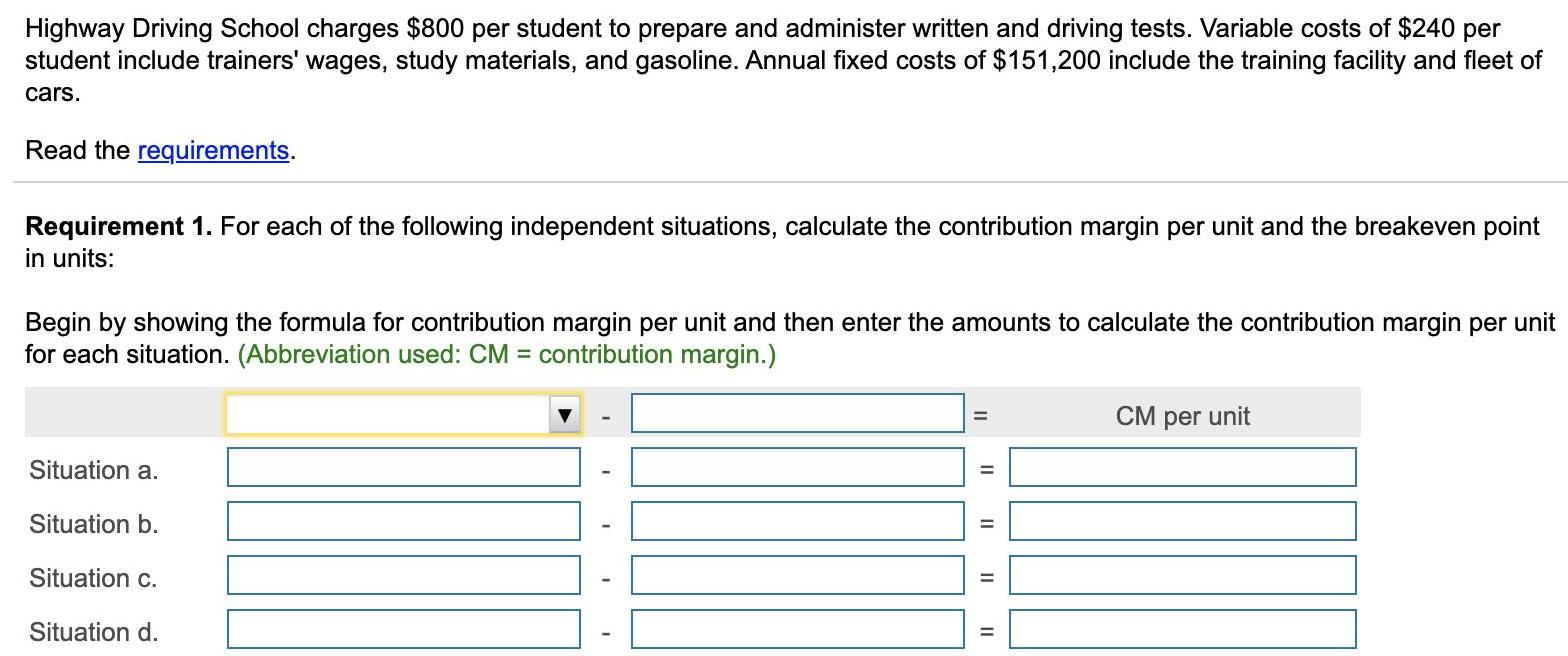

Highway Driving School charges $800 per student to prepare and administer written and driving tests. Variable...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

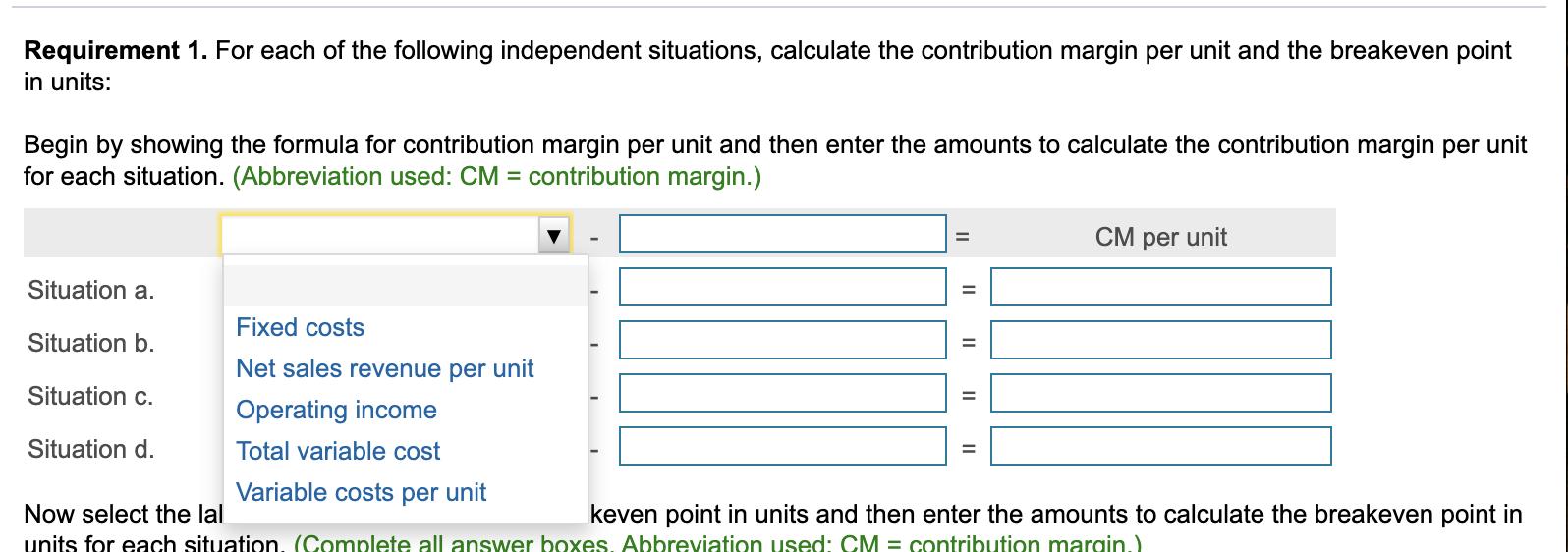

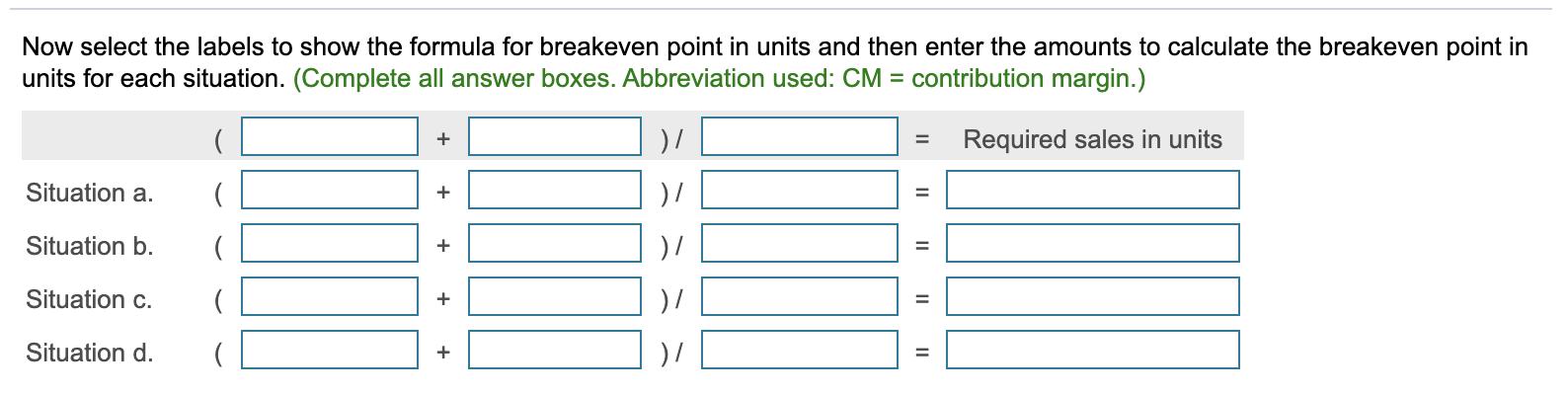

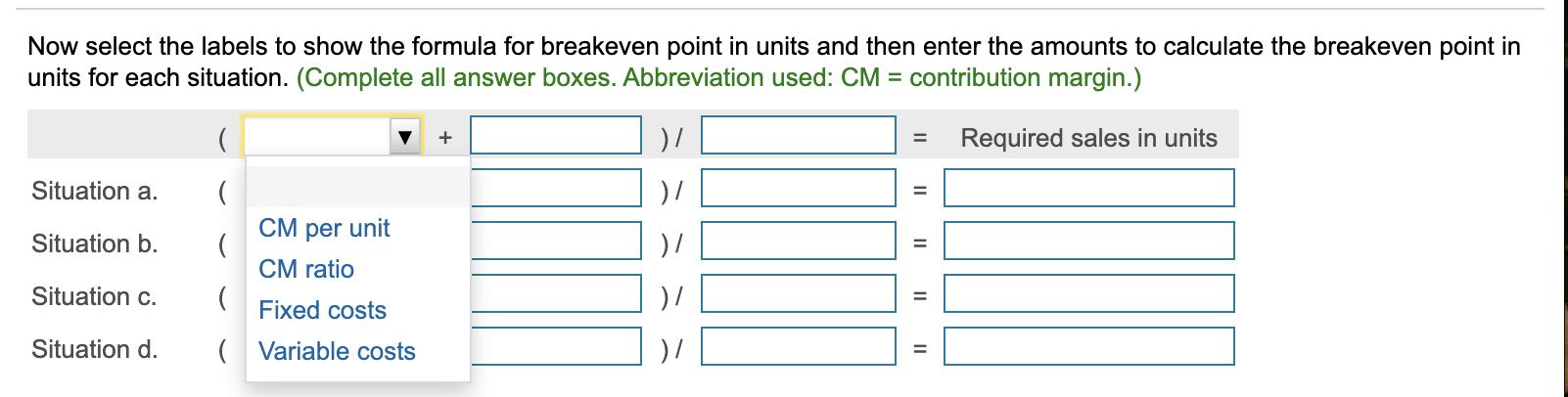

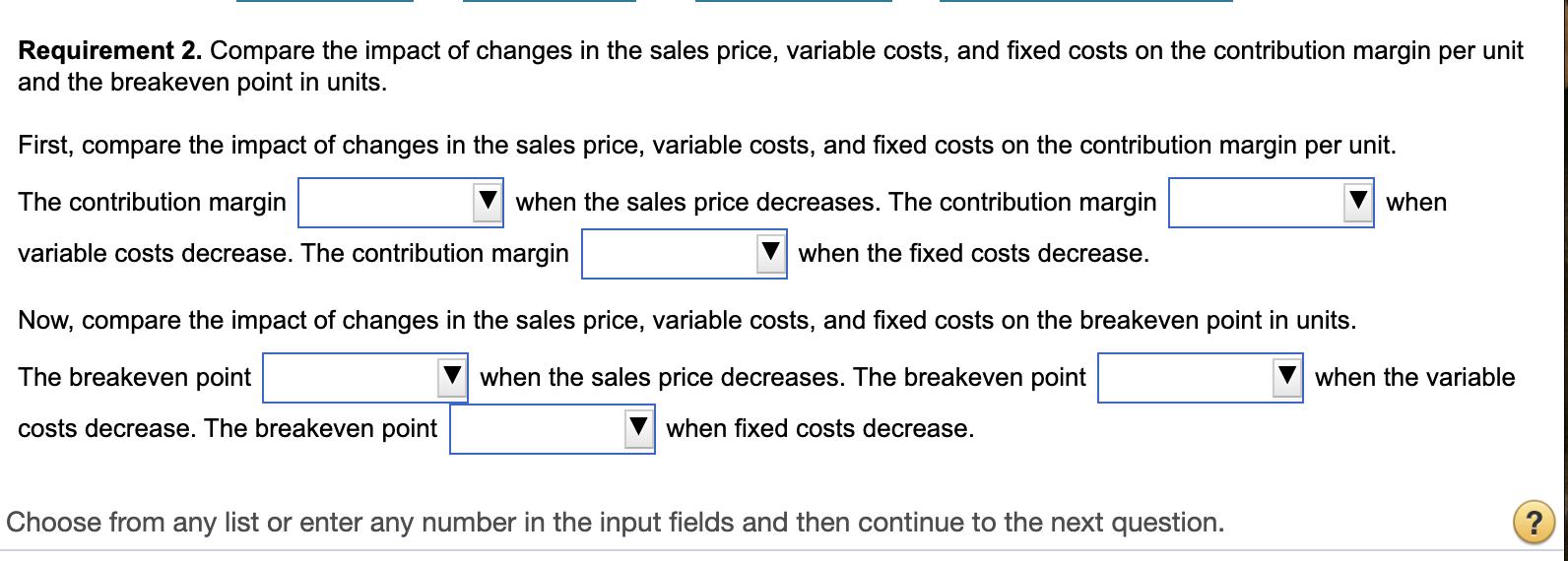

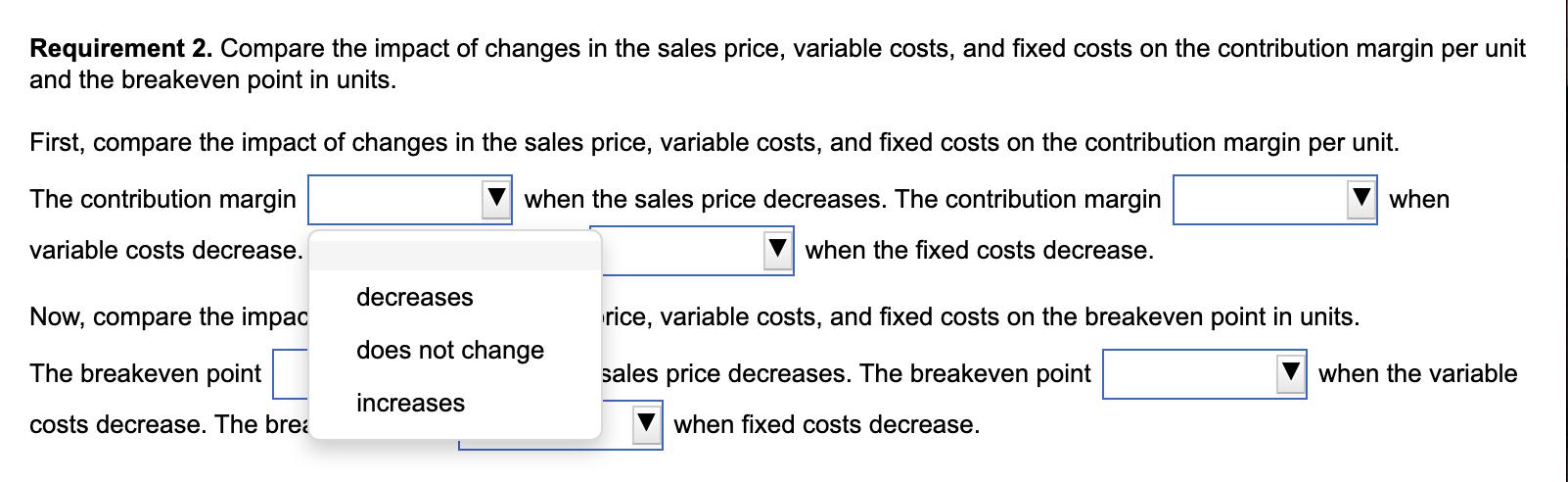

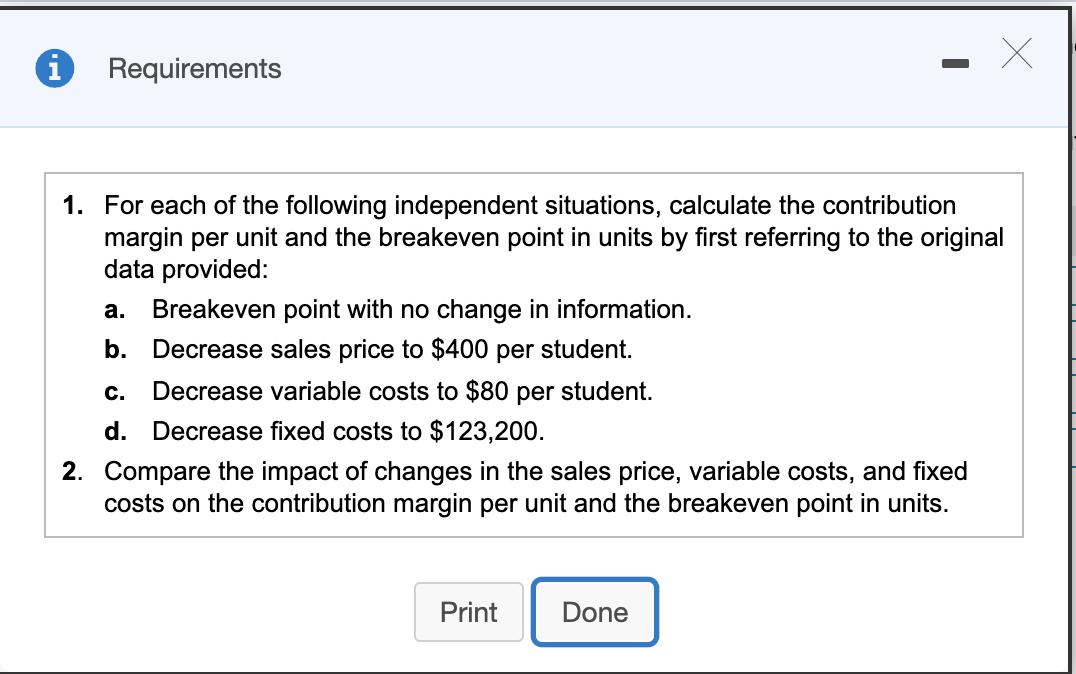

Highway Driving School charges $800 per student to prepare and administer written and driving tests. Variable costs of $240 per student include trainers' wages, study materials, and gasoline. Annual fixed costs of $151,200 include the training facility and fleet of cars. Read the requirements. Requirement 1. For each of the following independent situations, calculate the contribution margin per unit and the breakeven point in units: Begin by showing the formula for contribution margin per unit and then enter the amounts to calculate the contribution margin per unit for each situation. (Abbreviation used: CM = contribution margin.) CM per unit %3D Situation a. Situation b. Situation c. Situation d. II || I| II Requirement 1. For each of the following independent situations, calculate the contribution margin per unit and the breakeven point in units: Begin by showing the formula for contribution margin per unit and then enter the amounts to calculate the contribution margin per unit for each situation. (Abbreviation used: CM = contribution margin.) CM per unit Situation a. Fixed costs Situation b. Net sales revenue per unit Situation c. Operating income Situation d. Total variable cost Variable costs per unit Now select the lal keven point in units and then enter the amounts to calculate the breakeven point in units for each situation, (Complete all answer boxes, Abbreviation used: CM = contribution margin.) II II I| II Now select the labels to show the formula for breakeven point in units and then enter the amounts to calculate the breakeven point in units for each situation. (Complete all answer boxes. Abbreviation used: CM = contribution margin.) + Required sales in units %3D Situation a. + %3D Situation b. + Situation c. Situation d. + II II || + Now select the labels to show the formula for breakeven point in units and then enter the amounts to calculate the breakeven point in units for each situation. (Complete all answer boxes. Abbreviation used: CM = contribution margin.) Required sales in units %3D Situation a. %3D CM per unit ( CM ratio ( Situation b. Situation c. Fixed costs Situation d. ( Variable costs Requirement 2. Compare the impact of changes in the sales price, variable costs, and fixed costs on the contribution margin per unit and the breakeven point in units. First, compare the impact of changes in the sales price, variable costs, and fixed costs on the contribution margin per unit. The contribution margin when the sales price decreases. The contribution margin when variable costs decrease. The contribution margin when the fixed costs decrease. Now, compare the impact of changes in the sales price, variable costs, and fixed costs on the breakeven point in units. The breakeven point when the sales price decreases. The breakeven point when the variable costs decrease. The breakeven point when fixed costs decrease. Choose from any list or enter any number in the input fields and then continue to the next question. Requirement 2. Compare the impact of changes in the sales price, variable costs, and fixed costs on the contribution margin per unit and the breakeven point in units. First, compare the impact of changes in the sales price, variable costs, and fixed costs on the contribution margin per unit. The contribution margin when the sales price decreases. The contribution margin when variable costs decrease. when the fixed costs decrease. decreases Now, compare the impac rice, variable costs, and fixed costs on the breakeven point in units. does not change The breakeven point sales price decreases. The breakeven point when the variable increases costs decrease. The brea when fixed costs decrease. i Requirements 1. For each of the following independent situations, calculate the contribution margin per unit and the breakeven point in units by first referring to the original data provided: а. Breakeven point with no change in information. b. Decrease sales price to $400 per student. с. Decrease variable costs to $80 per student. d. Decrease fixed costs to $123,200. 2. Compare the impact of changes in the sales price, variable costs, and fixed costs on the contribution margin per unit and the breakeven point in units. Print Done Highway Driving School charges $800 per student to prepare and administer written and driving tests. Variable costs of $240 per student include trainers' wages, study materials, and gasoline. Annual fixed costs of $151,200 include the training facility and fleet of cars. Read the requirements. Requirement 1. For each of the following independent situations, calculate the contribution margin per unit and the breakeven point in units: Begin by showing the formula for contribution margin per unit and then enter the amounts to calculate the contribution margin per unit for each situation. (Abbreviation used: CM = contribution margin.) CM per unit %3D Situation a. Situation b. Situation c. Situation d. II || I| II Requirement 1. For each of the following independent situations, calculate the contribution margin per unit and the breakeven point in units: Begin by showing the formula for contribution margin per unit and then enter the amounts to calculate the contribution margin per unit for each situation. (Abbreviation used: CM = contribution margin.) CM per unit Situation a. Fixed costs Situation b. Net sales revenue per unit Situation c. Operating income Situation d. Total variable cost Variable costs per unit Now select the lal keven point in units and then enter the amounts to calculate the breakeven point in units for each situation, (Complete all answer boxes, Abbreviation used: CM = contribution margin.) II II I| II Now select the labels to show the formula for breakeven point in units and then enter the amounts to calculate the breakeven point in units for each situation. (Complete all answer boxes. Abbreviation used: CM = contribution margin.) + Required sales in units %3D Situation a. + %3D Situation b. + Situation c. Situation d. + II II || + Now select the labels to show the formula for breakeven point in units and then enter the amounts to calculate the breakeven point in units for each situation. (Complete all answer boxes. Abbreviation used: CM = contribution margin.) Required sales in units %3D Situation a. %3D CM per unit ( CM ratio ( Situation b. Situation c. Fixed costs Situation d. ( Variable costs Requirement 2. Compare the impact of changes in the sales price, variable costs, and fixed costs on the contribution margin per unit and the breakeven point in units. First, compare the impact of changes in the sales price, variable costs, and fixed costs on the contribution margin per unit. The contribution margin when the sales price decreases. The contribution margin when variable costs decrease. The contribution margin when the fixed costs decrease. Now, compare the impact of changes in the sales price, variable costs, and fixed costs on the breakeven point in units. The breakeven point when the sales price decreases. The breakeven point when the variable costs decrease. The breakeven point when fixed costs decrease. Choose from any list or enter any number in the input fields and then continue to the next question. Requirement 2. Compare the impact of changes in the sales price, variable costs, and fixed costs on the contribution margin per unit and the breakeven point in units. First, compare the impact of changes in the sales price, variable costs, and fixed costs on the contribution margin per unit. The contribution margin when the sales price decreases. The contribution margin when variable costs decrease. when the fixed costs decrease. decreases Now, compare the impac rice, variable costs, and fixed costs on the breakeven point in units. does not change The breakeven point sales price decreases. The breakeven point when the variable increases costs decrease. The brea when fixed costs decrease. i Requirements 1. For each of the following independent situations, calculate the contribution margin per unit and the breakeven point in units by first referring to the original data provided: а. Breakeven point with no change in information. b. Decrease sales price to $400 per student. с. Decrease variable costs to $80 per student. d. Decrease fixed costs to $123,200. 2. Compare the impact of changes in the sales price, variable costs, and fixed costs on the contribution margin per unit and the breakeven point in units. Print Done Highway Driving School charges $800 per student to prepare and administer written and driving tests. Variable costs of $240 per student include trainers' wages, study materials, and gasoline. Annual fixed costs of $151,200 include the training facility and fleet of cars. Read the requirements. Requirement 1. For each of the following independent situations, calculate the contribution margin per unit and the breakeven point in units: Begin by showing the formula for contribution margin per unit and then enter the amounts to calculate the contribution margin per unit for each situation. (Abbreviation used: CM = contribution margin.) CM per unit %3D Situation a. Situation b. Situation c. Situation d. II || I| II Requirement 1. For each of the following independent situations, calculate the contribution margin per unit and the breakeven point in units: Begin by showing the formula for contribution margin per unit and then enter the amounts to calculate the contribution margin per unit for each situation. (Abbreviation used: CM = contribution margin.) CM per unit Situation a. Fixed costs Situation b. Net sales revenue per unit Situation c. Operating income Situation d. Total variable cost Variable costs per unit Now select the lal keven point in units and then enter the amounts to calculate the breakeven point in units for each situation, (Complete all answer boxes, Abbreviation used: CM = contribution margin.) II II I| II Now select the labels to show the formula for breakeven point in units and then enter the amounts to calculate the breakeven point in units for each situation. (Complete all answer boxes. Abbreviation used: CM = contribution margin.) + Required sales in units %3D Situation a. + %3D Situation b. + Situation c. Situation d. + II II || + Now select the labels to show the formula for breakeven point in units and then enter the amounts to calculate the breakeven point in units for each situation. (Complete all answer boxes. Abbreviation used: CM = contribution margin.) Required sales in units %3D Situation a. %3D CM per unit ( CM ratio ( Situation b. Situation c. Fixed costs Situation d. ( Variable costs Requirement 2. Compare the impact of changes in the sales price, variable costs, and fixed costs on the contribution margin per unit and the breakeven point in units. First, compare the impact of changes in the sales price, variable costs, and fixed costs on the contribution margin per unit. The contribution margin when the sales price decreases. The contribution margin when variable costs decrease. The contribution margin when the fixed costs decrease. Now, compare the impact of changes in the sales price, variable costs, and fixed costs on the breakeven point in units. The breakeven point when the sales price decreases. The breakeven point when the variable costs decrease. The breakeven point when fixed costs decrease. Choose from any list or enter any number in the input fields and then continue to the next question. Requirement 2. Compare the impact of changes in the sales price, variable costs, and fixed costs on the contribution margin per unit and the breakeven point in units. First, compare the impact of changes in the sales price, variable costs, and fixed costs on the contribution margin per unit. The contribution margin when the sales price decreases. The contribution margin when variable costs decrease. when the fixed costs decrease. decreases Now, compare the impac rice, variable costs, and fixed costs on the breakeven point in units. does not change The breakeven point sales price decreases. The breakeven point when the variable increases costs decrease. The brea when fixed costs decrease. i Requirements 1. For each of the following independent situations, calculate the contribution margin per unit and the breakeven point in units by first referring to the original data provided: а. Breakeven point with no change in information. b. Decrease sales price to $400 per student. с. Decrease variable costs to $80 per student. d. Decrease fixed costs to $123,200. 2. Compare the impact of changes in the sales price, variable costs, and fixed costs on the contribution margin per unit and the breakeven point in units. Print Done Highway Driving School charges $800 per student to prepare and administer written and driving tests. Variable costs of $240 per student include trainers' wages, study materials, and gasoline. Annual fixed costs of $151,200 include the training facility and fleet of cars. Read the requirements. Requirement 1. For each of the following independent situations, calculate the contribution margin per unit and the breakeven point in units: Begin by showing the formula for contribution margin per unit and then enter the amounts to calculate the contribution margin per unit for each situation. (Abbreviation used: CM = contribution margin.) CM per unit %3D Situation a. Situation b. Situation c. Situation d. II || I| II Requirement 1. For each of the following independent situations, calculate the contribution margin per unit and the breakeven point in units: Begin by showing the formula for contribution margin per unit and then enter the amounts to calculate the contribution margin per unit for each situation. (Abbreviation used: CM = contribution margin.) CM per unit Situation a. Fixed costs Situation b. Net sales revenue per unit Situation c. Operating income Situation d. Total variable cost Variable costs per unit Now select the lal keven point in units and then enter the amounts to calculate the breakeven point in units for each situation, (Complete all answer boxes, Abbreviation used: CM = contribution margin.) II II I| II Now select the labels to show the formula for breakeven point in units and then enter the amounts to calculate the breakeven point in units for each situation. (Complete all answer boxes. Abbreviation used: CM = contribution margin.) + Required sales in units %3D Situation a. + %3D Situation b. + Situation c. Situation d. + II II || + Now select the labels to show the formula for breakeven point in units and then enter the amounts to calculate the breakeven point in units for each situation. (Complete all answer boxes. Abbreviation used: CM = contribution margin.) Required sales in units %3D Situation a. %3D CM per unit ( CM ratio ( Situation b. Situation c. Fixed costs Situation d. ( Variable costs Requirement 2. Compare the impact of changes in the sales price, variable costs, and fixed costs on the contribution margin per unit and the breakeven point in units. First, compare the impact of changes in the sales price, variable costs, and fixed costs on the contribution margin per unit. The contribution margin when the sales price decreases. The contribution margin when variable costs decrease. The contribution margin when the fixed costs decrease. Now, compare the impact of changes in the sales price, variable costs, and fixed costs on the breakeven point in units. The breakeven point when the sales price decreases. The breakeven point when the variable costs decrease. The breakeven point when fixed costs decrease. Choose from any list or enter any number in the input fields and then continue to the next question. Requirement 2. Compare the impact of changes in the sales price, variable costs, and fixed costs on the contribution margin per unit and the breakeven point in units. First, compare the impact of changes in the sales price, variable costs, and fixed costs on the contribution margin per unit. The contribution margin when the sales price decreases. The contribution margin when variable costs decrease. when the fixed costs decrease. decreases Now, compare the impac rice, variable costs, and fixed costs on the breakeven point in units. does not change The breakeven point sales price decreases. The breakeven point when the variable increases costs decrease. The brea when fixed costs decrease. i Requirements 1. For each of the following independent situations, calculate the contribution margin per unit and the breakeven point in units by first referring to the original data provided: а. Breakeven point with no change in information. b. Decrease sales price to $400 per student. с. Decrease variable costs to $80 per student. d. Decrease fixed costs to $123,200. 2. Compare the impact of changes in the sales price, variable costs, and fixed costs on the contribution margin per unit and the breakeven point in units. Print Done Highway Driving School charges $800 per student to prepare and administer written and driving tests. Variable costs of $240 per student include trainers' wages, study materials, and gasoline. Annual fixed costs of $151,200 include the training facility and fleet of cars. Read the requirements. Requirement 1. For each of the following independent situations, calculate the contribution margin per unit and the breakeven point in units: Begin by showing the formula for contribution margin per unit and then enter the amounts to calculate the contribution margin per unit for each situation. (Abbreviation used: CM = contribution margin.) CM per unit %3D Situation a. Situation b. Situation c. Situation d. II || I| II Requirement 1. For each of the following independent situations, calculate the contribution margin per unit and the breakeven point in units: Begin by showing the formula for contribution margin per unit and then enter the amounts to calculate the contribution margin per unit for each situation. (Abbreviation used: CM = contribution margin.) CM per unit Situation a. Fixed costs Situation b. Net sales revenue per unit Situation c. Operating income Situation d. Total variable cost Variable costs per unit Now select the lal keven point in units and then enter the amounts to calculate the breakeven point in units for each situation, (Complete all answer boxes, Abbreviation used: CM = contribution margin.) II II I| II Now select the labels to show the formula for breakeven point in units and then enter the amounts to calculate the breakeven point in units for each situation. (Complete all answer boxes. Abbreviation used: CM = contribution margin.) + Required sales in units %3D Situation a. + %3D Situation b. + Situation c. Situation d. + II II || + Now select the labels to show the formula for breakeven point in units and then enter the amounts to calculate the breakeven point in units for each situation. (Complete all answer boxes. Abbreviation used: CM = contribution margin.) Required sales in units %3D Situation a. %3D CM per unit ( CM ratio ( Situation b. Situation c. Fixed costs Situation d. ( Variable costs Requirement 2. Compare the impact of changes in the sales price, variable costs, and fixed costs on the contribution margin per unit and the breakeven point in units. First, compare the impact of changes in the sales price, variable costs, and fixed costs on the contribution margin per unit. The contribution margin when the sales price decreases. The contribution margin when variable costs decrease. The contribution margin when the fixed costs decrease. Now, compare the impact of changes in the sales price, variable costs, and fixed costs on the breakeven point in units. The breakeven point when the sales price decreases. The breakeven point when the variable costs decrease. The breakeven point when fixed costs decrease. Choose from any list or enter any number in the input fields and then continue to the next question. Requirement 2. Compare the impact of changes in the sales price, variable costs, and fixed costs on the contribution margin per unit and the breakeven point in units. First, compare the impact of changes in the sales price, variable costs, and fixed costs on the contribution margin per unit. The contribution margin when the sales price decreases. The contribution margin when variable costs decrease. when the fixed costs decrease. decreases Now, compare the impac rice, variable costs, and fixed costs on the breakeven point in units. does not change The breakeven point sales price decreases. The breakeven point when the variable increases costs decrease. The brea when fixed costs decrease. i Requirements 1. For each of the following independent situations, calculate the contribution margin per unit and the breakeven point in units by first referring to the original data provided: а. Breakeven point with no change in information. b. Decrease sales price to $400 per student. с. Decrease variable costs to $80 per student. d. Decrease fixed costs to $123,200. 2. Compare the impact of changes in the sales price, variable costs, and fixed costs on the contribution margin per unit and the breakeven point in units. Print Done Highway Driving School charges $800 per student to prepare and administer written and driving tests. Variable costs of $240 per student include trainers' wages, study materials, and gasoline. Annual fixed costs of $151,200 include the training facility and fleet of cars. Read the requirements. Requirement 1. For each of the following independent situations, calculate the contribution margin per unit and the breakeven point in units: Begin by showing the formula for contribution margin per unit and then enter the amounts to calculate the contribution margin per unit for each situation. (Abbreviation used: CM = contribution margin.) CM per unit %3D Situation a. Situation b. Situation c. Situation d. II || I| II Requirement 1. For each of the following independent situations, calculate the contribution margin per unit and the breakeven point in units: Begin by showing the formula for contribution margin per unit and then enter the amounts to calculate the contribution margin per unit for each situation. (Abbreviation used: CM = contribution margin.) CM per unit Situation a. Fixed costs Situation b. Net sales revenue per unit Situation c. Operating income Situation d. Total variable cost Variable costs per unit Now select the lal keven point in units and then enter the amounts to calculate the breakeven point in units for each situation, (Complete all answer boxes, Abbreviation used: CM = contribution margin.) II II I| II Now select the labels to show the formula for breakeven point in units and then enter the amounts to calculate the breakeven point in units for each situation. (Complete all answer boxes. Abbreviation used: CM = contribution margin.) + Required sales in units %3D Situation a. + %3D Situation b. + Situation c. Situation d. + II II || + Now select the labels to show the formula for breakeven point in units and then enter the amounts to calculate the breakeven point in units for each situation. (Complete all answer boxes. Abbreviation used: CM = contribution margin.) Required sales in units %3D Situation a. %3D CM per unit ( CM ratio ( Situation b. Situation c. Fixed costs Situation d. ( Variable costs Requirement 2. Compare the impact of changes in the sales price, variable costs, and fixed costs on the contribution margin per unit and the breakeven point in units. First, compare the impact of changes in the sales price, variable costs, and fixed costs on the contribution margin per unit. The contribution margin when the sales price decreases. The contribution margin when variable costs decrease. The contribution margin when the fixed costs decrease. Now, compare the impact of changes in the sales price, variable costs, and fixed costs on the breakeven point in units. The breakeven point when the sales price decreases. The breakeven point when the variable costs decrease. The breakeven point when fixed costs decrease. Choose from any list or enter any number in the input fields and then continue to the next question. Requirement 2. Compare the impact of changes in the sales price, variable costs, and fixed costs on the contribution margin per unit and the breakeven point in units. First, compare the impact of changes in the sales price, variable costs, and fixed costs on the contribution margin per unit. The contribution margin when the sales price decreases. The contribution margin when variable costs decrease. when the fixed costs decrease. decreases Now, compare the impac rice, variable costs, and fixed costs on the breakeven point in units. does not change The breakeven point sales price decreases. The breakeven point when the variable increases costs decrease. The brea when fixed costs decrease. i Requirements 1. For each of the following independent situations, calculate the contribution margin per unit and the breakeven point in units by first referring to the original data provided: а. Breakeven point with no change in information. b. Decrease sales price to $400 per student. с. Decrease variable costs to $80 per student. d. Decrease fixed costs to $123,200. 2. Compare the impact of changes in the sales price, variable costs, and fixed costs on the contribution margin per unit and the breakeven point in units. Print Done Highway Driving School charges $800 per student to prepare and administer written and driving tests. Variable costs of $240 per student include trainers' wages, study materials, and gasoline. Annual fixed costs of $151,200 include the training facility and fleet of cars. Read the requirements. Requirement 1. For each of the following independent situations, calculate the contribution margin per unit and the breakeven point in units: Begin by showing the formula for contribution margin per unit and then enter the amounts to calculate the contribution margin per unit for each situation. (Abbreviation used: CM = contribution margin.) CM per unit %3D Situation a. Situation b. Situation c. Situation d. II || I| II Requirement 1. For each of the following independent situations, calculate the contribution margin per unit and the breakeven point in units: Begin by showing the formula for contribution margin per unit and then enter the amounts to calculate the contribution margin per unit for each situation. (Abbreviation used: CM = contribution margin.) CM per unit Situation a. Fixed costs Situation b. Net sales revenue per unit Situation c. Operating income Situation d. Total variable cost Variable costs per unit Now select the lal keven point in units and then enter the amounts to calculate the breakeven point in units for each situation, (Complete all answer boxes, Abbreviation used: CM = contribution margin.) II II I| II Now select the labels to show the formula for breakeven point in units and then enter the amounts to calculate the breakeven point in units for each situation. (Complete all answer boxes. Abbreviation used: CM = contribution margin.) + Required sales in units %3D Situation a. + %3D Situation b. + Situation c. Situation d. + II II || + Now select the labels to show the formula for breakeven point in units and then enter the amounts to calculate the breakeven point in units for each situation. (Complete all answer boxes. Abbreviation used: CM = contribution margin.) Required sales in units %3D Situation a. %3D CM per unit ( CM ratio ( Situation b. Situation c. Fixed costs Situation d. ( Variable costs Requirement 2. Compare the impact of changes in the sales price, variable costs, and fixed costs on the contribution margin per unit and the breakeven point in units. First, compare the impact of changes in the sales price, variable costs, and fixed costs on the contribution margin per unit. The contribution margin when the sales price decreases. The contribution margin when variable costs decrease. The contribution margin when the fixed costs decrease. Now, compare the impact of changes in the sales price, variable costs, and fixed costs on the breakeven point in units. The breakeven point when the sales price decreases. The breakeven point when the variable costs decrease. The breakeven point when fixed costs decrease. Choose from any list or enter any number in the input fields and then continue to the next question. Requirement 2. Compare the impact of changes in the sales price, variable costs, and fixed costs on the contribution margin per unit and the breakeven point in units. First, compare the impact of changes in the sales price, variable costs, and fixed costs on the contribution margin per unit. The contribution margin when the sales price decreases. The contribution margin when variable costs decrease. when the fixed costs decrease. decreases Now, compare the impac rice, variable costs, and fixed costs on the breakeven point in units. does not change The breakeven point sales price decreases. The breakeven point when the variable increases costs decrease. The brea when fixed costs decrease. i Requirements 1. For each of the following independent situations, calculate the contribution margin per unit and the breakeven point in units by first referring to the original data provided: а. Breakeven point with no change in information. b. Decrease sales price to $400 per student. с. Decrease variable costs to $80 per student. d. Decrease fixed costs to $123,200. 2. Compare the impact of changes in the sales price, variable costs, and fixed costs on the contribution margin per unit and the breakeven point in units. Print Done Highway Driving School charges $800 per student to prepare and administer written and driving tests. Variable costs of $240 per student include trainers' wages, study materials, and gasoline. Annual fixed costs of $151,200 include the training facility and fleet of cars. Read the requirements. Requirement 1. For each of the following independent situations, calculate the contribution margin per unit and the breakeven point in units: Begin by showing the formula for contribution margin per unit and then enter the amounts to calculate the contribution margin per unit for each situation. (Abbreviation used: CM = contribution margin.) CM per unit %3D Situation a. Situation b. Situation c. Situation d. II || I| II Requirement 1. For each of the following independent situations, calculate the contribution margin per unit and the breakeven point in units: Begin by showing the formula for contribution margin per unit and then enter the amounts to calculate the contribution margin per unit for each situation. (Abbreviation used: CM = contribution margin.) CM per unit Situation a. Fixed costs Situation b. Net sales revenue per unit Situation c. Operating income Situation d. Total variable cost Variable costs per unit Now select the lal keven point in units and then enter the amounts to calculate the breakeven point in units for each situation, (Complete all answer boxes, Abbreviation used: CM = contribution margin.) II II I| II Now select the labels to show the formula for breakeven point in units and then enter the amounts to calculate the breakeven point in units for each situation. (Complete all answer boxes. Abbreviation used: CM = contribution margin.) + Required sales in units %3D Situation a. + %3D Situation b. + Situation c. Situation d. + II II || + Now select the labels to show the formula for breakeven point in units and then enter the amounts to calculate the breakeven point in units for each situation. (Complete all answer boxes. Abbreviation used: CM = contribution margin.) Required sales in units %3D Situation a. %3D CM per unit ( CM ratio ( Situation b. Situation c. Fixed costs Situation d. ( Variable costs Requirement 2. Compare the impact of changes in the sales price, variable costs, and fixed costs on the contribution margin per unit and the breakeven point in units. First, compare the impact of changes in the sales price, variable costs, and fixed costs on the contribution margin per unit. The contribution margin when the sales price decreases. The contribution margin when variable costs decrease. The contribution margin when the fixed costs decrease. Now, compare the impact of changes in the sales price, variable costs, and fixed costs on the breakeven point in units. The breakeven point when the sales price decreases. The breakeven point when the variable costs decrease. The breakeven point when fixed costs decrease. Choose from any list or enter any number in the input fields and then continue to the next question. Requirement 2. Compare the impact of changes in the sales price, variable costs, and fixed costs on the contribution margin per unit and the breakeven point in units. First, compare the impact of changes in the sales price, variable costs, and fixed costs on the contribution margin per unit. The contribution margin when the sales price decreases. The contribution margin when variable costs decrease. when the fixed costs decrease. decreases Now, compare the impac rice, variable costs, and fixed costs on the breakeven point in units. does not change The breakeven point sales price decreases. The breakeven point when the variable increases costs decrease. The brea when fixed costs decrease. i Requirements 1. For each of the following independent situations, calculate the contribution margin per unit and the breakeven point in units by first referring to the original data provided: а. Breakeven point with no change in information. b. Decrease sales price to $400 per student. с. Decrease variable costs to $80 per student. d. Decrease fixed costs to $123,200. 2. Compare the impact of changes in the sales price, variable costs, and fixed costs on the contribution margin per unit and the breakeven point in units. Print Done

Expert Answer:

Related Book For

Financial and Managerial Accounting

ISBN: 978-0538480895

11th Edition

Authors: Jonathan E. Duchac, James M. Reeve, Carl S. Warren

Posted Date:

Students also viewed these finance questions

-

Figure 1 below shows the price and other information of an Apple bond from the site Investing.com Figure 1: Apple 3.85% bond information (from Investing.com) as of 22 July 2022 Apple Inc AAPL 3.85%...

-

Intersection Driving School charges $500 per student to prepare and administer written and driving tests. Variable costs of $150 per student include trainers wages, study materials, and gasoline....

-

Calculate the missing information for each of the following independent cases: Deginning Cost of Goods Ending Inventory Ending Inventory Cases Inry Purchases Sold (perpetual system) ( (as counted...

-

Wynn Resorts owns a variety of popular gaming resorts. Its annual report contained the following information: Debenture Conversions Our convertible debentures are currently convertible at each...

-

What are the three sections of the cash budget?

-

Using Fig. 4.89 , design a problem to help other students better understand source transformation. Apply source transformation to determine v o and i o in the circuit in Fig. 4.89 . R, vo R2

-

Can the project manager and the systems analyst be the same? Explain your answer.

-

An off-duty, out-of-uniform police officer and his son purchased some food from a 7- Eleven store and were still in the parking lot when a carload of teenagers became rowdy. The officer went to speak...

-

Who and what defines professionalism? As emerging leaders in the field, it will be your role to set the standard - the bar - for those who follow in your footsteps. As with children, modeling for...

-

A. Describe some of the attributes of an ideal risk indicator for stock market investors. B. On the Internet, go to Yahoo! Finance (or msn Money) and download weekly price information over the past...

-

Discuss how Artificial intelligence (AI) can add value to the customer journey?

-

Recalculate the cyclomatic complexity metric for the if-then-else , while , and until structures depicted in Figure 8.1 . Figure 8.1 sequence if-then-else case while until

-

What itre the reengineering tools suggested in the textbook?

-

Fill in the blanks: a. The final. on whether the system is correctly and ready for implemen- tation is the b. The key input in to the phase is the phase. c. The is completed d. Once the. complete.....

-

How do you explain the use of countertrade? Under what scenarios might its use increase further by 2015? Under what scenarios might its use decline?

-

Consider a preemptive priority system. The three tasks in the system, time needed to complete, and priority are given below: If the tasks arrive in the order 1 , 2 , 3 , what is the time needed to...

-

3. (15) Consider the same closed flow line as before (the first station has a processing time of 2 minutes, the second one a processing time of 1 minute, and the third a processing time of 3...

-

The cost curve for the city water supply is C(Q) = 16 + 1/4 Q2, where Q is the amount of water supplied and C(Q) is the cost of providing Q acre-feet of water. (An acre-foot is the amount of water...

-

The Commercial division of Morse Company has income from operations of $160,000 and assets of $700,000. The minimum acceptable rate of return on assets is 9%. What is the residual income for the...

-

Identify the errors in the following incomestatement: Keepsakes Company Income Statement For the Year Ended February 29, 2012 Revenue from sales: $7,200.000 Sales... Add: Sales returns and allowances...

-

How does the use of the materials requisition help control the issuance of materials from the storeroom? Discuss.

-

Graph the discrete probability distribution given in Table 1 from Example 2. Approach In the graph of a discrete probability distribution, the horizontal axis represents the values of the discrete...

-

Compute the mean of the discrete random variable given in Table 1 from Example 2. Approach Find the mean of a discrete random variable by multiplying each value of the random variable by its...

-

Which of the following is a discrete probability distribution? Approach In a discrete probability distribution, the sum of the probabilities must equal 1, and all probabilities must be between 0 and...

Study smarter with the SolutionInn App