Question: Use a two-step binomial model to evaluate a call option on a stock with the following price projections. The current stock price is $80 and

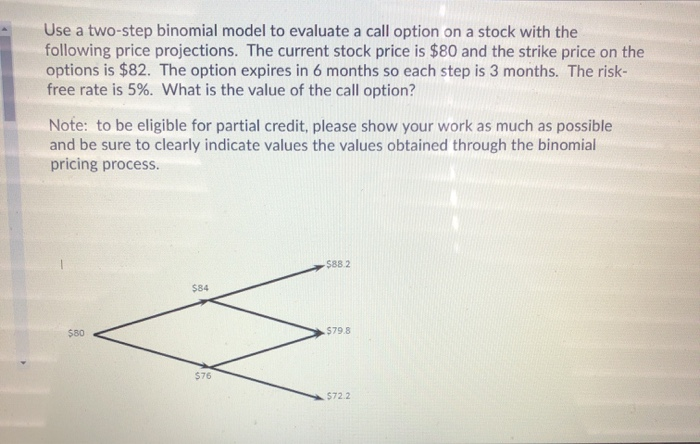

Use a two-step binomial model to evaluate a call option on a stock with the following price projections. The current stock price is $80 and the strike price on the options is $82. The option expires in 6 months so each step is 3 months. The risk- free rate is 5%. What is the value of the call option? Note: to be eligible for partial credit, please show your work as much as possible and be sure to clearly indicate values the values obtained through the binomial pricing process. $882 $80

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock