Question: Question Completion Status: The next two questions are based on the following A European call option and put option on a stock both have a

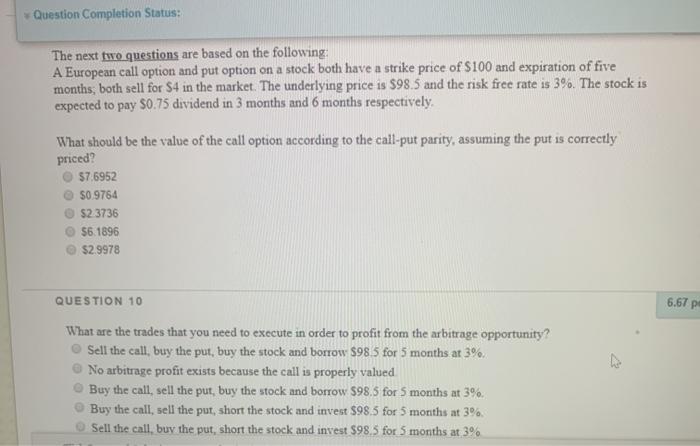

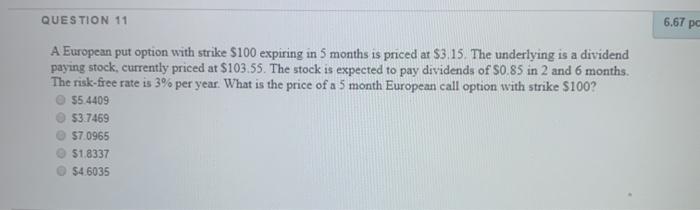

Question Completion Status: The next two questions are based on the following A European call option and put option on a stock both have a strike price of $100 and expiration of five months, both sell for S4 in the market. The underlying price is $98.5 and the risk free rate is 3%. The stock is expected to pay $0.75 dividend in 3 months and 6 months respectively, What should be the value of the call option according to the call-put parity, assuming the put is correctly priced? 57.6952 $0.9764 $23736 $6.1896 $2.9978 QUESTION 10 6.67 p What are the trades that you need to execute in order to profit from the arbitrage opportunity? Sell the call, buy the put, buy the stock and borrow $985 for 5 months at 3%. No arbitrage profit exists because the call is properly valued Buy the call, sell the put, buy the stock and borrow $98.5 for 5 months at 3%. Buy the call, sell the pur, short the stock and invest $98.5 for 5 months at 3%. Sell the call, buy the put, short the stock and invest $98,5 for 5 months at 3% QUESTION 11 6.67 pa A European put option with strike $100 expiring in 5 months is priced at $3.15. The underlying is a dividend paying stock, currently priced at $103.55. The stock is expected to pay dividends of $0.85 in 2 and 6 months. The risk-free rate is 3% per year. What is the price of a 5 month European call option with strike $100? 55.4409 $3.7469 $7.0965 $1.8337 $46035

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts