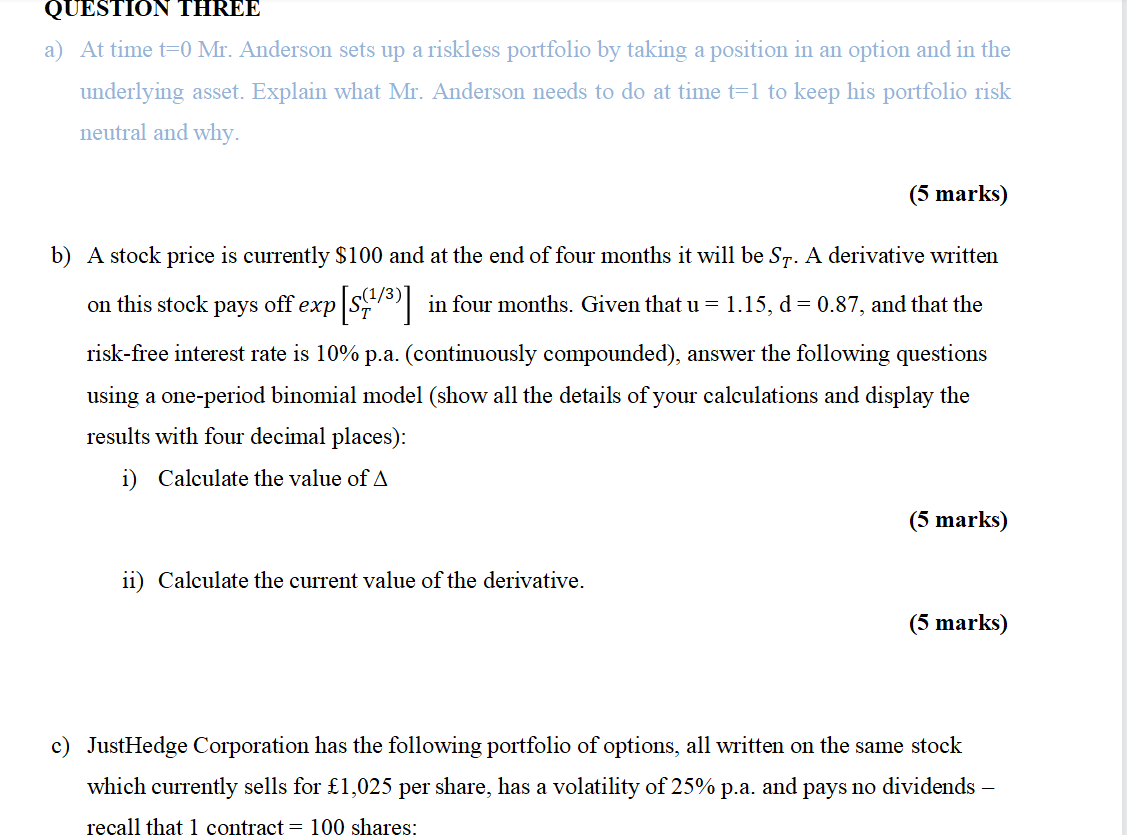

Question: QUESTION THREE a) At time t=0 Mr. Anderson sets up a riskless portfolio by taking a position in an option and in the underlying asset.

QUESTION THREE a) At time t=0 Mr. Anderson sets up a riskless portfolio by taking a position in an option and in the underlying asset. Explain what Mr. Anderson needs to do at time t=1 to keep his portfolio risk neutral and why. (5 marks) b) A stock price is currently $100 and at the end of four months it will be St. A derivative written on this stock pays off exp [s

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock