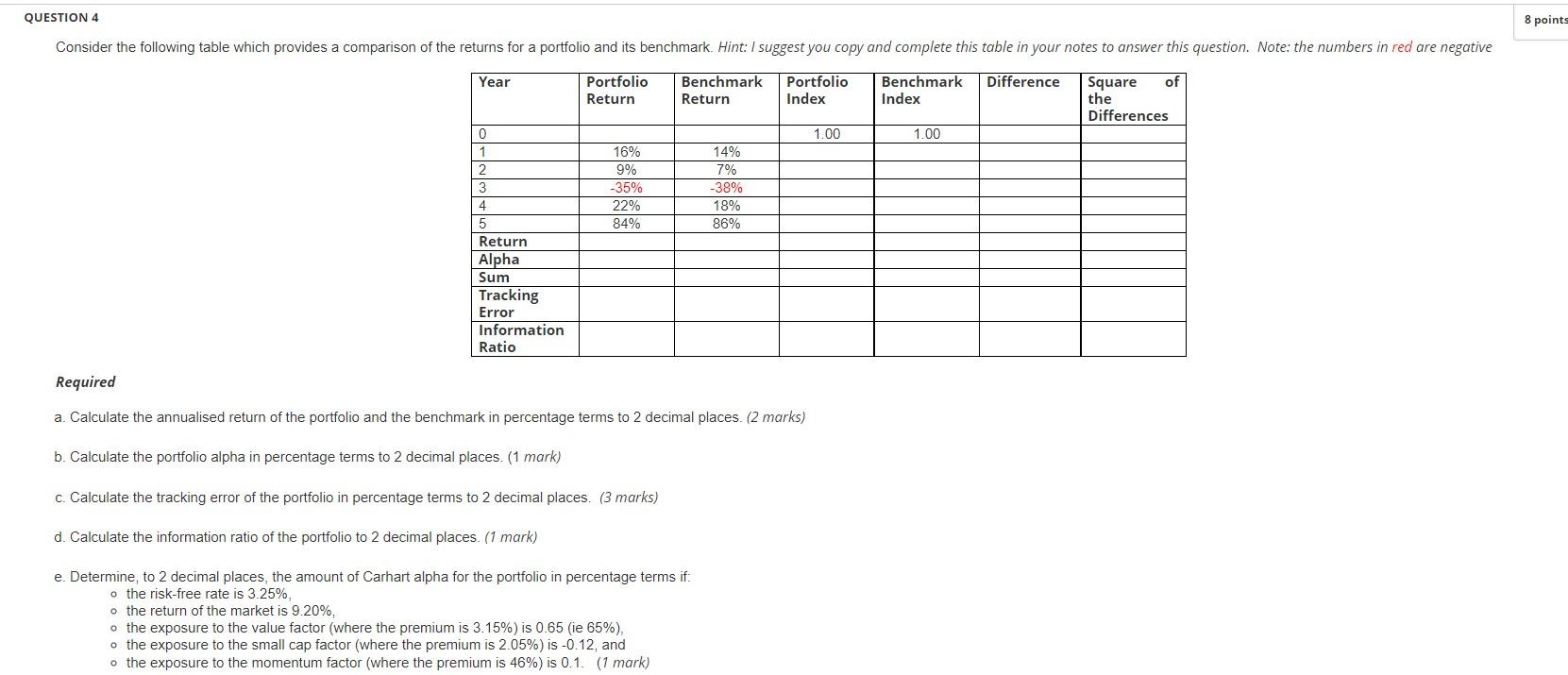

Question: QUESTION 4 Consider the following table which provides a comparison of the returns for a portfolio and its benchmark. Hint: I suggest you copy and

QUESTION 4 Consider the following table which provides a comparison of the returns for a portfolio and its benchmark. Hint: I suggest you copy and complete this table in your notes to answer this question. Note: the numbers in red are negative of Benchmark Portfolio Return Index Benchmark Difference Index Square the Differences Year 0 1 2 3 4 5 Return Alpha Sum Tracking Error Information Ratio Portfolio Return 16% 9% -35% 22% 84% 14% 7% -38% 18% 86% Required a. Calculate the annualised return of the portfolio and the benchmark in percentage terms to 2 decimal places. (2 marks) b. Calculate the portfolio alpha in percentage terms to 2 decimal places. (1 mark) c. Calculate the tracking error of the portfolio in percentage terms to 2 decimal places. (3 marks) d. Calculate the information ratio of the portfolio to 2 decimal places. (1 mark) e. Determine, to 2 decimal places, the amount of Carhart alpha for the portfolio in percentage terms if: o the risk-free rate is 3.25%, o the return of the market is 9.20%, o the exposure to the value factor (where the premium is 3.15%) is 0.65 (ie 65%), o the exposure to the small cap factor (where the premium is 2.05%) is -0.12, and o the exposure to the momentum factor (where the premium is 46%) is 0.1. (1 mark) 1.00 1.00 8 points QUESTION 4 Consider the following table which provides a comparison of the returns for a portfolio and its benchmark. Hint: I suggest you copy and complete this table in your notes to answer this question. Note: the numbers in red are negative of Benchmark Portfolio Return Index Benchmark Difference Index Square the Differences Year 0 1 2 3 4 5 Return Alpha Sum Tracking Error Information Ratio Portfolio Return 16% 9% -35% 22% 84% 14% 7% -38% 18% 86% Required a. Calculate the annualised return of the portfolio and the benchmark in percentage terms to 2 decimal places. (2 marks) b. Calculate the portfolio alpha in percentage terms to 2 decimal places. (1 mark) c. Calculate the tracking error of the portfolio in percentage terms to 2 decimal places. (3 marks) d. Calculate the information ratio of the portfolio to 2 decimal places. (1 mark) e. Determine, to 2 decimal places, the amount of Carhart alpha for the portfolio in percentage terms if: o the risk-free rate is 3.25%, o the return of the market is 9.20%, o the exposure to the value factor (where the premium is 3.15%) is 0.65 (ie 65%), o the exposure to the small cap factor (where the premium is 2.05%) is -0.12, and o the exposure to the momentum factor (where the premium is 46%) is 0.1. (1 mark) 1.00 1.00 8 points

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts