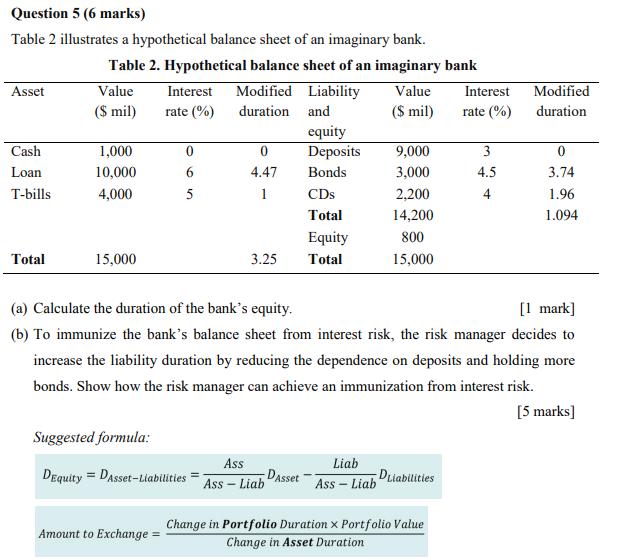

Question: Question 5 (6 marks) Table 2 illustrates a hypothetical balance sheet of an imaginary bank. Asset Cash Loan T-bills Total Table 2. Hypothetical balance

Question 5 (6 marks) Table 2 illustrates a hypothetical balance sheet of an imaginary bank. Asset Cash Loan T-bills Total Table 2. Hypothetical balance sheet of an imaginary bank Value ($ mil) 1,000 10,000 4,000 15,000 Interest rate (%) 0 6 5 Amount to Exchange = Suggested formula: DEquity = DAsset-Liabilities Modified Liability duration and equity Deposits Bonds CDs Total Equity Total 0 4.47 1 3.25 Ass Ass-Liab DAsset Value ($ mil) Liab Ass-Liab 9,000 3,000 2,200 14,200 800 15,000 (a) Calculate the duration of the bank's equity. [1 mark] (b) To immunize the bank's balance sheet from interest risk, the risk manager decides to increase the liability duration by reducing the dependence on deposits and holding more bonds. Show how the risk manager can achieve an immunization from interest risk. [5 marks] DLiabilities Interest rate (%) Change in Portfolio Duration x Portfolio Value Change in Asset Duration 3 4.5 4 Modified duration 0 3.74 1.96 1.094

Step by Step Solution

There are 3 Steps involved in it

The image you provided contains a table illustrating a hypothetical balance sheet of an imaginary bank and a question associated with this data There are two parts to the question Lets address them on... View full answer

Get step-by-step solutions from verified subject matter experts