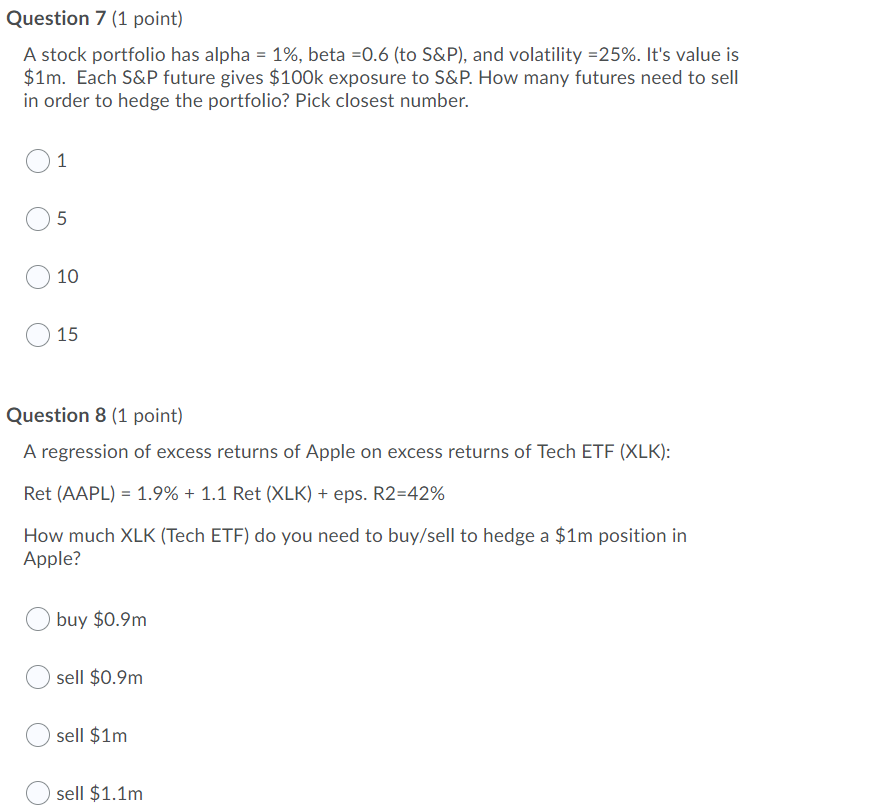

Question: Question 7 (1 point) A stock portfolio has alpha = 1%, beta =0.6 (to S&P), and volatility = 25%. It's value is $1m. Each S&P

Question 7 (1 point) A stock portfolio has alpha = 1%, beta =0.6 (to S&P), and volatility = 25%. It's value is $1m. Each S&P future gives $100k exposure to S&P. How many futures need to sell in order to hedge the portfolio? Pick closest number. 01 O O O 10 O Question 8 (1 point) A regression of excess returns of Apple on excess returns of Tech ETF (XLK): Ret (AAPL) = 1.9% + 1.1 Ret (XLK) + eps. R2=42% How much XLK (Tech ETF) do you need to buy/sell to hedge a $1m position in Apple? buy $0.9m o O sell $0.9m $1m O sell $1.1m Question 7 (1 point) A stock portfolio has alpha = 1%, beta =0.6 (to S&P), and volatility = 25%. It's value is $1m. Each S&P future gives $100k exposure to S&P. How many futures need to sell in order to hedge the portfolio? Pick closest number. 01 O O O 10 O Question 8 (1 point) A regression of excess returns of Apple on excess returns of Tech ETF (XLK): Ret (AAPL) = 1.9% + 1.1 Ret (XLK) + eps. R2=42% How much XLK (Tech ETF) do you need to buy/sell to hedge a $1m position in Apple? buy $0.9m o O sell $0.9m $1m O sell $1.1m

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts