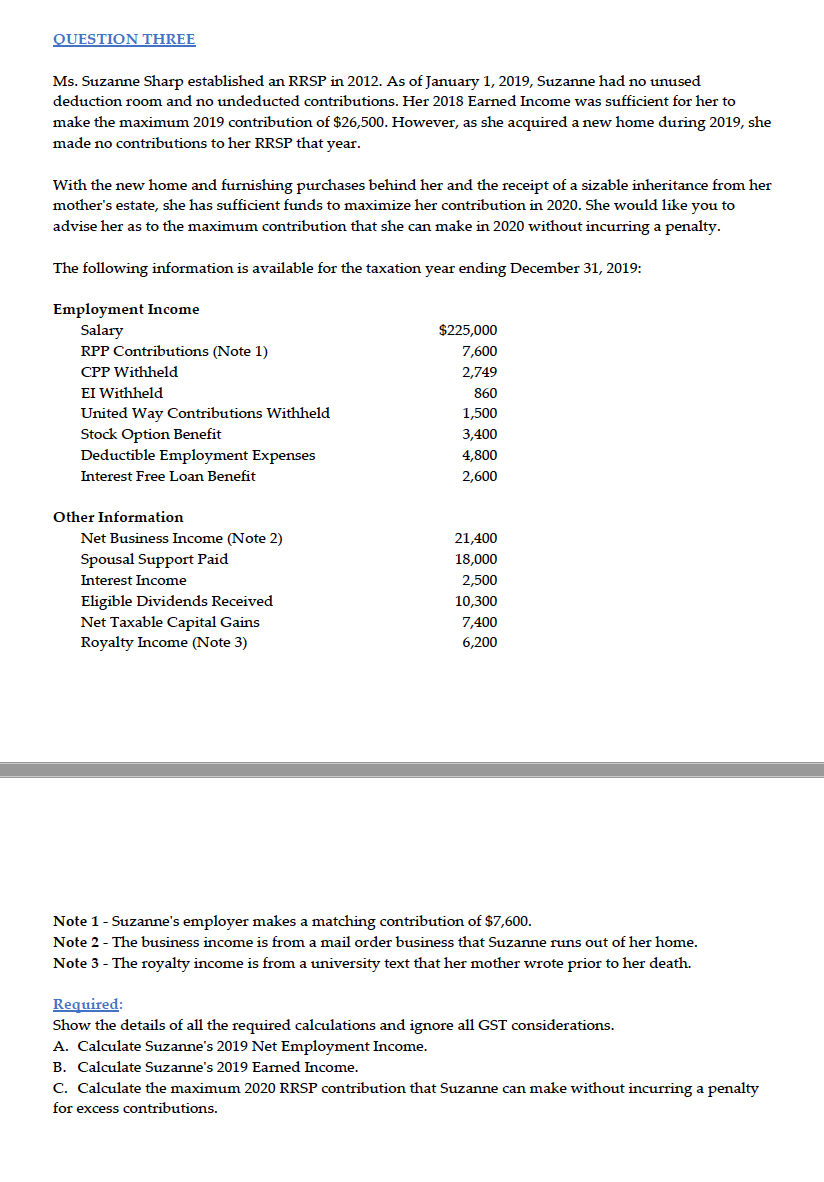

Question: QUESTION THREE Ms. Suzanne Sharp established an RRSP in 2012. As of January 1, 2019, Suzanne had no unused deduction room and no undeducted contributions.

QUESTION THREE Ms. Suzanne Sharp established an RRSP in 2012. As of January 1, 2019, Suzanne had no unused deduction room and no undeducted contributions. Her 2018 Earned Income was sufficient for her to make the maximum 2019 contribution of $26,500. However, as she acquired a new home during 2019, she made no contributions to her RRSP that year. With the new home and furnishing purchases behind her and the receipt of a sizable inheritance from her mother's estate, she has sufficient funds to maximize her contribution in 2020. She would like you to advise her as to the maximum contribution that she can make in 2020 without incurring a penalty. The following information is available for the taxation year ending December 31, 2019: Employment Income Salary RPP Contributions (Note 1) CPP Withheld EI Withheld United Way Contributions Withheld Stock Option Benefit Deductible Employment Expenses Interest Free Loan Benefit $225,000 7,600 2,749 860 1,500 3,400 4,800 2,600 Other Information Net Business Income (Note 2) Spousal Support Paid Interest Income Eligible Dividends Received Net Taxable Capital Gains Royalty Income (Note 3) 21,400 18,000 2,500 10,300 7,400 6,200 Note 1 - Suzanne's employer makes a matching contribution of $7,600. Note 2 - The business income is from a mail order business that Suzanne runs out of her home. Note 3 - The royalty income is from a university text that her mother wrote prior to her death. Required: Show the details of all the required calculations and ignore all GST considerations. A. Calculate Suzanne's 2019 Net Employment Income. B. Calculate Suzanne's 2019 Earned Income. C. Calculate the maximum 2020 RRSP contribution that Suzanne can make without incurring a penalty for excess contributions. QUESTION THREE Ms. Suzanne Sharp established an RRSP in 2012. As of January 1, 2019, Suzanne had no unused deduction room and no undeducted contributions. Her 2018 Earned Income was sufficient for her to make the maximum 2019 contribution of $26,500. However, as she acquired a new home during 2019, she made no contributions to her RRSP that year. With the new home and furnishing purchases behind her and the receipt of a sizable inheritance from her mother's estate, she has sufficient funds to maximize her contribution in 2020. She would like you to advise her as to the maximum contribution that she can make in 2020 without incurring a penalty. The following information is available for the taxation year ending December 31, 2019: Employment Income Salary RPP Contributions (Note 1) CPP Withheld EI Withheld United Way Contributions Withheld Stock Option Benefit Deductible Employment Expenses Interest Free Loan Benefit $225,000 7,600 2,749 860 1,500 3,400 4,800 2,600 Other Information Net Business Income (Note 2) Spousal Support Paid Interest Income Eligible Dividends Received Net Taxable Capital Gains Royalty Income (Note 3) 21,400 18,000 2,500 10,300 7,400 6,200 Note 1 - Suzanne's employer makes a matching contribution of $7,600. Note 2 - The business income is from a mail order business that Suzanne runs out of her home. Note 3 - The royalty income is from a university text that her mother wrote prior to her death. Required: Show the details of all the required calculations and ignore all GST considerations. A. Calculate Suzanne's 2019 Net Employment Income. B. Calculate Suzanne's 2019 Earned Income. C. Calculate the maximum 2020 RRSP contribution that Suzanne can make without incurring a penalty for excess contributions

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts