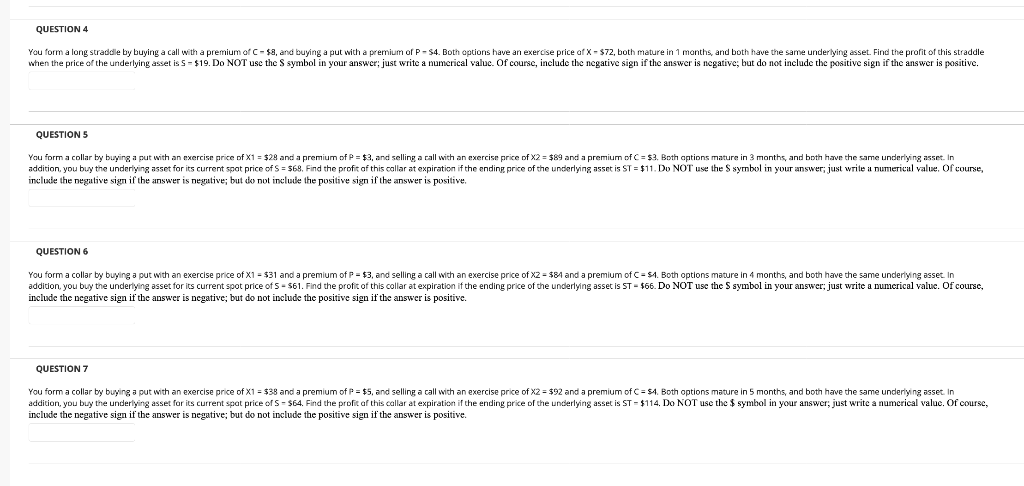

Question: QUESTION 4 You form a long straddle by buying a call with a premium of C- $, and buying a put with a premium of

QUESTION 4 You form a long straddle by buying a call with a premium of C- $, and buying a put with a premium of P-54. Both options have an exercise price of X - $72, both mature in 1 months and both have the same underlying asset. Find the profit of this straddle when the price of the underlying asset is S - $19. Do NOT use the symbol in your answer; just write a numerical value. Of course, include the negative sign if the answer is negative, but do not include the positive sign if the answer is positive. QUESTIONS You form a collar by buying a put with an exercise price of X1 = $29 and a premium of P = $3, and selling a call with an exercise price of X2 = $89 and a premium of C = $3. Both options mature in 3 months, and both have the same underlying asset. In addition, you buy the underlying asset for its current spat price of S = $68. Find the profit of this callar at expiration if the ending price of the underlying asset is ST = $11. Do NOT use the symbol in your answer; just write a numerical value. Of course, include the negative sign if the answer is negative; but do not include the positive sign if the answer is positive QUESTION 6 You form a collar by buying a put with an exercise price of X1 = $31 and a premium of P = $3, and selling a call with an exercise price of x2 = $81 and a premium of C = 51. Both options mature in 4 months and both have the same underlying asset. In addition, you buy the underlying asset for its current spot price of 5 - $61. Find the profit of this collar at expiration if the ending price of the underlying asset is ST - $66. Do NOT use the symbol in your answer; just write a numerical value. Of course, include the negative sign if the answer is negative; but do not include the positive sign if the answer is positive. QUESTION 7 You form a collar by buying a put with an exercise price of x1 = $38 and a premium of P = $5, and selling a call with an exercise price of x2 = $92 and a premium of C = 54. Both options mature in 5 months and both have the same underlying asset. In addition, you buy the underlying asset for its current spat price of S - $64. Find the profit of this callar at expiration if the ending price of the underlying asset is ST - $114. Do NOT use the $ symbol in your answer, just write a numerical value. Of course, include the negative sign if the answer is negative; but do not include the positive sign if the answer is positive

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts