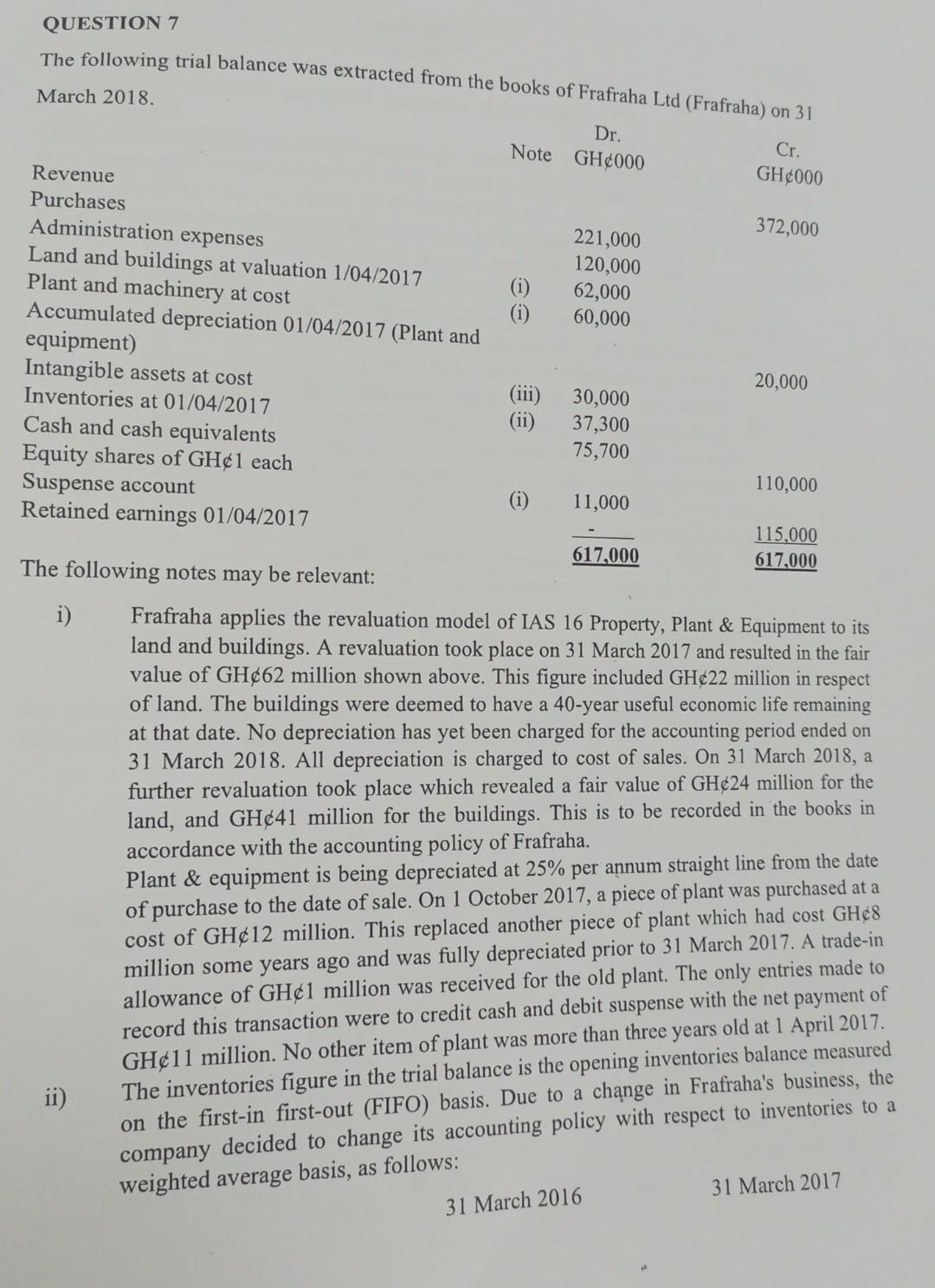

QUESTION 7 The following trial balance was extracted from the books of Frafraha Ltd (Frafraha) on...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

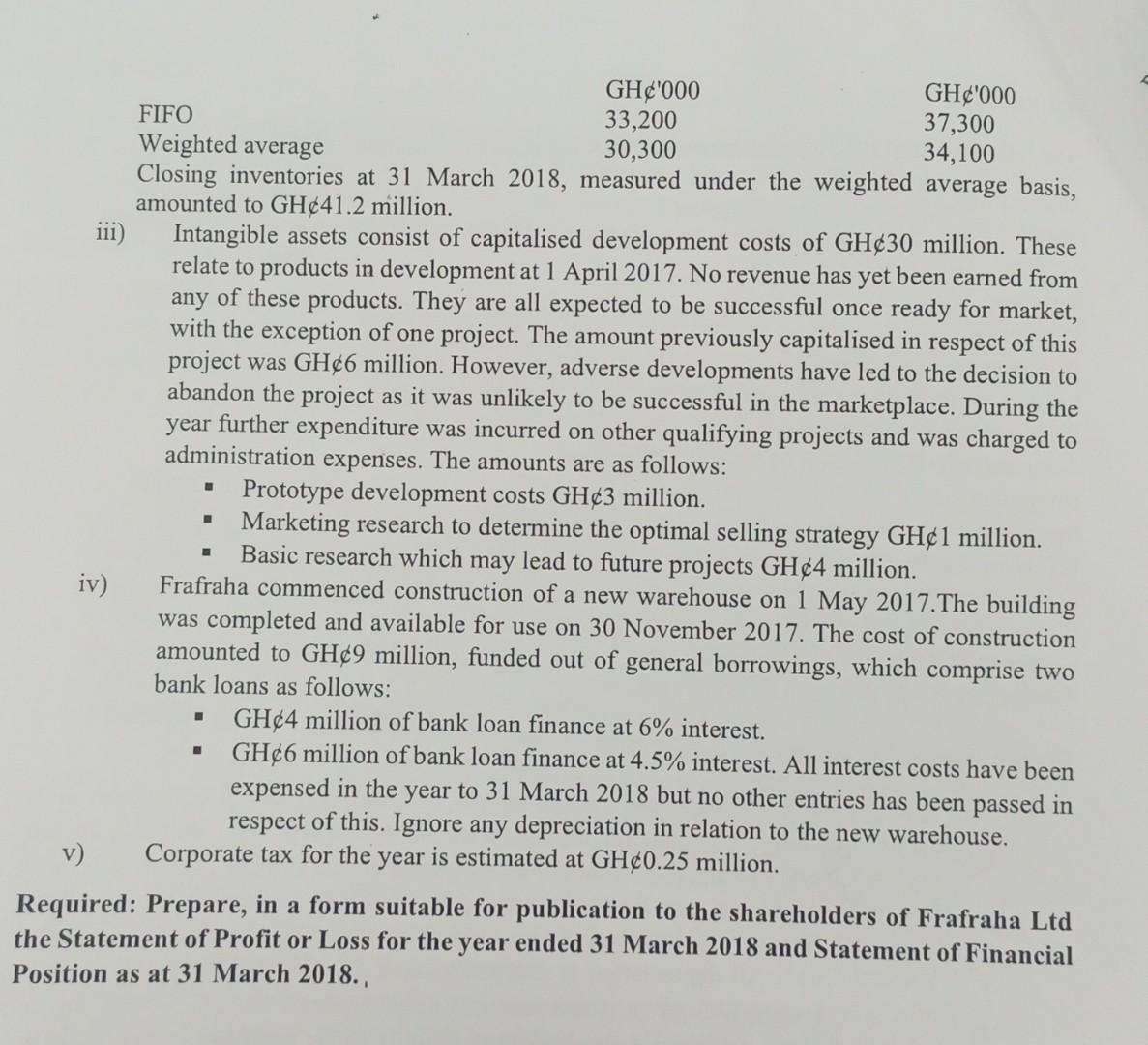

QUESTION 7 The following trial balance was extracted from the books of Frafraha Ltd (Frafraha) on 31 March 2018. Dr. Note GH¢000 Revenue Purchases Administration expenses Land and buildings at valuation 1/04/2017 Plant and machinery at cost Accumulated depreciation 01/04/2017 (Plant and equipment) Intangible assets at cost Inventories at 01/04/2017 Cash and cash equivalents Equity shares of GH¢1 each Suspense account Retained earnings 01/04/2017 The following notes may be relevant: i) ii) (i) (i) (iii) (ii) (i) 221,000 120,000 62,000 60,000 30,000 37,300 75,700 11,000 617,000 Cr. GH 000 372,000 31 March 2016 20,000 110,000 115,000 617,000 Frafraha applies the revaluation model of IAS 16 Property, Plant & Equipment to its land and buildings. A revaluation took place on 31 March 2017 and resulted in the fair value of GH¢62 million shown above. This figure included GH¢22 million in respect of land. The buildings were deemed to have a 40-year useful economic life remaining at that date. No depreciation has yet been charged for the accounting period ended on 31 March 2018. All depreciation is charged to cost of sales. On 31 March 2018, a further revaluation took place which revealed a fair value of GH¢24 million for the land, and GH¢41 million for the buildings. This is to be recorded in the books in accordance with the accounting policy of Frafraha. Plant & equipment is being depreciated at 25% per annum straight line from the date of purchase to the date of sale. On 1 October 2017, a piece of plant was purchased at a cost of GH¢12 million. This replaced another piece of plant which had cost GH¢8 million some years ago and was fully depreciated prior to 31 March 2017. A trade-in allowance of GH¢1 million was received for the old plant. The only entries made to record this transaction were to credit cash and debit suspense with the net payment of GH¢11 million. No other item of plant was more than three years old at 1 April 2017. The inventories figure in the trial balance is the opening inventories balance measured on the first-in first-out (FIFO) basis. Due to a change in Frafraha's business, the company decided to change its accounting policy with respect to inventories to a weighted average basis, as follows: 31 March 2017 GH¢'000 GH¢'000 33,200 FIFO 37,300 Weighted average 30,300 34,100 Closing inventories at 31 March 2018, measured under the weighted average basis, amounted to GH¢41.2 million. 111) Intangible assets consist of capitalised development costs of GH¢30 million. These relate to products in development at 1 April 2017. No revenue has yet been earned from any of these products. They are all expected to be successful once ready for market, with the exception of one project. The amount previously capitalised in respect of this project was GH¢6 million. However, adverse developments have led to the decision to abandon the project as it was unlikely to be successful in the marketplace. During the year further expenditure was incurred on other qualifying projects and was charged to administration expenses. The amounts are as follows: iv) Prototype development costs GH¢3 million. Marketing research to determine the optimal selling strategy GH¢1 million. Basic research which may lead to future projects GH¢4 million. Frafraha commenced construction of a new warehouse on 1 May 2017. The building was completed and available for use on 30 November 2017. The cost of construction amounted to GH¢9 million, funded out of general borrowings, which comprise two bank loans as follows: GH¢4 million of bank loan finance at 6% interest. GH¢6 million of bank loan finance at 4.5% interest. All interest costs have been expensed in the year to 31 March 2018 but no other entries has been passed in respect of this. Ignore any depreciation in relation to the new warehouse. Corporate tax for the year is estimated at GH¢0.25 million. ■ ■ v) Required: Prepare, in a form suitable for publication to the shareholders of Frafraha Ltd the Statement of Profit or Loss for the year ended 31 March 2018 and Statement of Financial Position as at 31 March 2018., QUESTION 7 The following trial balance was extracted from the books of Frafraha Ltd (Frafraha) on 31 March 2018. Dr. Note GH¢000 Revenue Purchases Administration expenses Land and buildings at valuation 1/04/2017 Plant and machinery at cost Accumulated depreciation 01/04/2017 (Plant and equipment) Intangible assets at cost Inventories at 01/04/2017 Cash and cash equivalents Equity shares of GH¢1 each Suspense account Retained earnings 01/04/2017 The following notes may be relevant: i) ii) (i) (i) (iii) (ii) (i) 221,000 120,000 62,000 60,000 30,000 37,300 75,700 11,000 617,000 Cr. GH 000 372,000 31 March 2016 20,000 110,000 115,000 617,000 Frafraha applies the revaluation model of IAS 16 Property, Plant & Equipment to its land and buildings. A revaluation took place on 31 March 2017 and resulted in the fair value of GH¢62 million shown above. This figure included GH¢22 million in respect of land. The buildings were deemed to have a 40-year useful economic life remaining at that date. No depreciation has yet been charged for the accounting period ended on 31 March 2018. All depreciation is charged to cost of sales. On 31 March 2018, a further revaluation took place which revealed a fair value of GH¢24 million for the land, and GH¢41 million for the buildings. This is to be recorded in the books in accordance with the accounting policy of Frafraha. Plant & equipment is being depreciated at 25% per annum straight line from the date of purchase to the date of sale. On 1 October 2017, a piece of plant was purchased at a cost of GH¢12 million. This replaced another piece of plant which had cost GH¢8 million some years ago and was fully depreciated prior to 31 March 2017. A trade-in allowance of GH¢1 million was received for the old plant. The only entries made to record this transaction were to credit cash and debit suspense with the net payment of GH¢11 million. No other item of plant was more than three years old at 1 April 2017. The inventories figure in the trial balance is the opening inventories balance measured on the first-in first-out (FIFO) basis. Due to a change in Frafraha's business, the company decided to change its accounting policy with respect to inventories to a weighted average basis, as follows: 31 March 2017 GH¢'000 GH¢'000 33,200 FIFO 37,300 Weighted average 30,300 34,100 Closing inventories at 31 March 2018, measured under the weighted average basis, amounted to GH¢41.2 million. 111) Intangible assets consist of capitalised development costs of GH¢30 million. These relate to products in development at 1 April 2017. No revenue has yet been earned from any of these products. They are all expected to be successful once ready for market, with the exception of one project. The amount previously capitalised in respect of this project was GH¢6 million. However, adverse developments have led to the decision to abandon the project as it was unlikely to be successful in the marketplace. During the year further expenditure was incurred on other qualifying projects and was charged to administration expenses. The amounts are as follows: iv) Prototype development costs GH¢3 million. Marketing research to determine the optimal selling strategy GH¢1 million. Basic research which may lead to future projects GH¢4 million. Frafraha commenced construction of a new warehouse on 1 May 2017. The building was completed and available for use on 30 November 2017. The cost of construction amounted to GH¢9 million, funded out of general borrowings, which comprise two bank loans as follows: GH¢4 million of bank loan finance at 6% interest. GH¢6 million of bank loan finance at 4.5% interest. All interest costs have been expensed in the year to 31 March 2018 but no other entries has been passed in respect of this. Ignore any depreciation in relation to the new warehouse. Corporate tax for the year is estimated at GH¢0.25 million. ■ ■ v) Required: Prepare, in a form suitable for publication to the shareholders of Frafraha Ltd the Statement of Profit or Loss for the year ended 31 March 2018 and Statement of Financial Position as at 31 March 2018.,

Expert Answer:

Answer rating: 100% (QA)

Particulars Revenue Cost of Sales i Gross Profit Administration Expense 1200006000iv 3000iv Gain on ... View the full answer

Related Book For

Posted Date:

Students also viewed these accounting questions

-

The following trial balance was extracted from the books of Marric Ltd. as at 31.05.03 The following information has not been accounted for: 1. Closing inventory as at 31.05.03 is £497,000 2....

-

Lime's business has had liquidity problems for some months. The following trial balance was extracted from his books of account as at 30 September 2012: Additional information: 1. Stock at 30...

-

The Following Trial Balance Was Extracted From the Books of KINJO Ltd at 31 December 2019 Share capital authorized and issued: 80,000 ordinary shares of 1 each Freehold premises at cost 80,000...

-

Jimmy and Elizabeth plan on getting married on the 15th of August. Elizabeth decides that she would prefer to have the reception in her backyard, so she rents an event tent from CELEBRATE Ltd, a firm...

-

The accounting records of Last Chance, Inc., reveal the following: Requirements 1. Compute cash flows from operating activities by the direct method. 2. Evaluate the operating cash flow of Last...

-

Explain how economic growth may bring about an increase in potential output. the world, especially China. China's foreign direct investment in new projects such as renewable energy, textile factories...

-

Show that A* is optimal and complete in most circumstances.

-

The town barber shop can accommodate 35 customers per day. The manager has determined that if two additional barbers are hired, the shop can accommodate 80 customers per day. What are the design and...

-

It is the first week of December and Christmas break is right around the corner when a close colleague of yours approaches you in confidence. Kelley Garcia is also a second year teacher and you were...

-

Honolulu Shirt Shop has very seasonal sales. Assume that for next year management is trying to decide whether to establish a sales budget based on average sales or on sales estimated by quarter. The...

-

Construct the indicated confidence interval for the population meanu using the t-distribution. Assume the population is normally distributed. c= 0.90, x= 12.8, s 2.0, n 6 (Round to one decimal place...

-

If the outlay is lower by the amount that Simpson suggests, the project NPV should increase by an amount closest to: A. 0.09 billion. B. 0.14 billion. C. 0.17 billion. Barbara Simpson is a sell-side...

-

Steve Jackson (birthdate December 13, 1967) is a single taxpayer living at 3215 Pacific Dr., Apt. B, Pacific Beach, CA 92109. His Social Security number is 465-88-9415. In 2020, Steves earnings and...

-

A switch from straight-line to accelerated depreciation would: A. increase the NPV and decrease the first year operating income after taxes. B. increase the first year operating income after taxes...

-

Simpson should estimate the initial outlay and the terminal year nonoperating cash flow, respectively, to be closest to: A. 1.50 billion and 0.70 billion. B. 1.90 billion and 0.70 billion. C. 1.90...

-

The following are selected account balances for Warren Clinic as of December 31, 2015, in alphabetical order. Create Warren Clinics balance sheet. Accounts payable Accounts receivable, net Cash $...

-

1. Why are visuals/charts important in technical writing? 2. What is the reason for using each of the visuals/charts? 3. Describe the visual/chart. 1 2 3 4 LO 5 6 7 Name of the chart/graph Tables...

-

a. Determine the domain and range of the following functions.b. Graph each function using a graphing utility. Be sure to experiment with the window and orientation to give the best perspective of the...

-

From the following information in respect of Orchard Ltd., prepare the statement of cash flows for the year ended 31.03.20X3 STATEMENT OF FINANCIAL POSITION AT Income statement for the years ended...

-

Minor Cars Ltd., a small company selling second-hand cars, has just been taken over by Major Vehicles plc, which runs a chain of garages. One implication is that the existing accounting systems of...

-

Identify and discuss the determinants of the accounting framework of three countries in Europe and explain why these might present barriers to the harmonisation of accounting across Europe.

-

Find the flexibility and stiffness influence coefficients of the torsional system shown in Fig. 6.28. Also write the equations of motion of the system. (GJ)1 01 Compressor (GJ)2 (Jan) Turbine (142)...

-

Derive the flexibility matrix of the system shown in Fig. 5.42. 00000 2m 8(t) * 2m ellee x(t) m 00000 FIGURE 5.42 Rigid bar connected to masses and springs.

-

Derive the stiffness matrix of the system shown in Fig. 5.39. mo e(t) ellee k1 k2 lllll m x(t) FIGURE 5.39 Mass hanging from a pulley.

Study smarter with the SolutionInn App