Question: Question 9 : Can you explain step by step please? Assume a cross - rate trader at Soci t G n rale notices that BNP

Question : Can you explain step by step please?

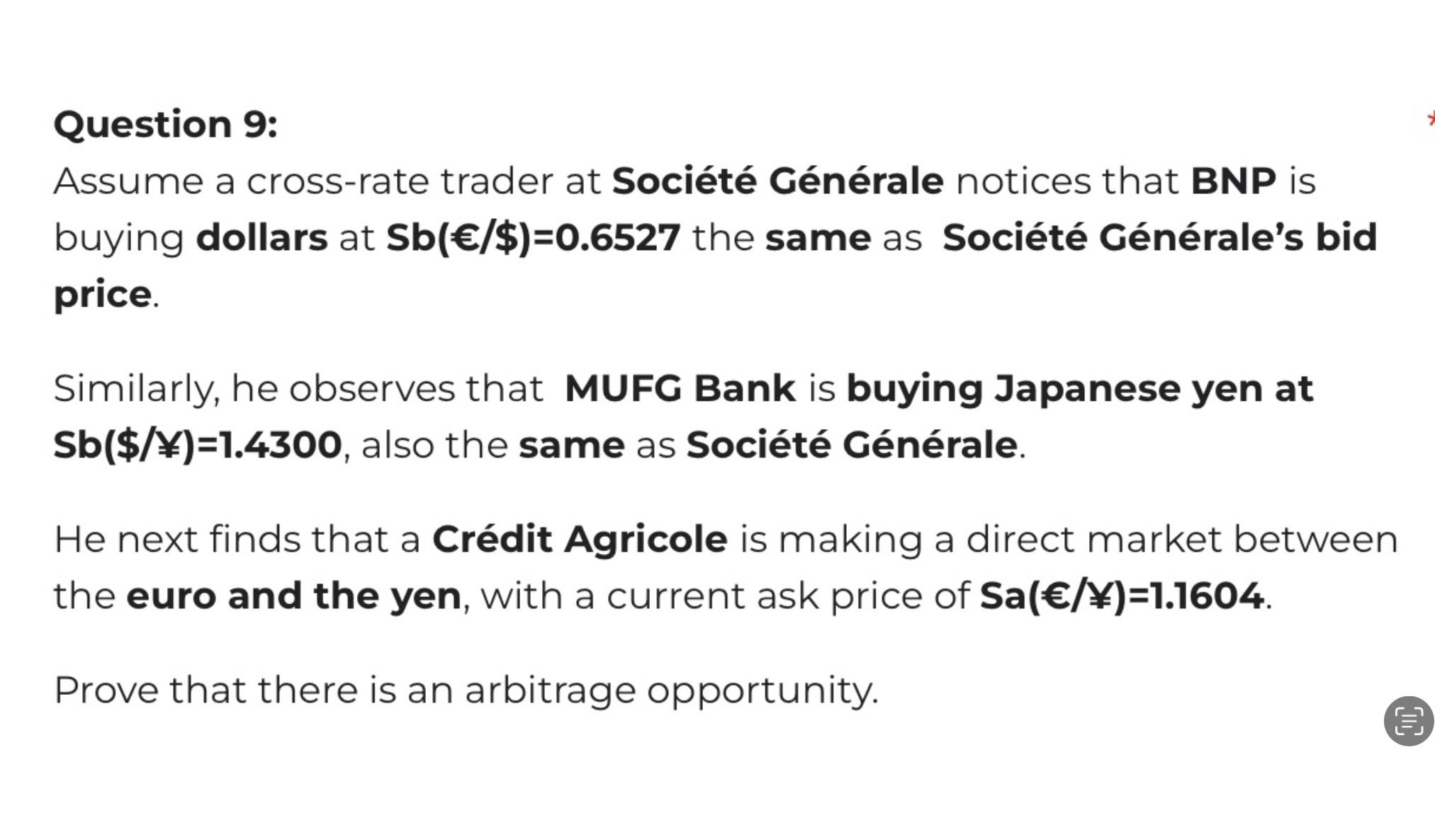

Assume a crossrate trader at Socit Gnrale notices that BNP is buying dollars at the same as Socit Gnrales bid price.

Similarly, he observes that MUFG Bank is buying Japanese yen at # also the same as Socit Gnrale

He next finds that a Crdit Agricole is making a direct market between the euro and the yen, with a current ask price of

Prove that there is an arbitrage opportunity.

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock