Question: Question 5 (25 marks) The table below illustrates the performance of returns of three (3) funds managed by three (3) different fund managers. The

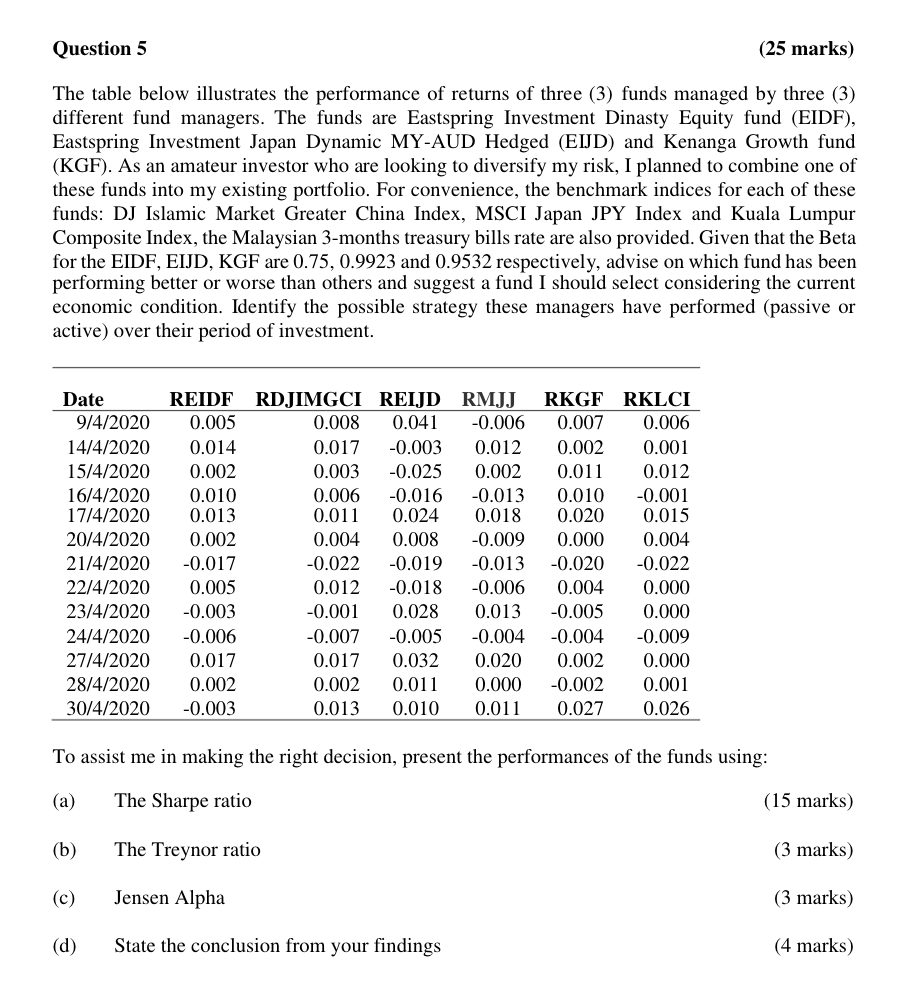

Question 5 (25 marks) The table below illustrates the performance of returns of three (3) funds managed by three (3) different fund managers. The funds are Eastspring Investment Dinasty Equity fund (EIDF), Eastspring Investment Japan Dynamic MY-AUD Hedged (EIJD) and Kenanga Growth fund (KGF). As an amateur investor who are looking to diversify my risk, I planned to combine one of these funds into my existing portfolio. For convenience, the benchmark indices for each of these funds: DJ Islamic Market Greater China Index, MSCI Japan JPY Index and Kuala Lumpur Composite Index, the Malaysian 3-months treasury bills rate are also provided. Given that the Beta for the EIDF, EIJD, KGF are 0.75, 0.9923 and 0.9532 respectively, advise on which fund has been performing better or worse than others and suggest a fund I should select considering the current economic condition. Identify the possible strategy these managers have performed (passive or active) over their period of investment. Date REIDF RDJIMGCI 0.005 9/4/2020 14/4/2020 0.014 15/4/2020 0.002 16/4/2020 0.010 17/4/2020 0.013 20/4/2020 0.002 21/4/2020 -0.017 22/4/2020 0.005 23/4/2020 -0.003 24/4/2020 -0.006 27/4/2020 0.017 28/4/2020 0.002 30/4/2020 -0.003 REIJD RMJJ RKGF RKLCI 0.041 -0.006 0.007 0.008 0.006 0.017 -0.003 0.012 0.002 0.001 0.002 0.011 0.012 -0.001 0.015 0.003 -0.025 0.006 -0.016 0.011 0.024 0.004 0.008 -0.009 -0.022 0.012 -0.018 -0.001 0.004 -0.019 -0.013 -0.020 -0.022 -0.006 0.004 0.028 0.013 -0.005 -0.013 0.010 0.018 0.020 0.000 -0.007 -0.004 -0.004 -0.005 0.017 0.032 0.020 0.002 0.002 0.011 0.000 -0.002 0.013 0.010 0.011 0.027 The Treynor ratio Jensen Alpha State the conclusion from your findings 0.000 0.000 -0.009 0.000 0.001 0.026 To assist me in making the right decision, present the performances of the funds using: (a) The Sharpe ratio (b) (c) (d) (15 marks) (3 marks) (3 marks) (4 marks)

Step by Step Solution

3.37 Rating (150 Votes )

There are 3 Steps involved in it

Here is my analysis of the three funds based on their performances a Sharpe Ratio The Sharpe Ratio measures the excess return per unit of risk in an investment asset or a trading strategy A higher Sha... View full answer

Get step-by-step solutions from verified subject matter experts