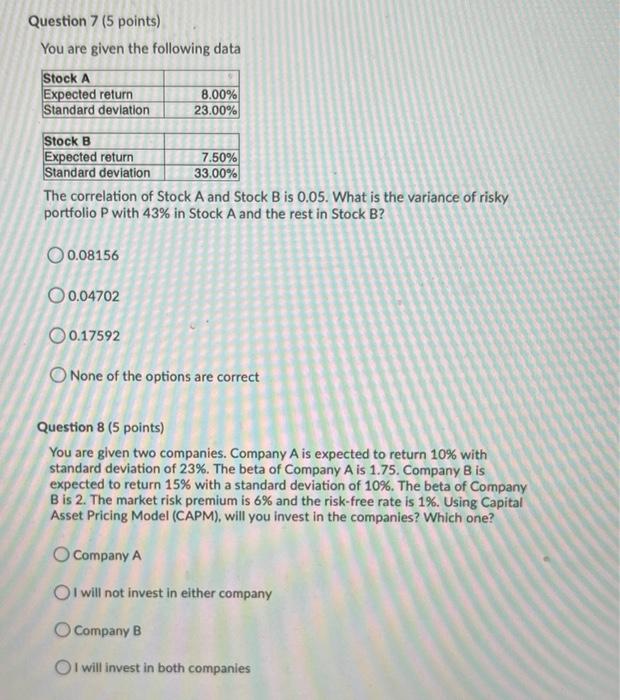

Question: Question 7 (5 points) You are given the following data Stock A Expected return Standard deviation 8.00% 23.00% Stock B Expected return 7.50% Standard deviation

Question 7 (5 points) You are given the following data Stock A Expected return Standard deviation 8.00% 23.00% Stock B Expected return 7.50% Standard deviation 33.00% The correlation of Stock A and Stock B is 0.05. What is the variance of risky portfolio P with 43% in Stock A and the rest in Stock B? 0.08156 O 0.04702 O 0.17592 O None of the options are correct Question 8 (5 points) You are given two companies. Company A is expected to return 10% with standard deviation of 23%. The beta of Company A is 1.75. Company B is expected to return 15% with a standard deviation of 10%. The beta of Company Bis 2. The market risk premium is 6% and the risk-free rate is 1%. Using Capital Asset Pricing Model (CAPM), will you invest in the companies? Which one? O Company A I will not invest in either company Company B I will invest in both companies

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts