Question: Question: Critically evaluate the adequacy of the proposed model using a range of model diagnostic tests listed below. Choose three from the list below. Discuss

Question: Critically evaluate the adequacy of the proposed model using a range of model diagnostic tests listed below. Choose three from the list below. Discuss your results, combining the evidence from these three tests:

Bayes factor for H0: 5 = 0 against H1: 50

Signal-to-noise ratio or Cohens f2

RESET

A test for non-normality, heteroskedasticity or autocorrelation (either using data visualization or statistical tests)

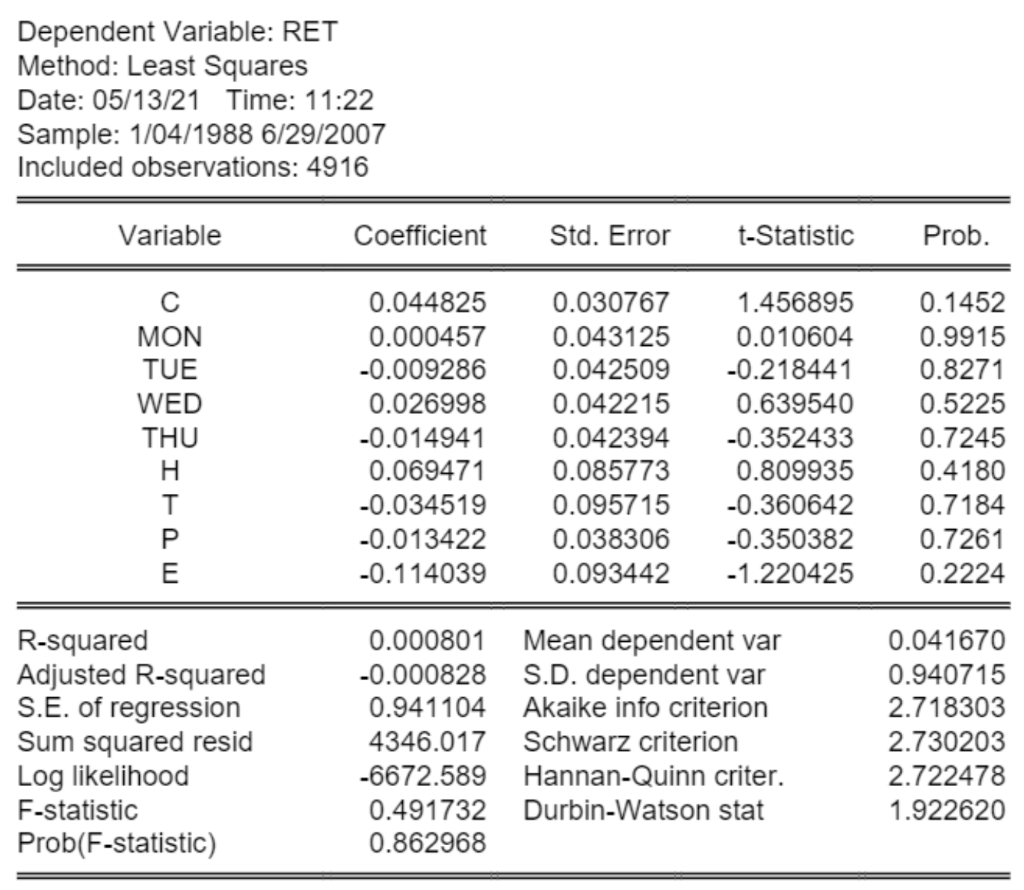

The discussion based on the table below

Dependent Variable: RET Method: Least Squares Date: 05/13/21 Time: 11:22 Sample: 1/04/1988 6/29/2007 Included observations: 4916 Variable Coefficient Std. Error t-Statistic Prob. MON TUE WED THU H 0.044825 0.000457 -0.009286 0.026998 -0.014941 0.069471 -0.034519 -0.013422 -0.114039 0.030767 0.043125 0.042509 0.042215 0.042394 0.085773 0.095715 0.038306 0.093442 1.456895 0.010604 -0.218441 0.639540 -0.352433 0.809935 -0.360642 -0.350382 -1.220425 0.1452 0.9915 0.8271 0.5225 0.7245 0.4180 0.7184 0.7261 0.2224 IAW R-squared Adjusted R-squared S.E. of regression Sum squared resid Log likelihood F-statistic Prob(F-statistic) 0.000801 Mean dependent var -0.000828 S.D. dependent var 0.941104 Akaike info criterion 4346.017 Schwarz criterion -6672.589 Hannan-Quinn criter. 0.491732 Durbin-Watson stat 0.862968 0.041670 0.940715 2.718303 2.730203 2.722478 1.922620 Dependent Variable: RET Method: Least Squares Date: 05/13/21 Time: 11:22 Sample: 1/04/1988 6/29/2007 Included observations: 4916 Variable Coefficient Std. Error t-Statistic Prob. MON TUE WED THU H 0.044825 0.000457 -0.009286 0.026998 -0.014941 0.069471 -0.034519 -0.013422 -0.114039 0.030767 0.043125 0.042509 0.042215 0.042394 0.085773 0.095715 0.038306 0.093442 1.456895 0.010604 -0.218441 0.639540 -0.352433 0.809935 -0.360642 -0.350382 -1.220425 0.1452 0.9915 0.8271 0.5225 0.7245 0.4180 0.7184 0.7261 0.2224 IAW R-squared Adjusted R-squared S.E. of regression Sum squared resid Log likelihood F-statistic Prob(F-statistic) 0.000801 Mean dependent var -0.000828 S.D. dependent var 0.941104 Akaike info criterion 4346.017 Schwarz criterion -6672.589 Hannan-Quinn criter. 0.491732 Durbin-Watson stat 0.862968 0.041670 0.940715 2.718303 2.730203 2.722478 1.922620

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts