Question: Question 5 : efficient frontier Referencing the cells in the diversification sheet, enter the expected return and standard deviation for WMT and CVX in B

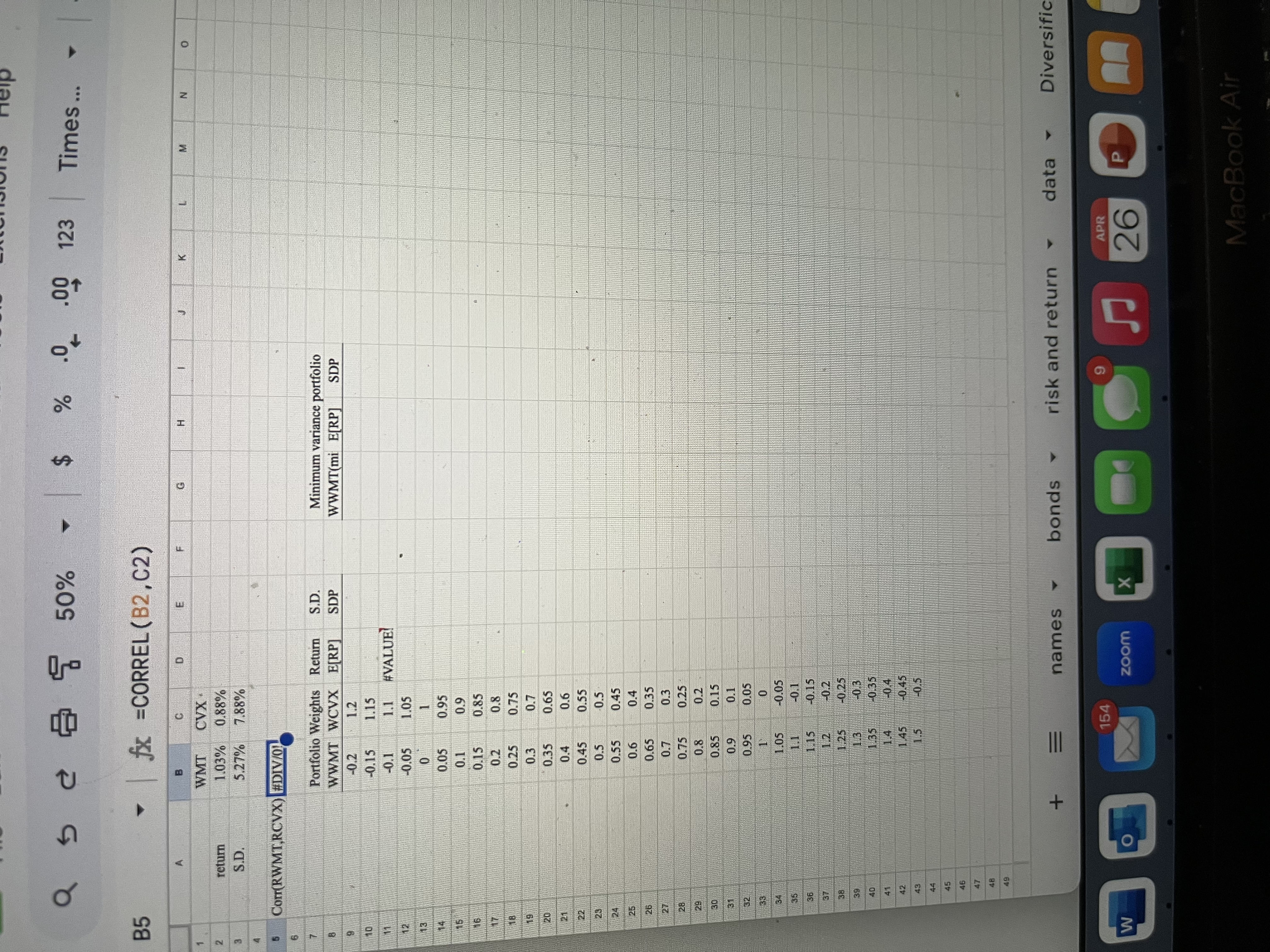

Question : efficient frontier Referencing the cells in the "diversification" sheet, enter the expected return and standard deviation for WMT and CVX in B:C and the correlation between them in BConstruct twoasset portfolios with different weights in WMT and CVX Calculate the returns and standard deviations of each possible portfolio in D:In a "Scatter with Smooth Lines" chart, plot the investment opportunity set. Make sure the y values are the returns and the x values are the standard deviations. Your figure should look somewhat like Figure in Section of the textbook. Here's how to create a scatter chart.Find the minimum variance portfolio using the formula in B of SpreadSheet in Section of the textbook. Enter the portfolio weight for WMT the expected return and the standard deviation of the minimum variance portfolio in G:

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock