Question: Question: Chief executives with multi-million-dollar pay packets are not necessarily working in the best interests of shareholders and there may be a case to cap

Question:

Chief executives with multi-million-dollar pay packets are not necessarily working in the best interests of shareholders and there may be a case to cap their pay. New research explores whether limits on executive pay hurt or benefit shareholders and suggests that providing CEOs with $10 million bonuses encourages them to make short-term decisions rather than work closely with the board and in the best interest of shareholders. The research proposes that limiting executive compensation might be more beneficial for shareholders. Over the past 30 years, CEO compensation has been increasing on the basis of a theoretical argument that it creates shareholder value. However, the current system encourages companies to be 'transactional focused' rather than building capacity and innovating; CEOs are likely to pursue strategies with outcomes that are easy to measure in financial terms. It has been proposed that the current corporate governance structure and guidelines in Australia encourage director independence. But this often means that directors do not have a deep understanding of the business. Relying on financial performance measures means directors do not need to really understand whether CEOs are good leaders, insightful, pursuing the right strategies and communicating well. Source: Adapted from Nassim Khadem, '$10m CEO bonuses encourage short-term decisions', The Sydney Morning Herald.146 in Rankin M. et al: Contemporary Issues in Accounting (2e) Case Study 5.2, p.168-169

The article highlights the excessive use of bonuses to encourage shore-term decisions. From an agency perspective, why would managers prefer short-term cash bonuses instead of long-term equity bonuses? What problems does this approach lead to for the board of directors and shareholders? In presenting your answer you should refer to relevant information in the above article to support your view.

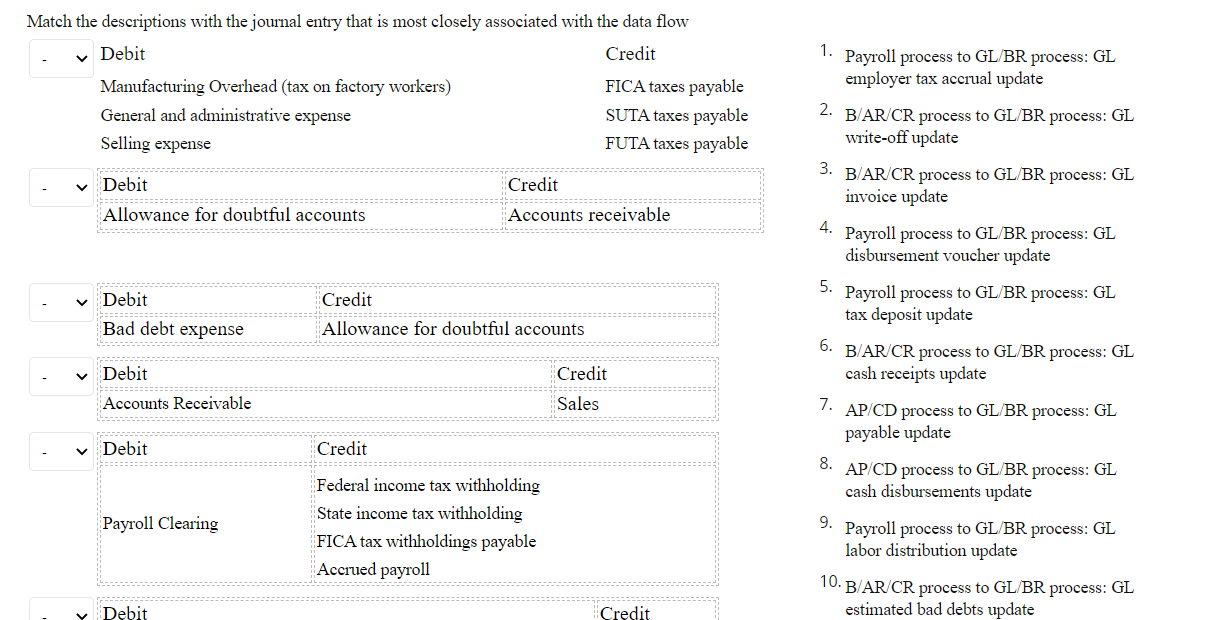

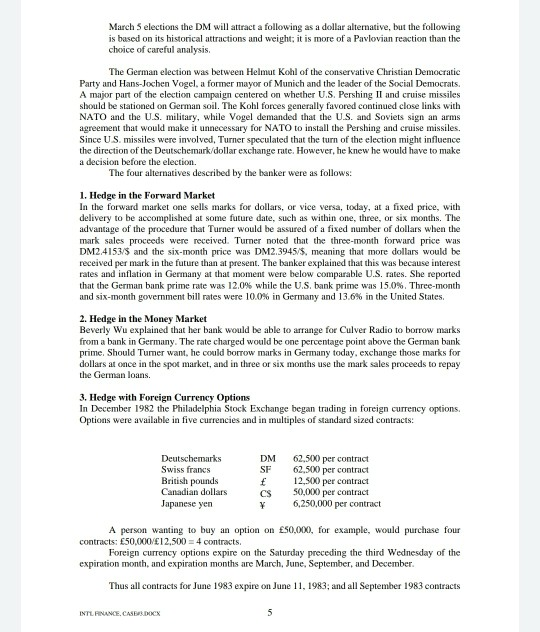

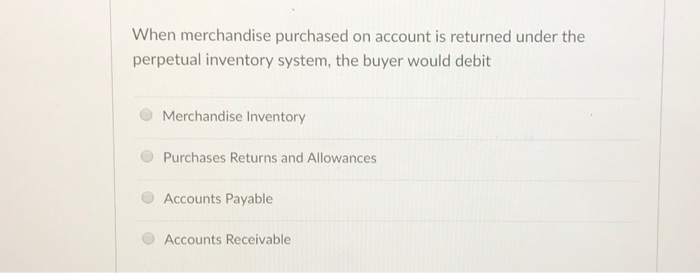

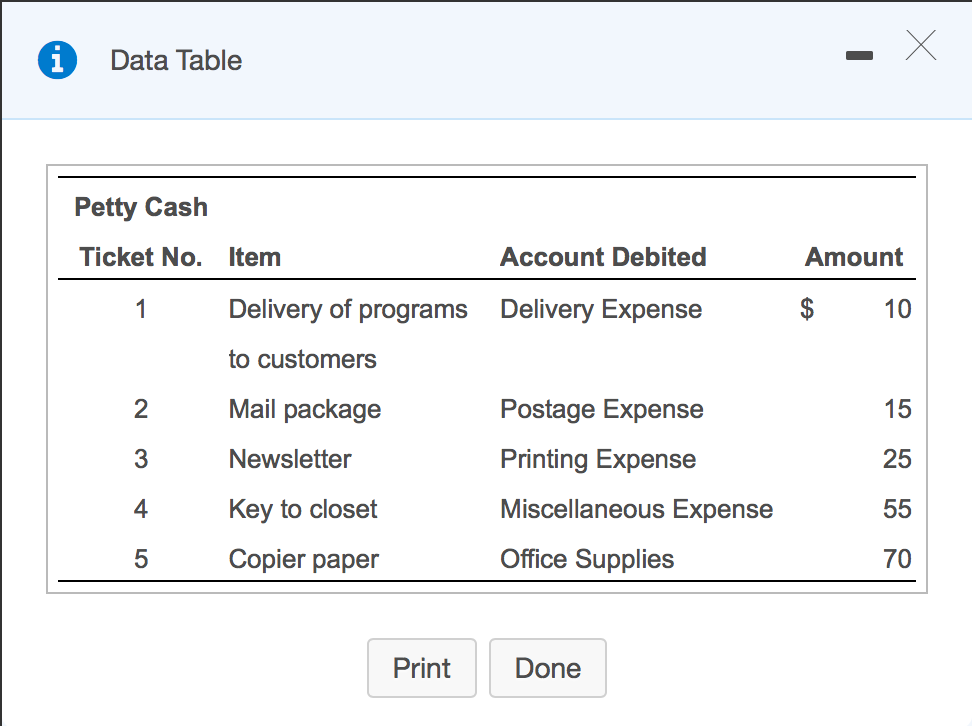

Match the descriptions with the journal entry that is most closely associated with the data flow Debit Credit 1. Payroll process to GL/BR process: GL Manufacturing Overhead (tax on factory workers) FICA taxes payable employer tax accrual update General and administrative expense SUTA taxes payable 2. B/AR/CR process to GL/BR process: GL Selling expense FUTA taxes payable write-off update Debit Credit 3. B/AR/CR process to GL/BR process: GL invoice update Allowance for doubtful accounts Accounts receivable 4. Payroll process to GL/BR process: GL disbursement voucher update v Debit Credit 5. Payroll process to GL/BR process: GL tax deposit update Bad debt expense Allowance for doubtful accounts 6. B/AR/CR process to GL/BR process: GL V Debit Credit cash receipts update Accounts Receivable Sales 7. AP/CD process to GL/BR process: GL payable update v Debit Credit 8. AP/CD process to GL/BR process: GL Federal income tax withholding cash disbursements update Payroll Clearing State income tax withholding FICA tax withholdings payable 9. Payroll process to GL/BR process: GL labor distribution update Accrued payroll 10. B/AR/CR process to GL/BR process: GL *Debit Credit estimated bad debts updateMarch 5 elections the DM will attract a following as a dollar alternative, but the following is based on its historical attractions and weight: it is more of a Pavlovian reaction than the choice of careful analysis. The German election was between Helmut Kohl of the conservative Christian Democratic Party and Hans-Jochen Vogel, a former mayor of Munich and the leader of the Social Democrats. A major part of the election campaign centered on whether U.S. Pershing II and cruise missiles should be stationed on German soil. The Kohl forces generally favored continued close links with NATO and the U.S. military, while Vogel demanded that the U.S. and Soviets sign an arms agreement that would make it unnecessary for NATO to install the Pershing and cruise missiles. Since U.S. missiles were involved, Turner speculated that the turn of the election might influence the direction of the Deutschemark/dollar exchange rate. However, he knew he would have to make a decision before the election. The four alternatives described by the banker were as follows: 1. Hedge in the Forward Market In the forward market one sells marks for dollars, or vice versa, today, at a fixed price, with delivery to be accomplished at some future date, such as within one, three, or six months. The advantage of the procedure that Turner would be assured of a fixed number of dollars when the mark sales proceeds were received. Turner noted that the three-month forward price was DM24153/3 and the six-month price was DM2.3945/5. meaning that more dollars would be received per mark in the future than at present. The banker explained that this was because interest rates and inflation in Germany at that moment were below comparable U.S. rates. She reported that the German bank prime rate was 12.0% while the U.S. bank prime was 15.0%, Three-month and six-month government bill rates were 10.0% in Germany and 13.6% in the United States, 2. Hedge in the Money Market Beverly Wu explained that her bank would be able to arrange for Culver Radio to borrow marks from a bank in Germany. The rate charged would be one percentage point above the German bank prime. Should Turner want, he could borrow marks in Germany today, exchange those marks for dollars at once in the spot market, and in three or six months use the mark sales proceeds to repay the German loans. 3. Hedge with Foreign Currency Options In December 1982 the Philadelphia Stock Exchange began trading in foreign currency options. Options were available in five currencies and in multiples of standard sized contracts: Deutschemarks DM 62.500 per contract Swiss francs 62.500 per contract British pounds f 12,500 per contract Canadian dollars CS 50,000 per contract Japanese yen 6,250,000 per contract A person wanting to buy an option on $50,000, for example, would purchase four contracts: $50,000/$12.500 = 4 contracts. Foreign currency options expire on the Saturday preceding the third Wednesday of the expiration month, and expiration months are March, June. September, and December. Thus all contracts for June 1983 expire on June 11, 1983; and all September 1983 contracts INTL FRANCE. CATE ADORNWhen merchandise purchased on account is returned under the perpetual inventory system, the buyer would debit O Merchandise Inventory O Purchases Returns and Allowances O Accounts Payable Accounts Receivablei Data Table X Petty Cash Ticket No. Item Account Debited Amount Delivery of programs Delivery Expense $ 10 to customers 2 Mail package Postage Expense 15 3 Newsletter Printing Expense 25 4 Key to closet Miscellaneous Expense 55 5 Copier paper Office Supplies 70 Print Done

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts