Question: Question 4(30 marks) a) Explain how to construct a swap using a floating-rate bond and a fixed-rate bond. b) Consider the swap as in

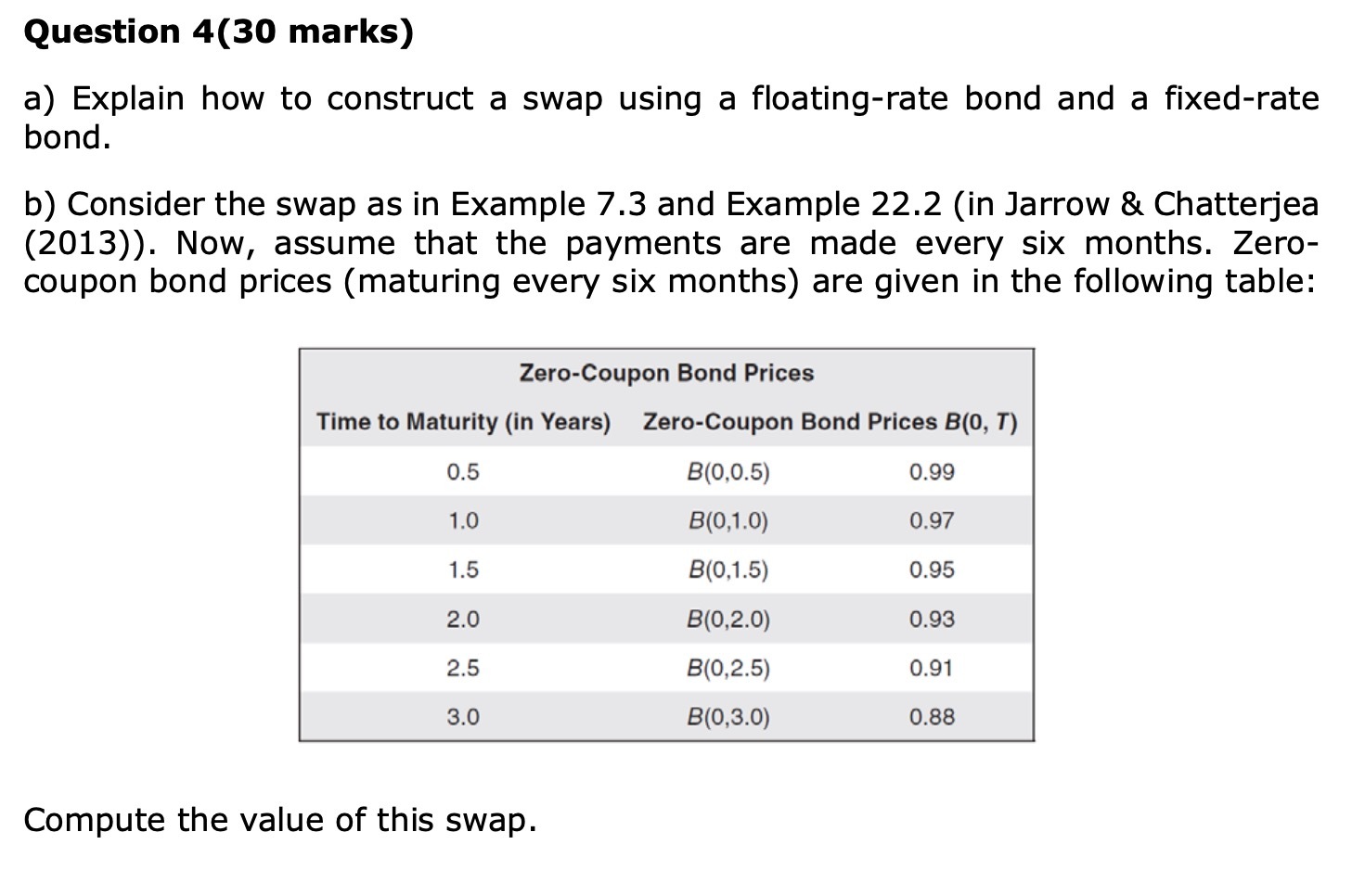

Question 4(30 marks) a) Explain how to construct a swap using a floating-rate bond and a fixed-rate bond. b) Consider the swap as in Example 7.3 and Example 22.2 (in Jarrow & Chatterjea (2013)). Now, assume that the payments are made every six months. Zero- coupon bond prices (maturing every six months) are given in the following table: Zero-Coupon Bond Prices Time to Maturity (in Years) Zero-Coupon Bond Prices B(0, T) 0.5 B(0,0.5) 0.99 1.0 B(0,1.0) 0.97 1.5 B(0,1.5) 0.95 2.0 B(0,2.0) 0.93 2.5 B(0,2.5) 0.91 3.0 B(0,3.0) 0.88 Compute the value of this swap.

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock