Question: Question #51 (10 points) Use a two-step binomial model to evaluate a call option on a stock with the following price projections. The current stock

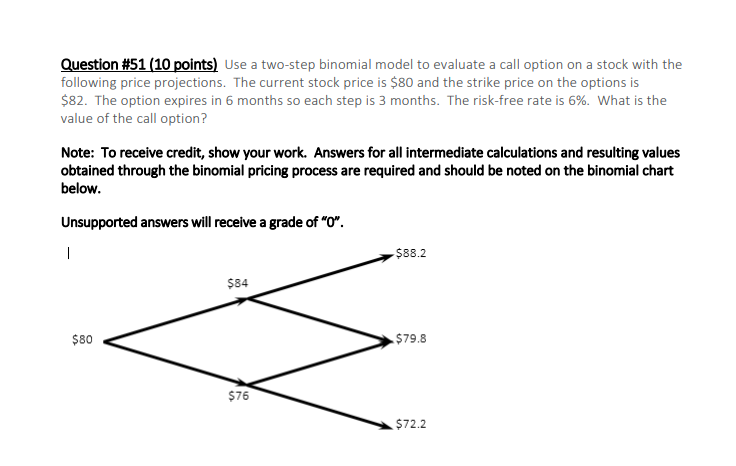

Question #51 (10 points) Use a two-step binomial model to evaluate a call option on a stock with the following price projections. The current stock price is $80 and the strike price on the options is $82. The option expires in 6 months so each step is 3 months. The risk-free rate is 6%. What is the value of the call option? Note: To receive credit, show your work. Answers for all intermediate calculations and resulting values obtained through the binomial pricing process are required and should be noted on the binomial chart below. Unsupported answers will receive a grade of "o". 1 $88.2 $84 $80 $79.8 $76 $72.2

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock