Question: Question 5. Problem Solving I In a hypothetical world of a risk-free asset Rf and three risky assets A, B, and C. Suppose the CAPM

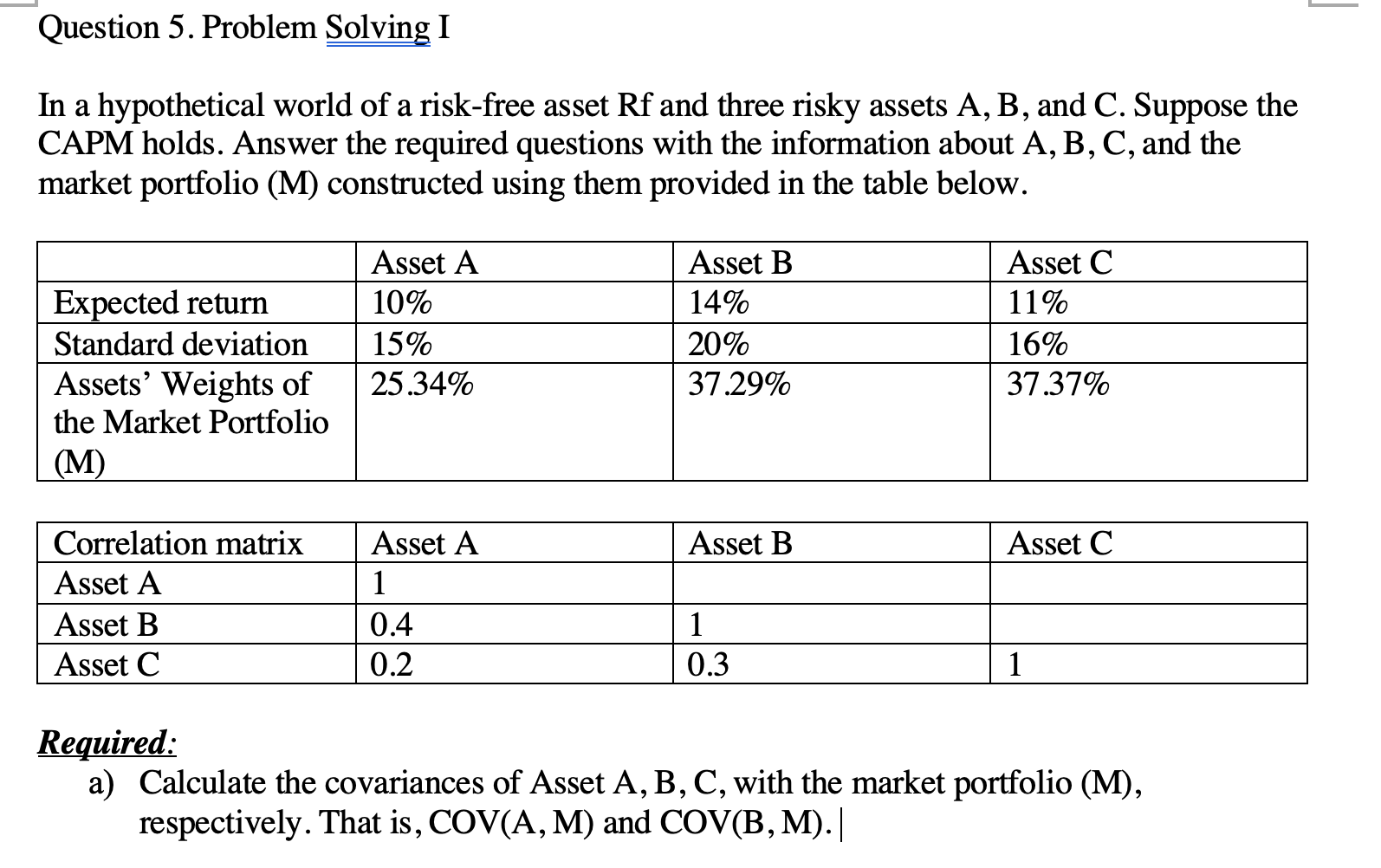

Question 5. Problem Solving I In a hypothetical world of a risk-free asset Rf and three risky assets A, B, and C. Suppose the CAPM holds. Answer the required questions with the information about A, B, C, and the market portfolio (M) constructed using them provided in the table below. - Expected return Standard deviation Assets' Weights of the Market Portfolio (M) Asset A 10% 15% 25.34% Asset B 14% 20% 37.29% Asset C 11% 16% 37.37% Asset B Asset C Correlation matrix Asset A Asset B Asset C Asset A 1 0.4 0.2 1 0.3 1 Required: a) Calculate the covariances of Asset A, B, C, with the market portfolio (M), respectively. That is, COV(A, M) and COV(B,M). >

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts