Question: Question 7 (1 point) Saved Suppose that a trader on March 5, 2010, bought a three-year cap on the six-month LIBOR with a cap rate

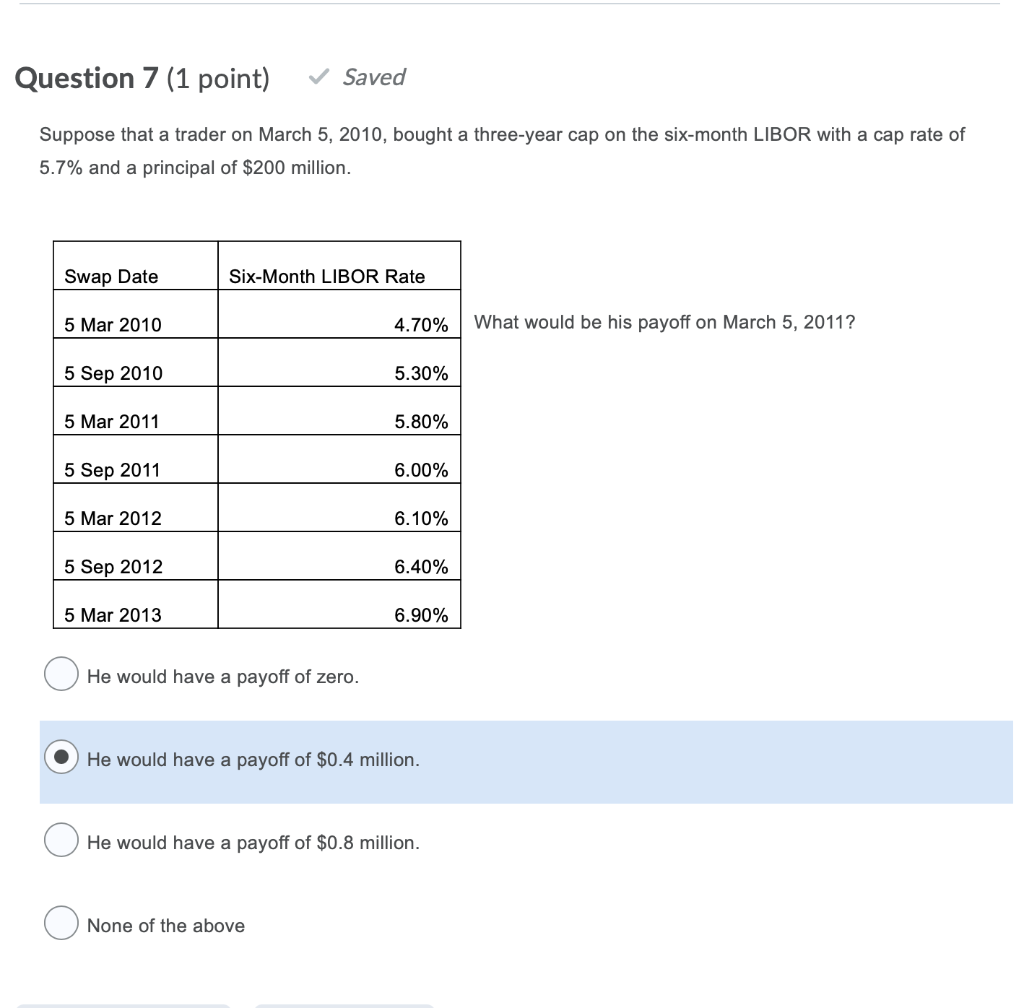

Question 7 (1 point) Saved Suppose that a trader on March 5, 2010, bought a three-year cap on the six-month LIBOR with a cap rate of 5.7% and a principal of $200 million. Swap Date Six-Month LIBOR Rate 5 Mar 2010 4.70% What would be his payoff on March 5, 2011? 5 Sep 2010 5.30% 5 Mar 2011 5.80% 5 Sep 2011 6.00% 5 Mar 2012 6.10% 5 Sep 2012 6.40% 5 Mar 2013 6.90% He would have a payoff of zero. He would have a payoff of $0.4 million. He would have a payoff of $0.8 million. None of the above

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock