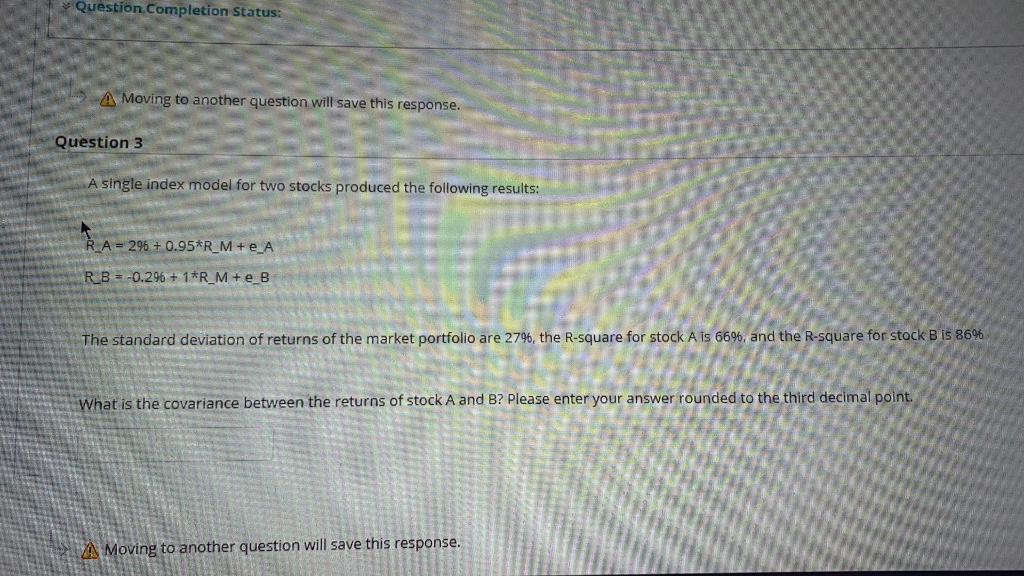

Question: Question Completion Status: A Moving to another question will save this response. Question 3 A single index model for two stocks produced the following results:

Question Completion Status: A Moving to another question will save this response. Question 3 A single index model for two stocks produced the following results: A = 296 + 0.95*R_M + e_A RB = -0.296 + 1*R_M+e_B The standard deviation of returns of the market portfolio are 2796, the R-square for stock A is 66%6, and the R-square for stock B is 86% What is the covariance between the returns of stock A and B? Please enter your answer rounded to the third decimal point. A Moving to another question will save this response. Question Completion Status: A Moving to another question will save this response. Question 3 A single index model for two stocks produced the following results: A = 296 + 0.95*R_M + e_A RB = -0.296 + 1*R_M+e_B The standard deviation of returns of the market portfolio are 2796, the R-square for stock A is 66%6, and the R-square for stock B is 86% What is the covariance between the returns of stock A and B? Please enter your answer rounded to the third decimal point. A Moving to another question will save this response

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts