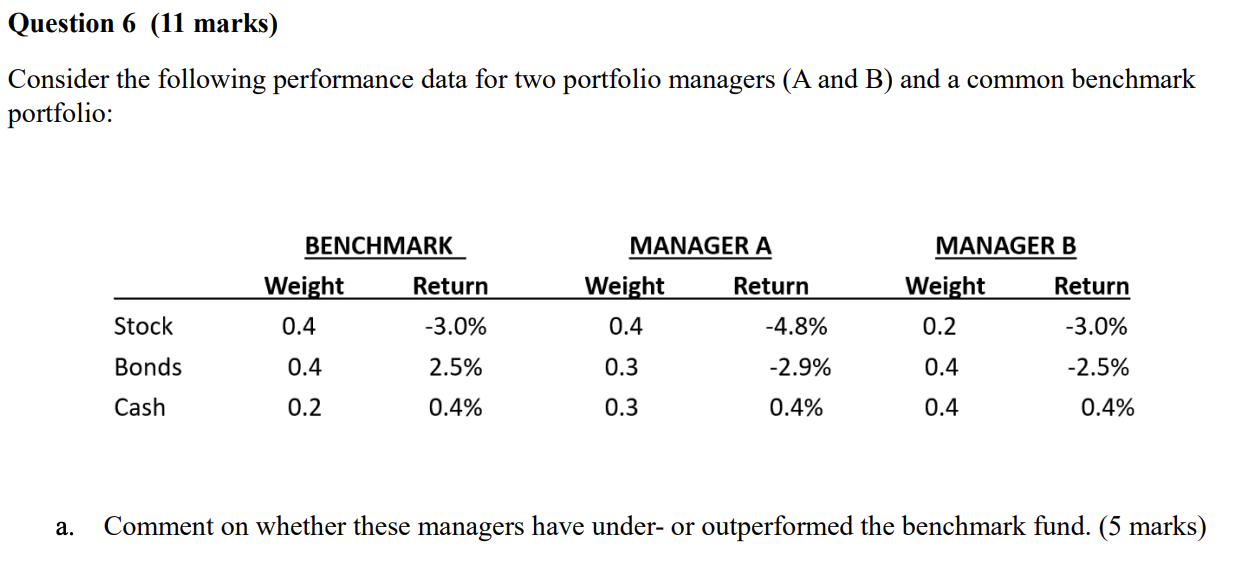

Question: Question 6 (11 marks) Consider the following performance data for two portfolio managers (A and B) and a common benchmark portfolio: BENCHMARK Weight Return 0.4

Question 6 (11 marks) Consider the following performance data for two portfolio managers (A and B) and a common benchmark portfolio: BENCHMARK Weight Return 0.4 -3.0% MANAGER A Weight Return 0.4 -4.8% MANAGER B Weight Return 0.2 -3.0% Stock Bonds 0.4 2.5% 0.3 -2.9% 0.4 -2.5% Cash 0.2 0.4% 0.3 0.4% 0.4 0.4% a. Comment on whether these managers have under- or outperformed the benchmark fund. (5 marks) b. Using attribution analysis, calculate the selection effect for manager A. (2 mark) c. Using attribution analysis, calculate the allocation effect for manager B. (2 mark) d. Using these numbers from (b) and (c), and in conjunction with your results from Part (a), comment on whether these managers have added value through their selection skills, their allocation skills or both. (2 marks)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts