Question: Question 6 ( b ) What is the unconditional variance var ( t ) ? Consider the ARCH model for stock returns ( DLOG (

Question

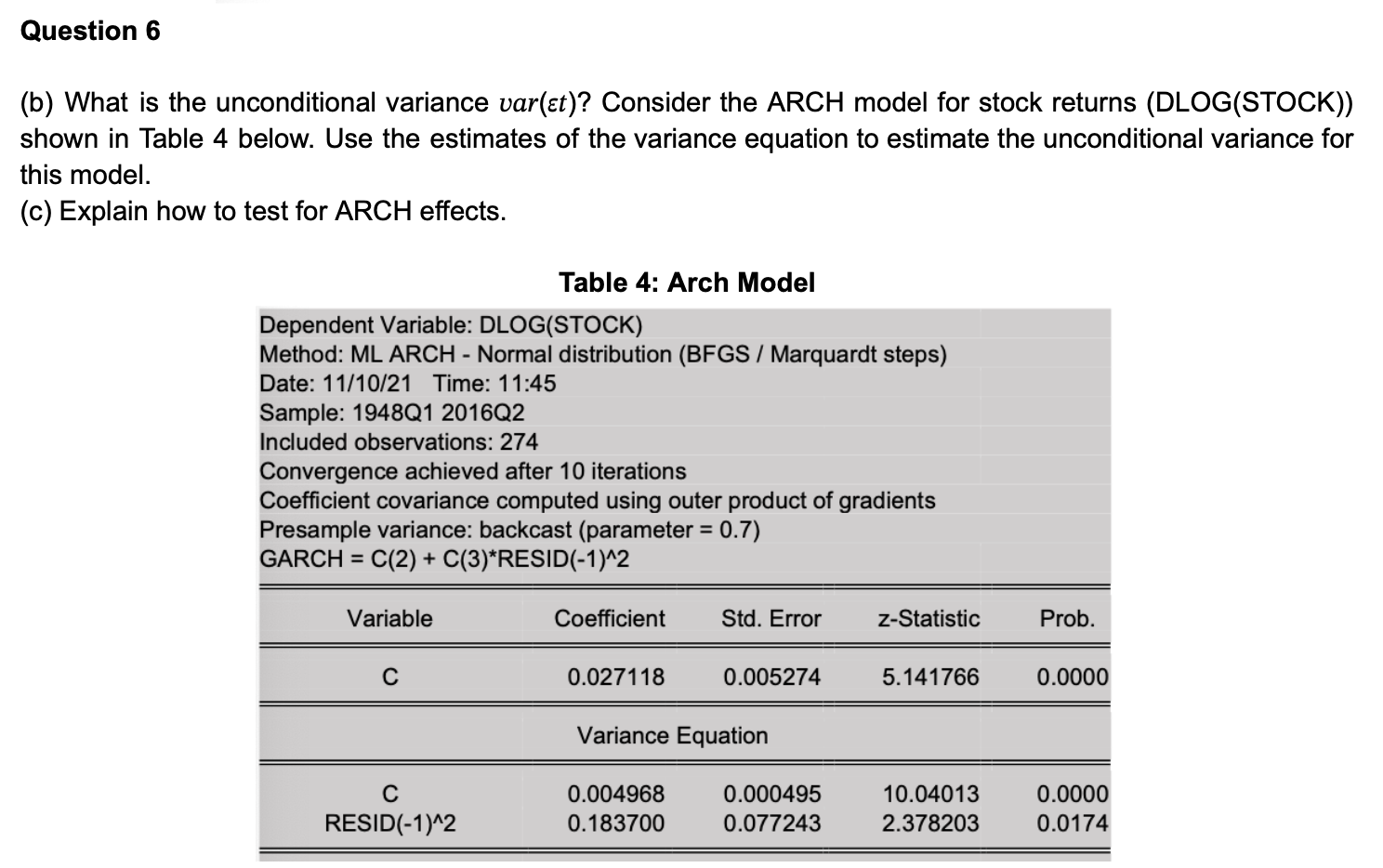

b What is the unconditional variance var Consider the ARCH model for stock returns DLOGSTOCK

shown in Table below. Use the estimates of the variance equation to estimate the unconditional variance for

this model.

c Explain how to test for ARCH effects.

Table : Arch Model

Dependent Variable: DLOGSTOCK

Method: ML ARCH Normal distribution BFGS Marquardt steps

Date: Time: :

Sample: QQ

Included observations:

Convergence achieved after iterations

Coefficient covariance computed using outer product of gradients

Presample variance: backcast parameter

GARCHRESID

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock