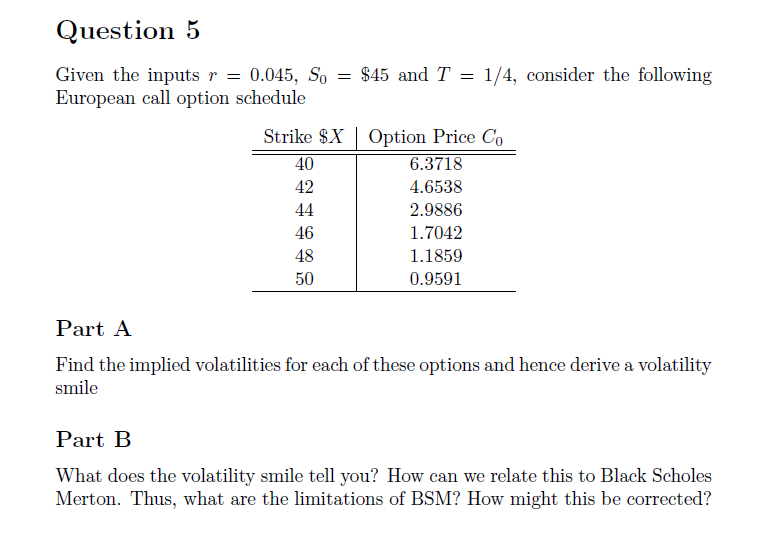

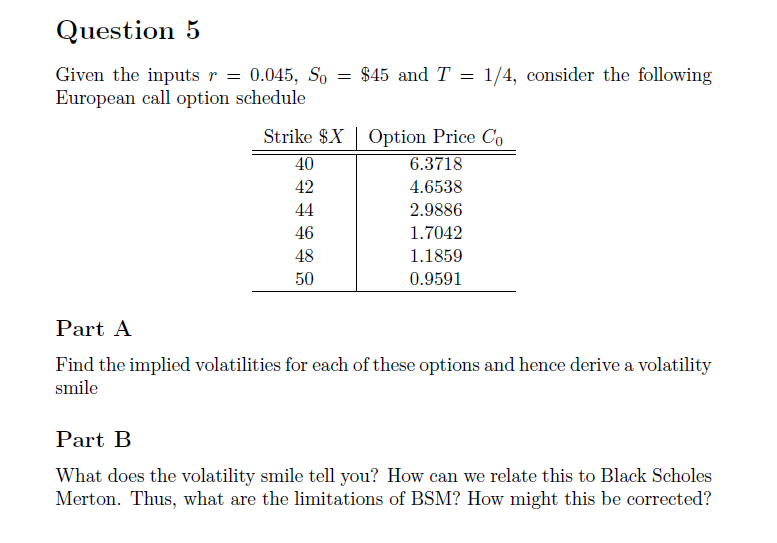

Question: Question 5 Given the inputs r = 0.045, So = $45 and T = 1/4, consider the following European call option schedule Strike $X |Option

Question 5 Given the inputs r = 0.045, So = $45 and T = 1/4, consider the following European call option schedule Strike $X |Option Price Co 40 6.3718 42 4.6538 44 2.9886 46 1.7042 48 1.1859 50 0.9591 Part A Find the implied volatilities for each of these options and hence derive a volatility smile Part B What does the volatility smile tell you? How can we relate this to Black Scholes Merton. Thus, what are the limitations of BSM? How might this be corrected

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock