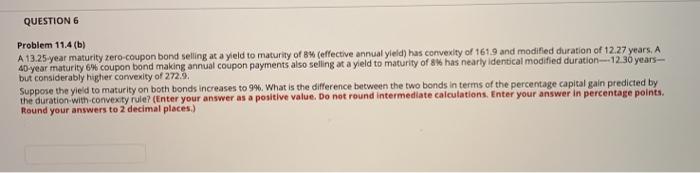

Question: QUESTION 6 Problem 11.4 (b) A 13.25-year maturity zero-coupon bond selling at a yield to maturity of BM (effective annual yield) has convexity of 161.9

QUESTION 6 Problem 11.4 (b) A 13.25-year maturity zero-coupon bond selling at a yield to maturity of BM (effective annual yield) has convexity of 161.9 and modified duration of 12.27 years, A 40 year maturity 6% coupon bond making annual coupon payments also selling at a yield to maturity of 8% has nearly identical modified duration 12.36 years- but considerably higher convexity of 272.6. Suppose the yield to maturity on both bonds increases to 9%. What is the difference between the two bonds in terms of the percentage capital gain predicted by the duration with convexity rule? (Enter your answer as a positive value. Do not round intermediate calculations. Enter your answer in percentage points. Round your answers to 2 decimal places)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts