Question: QUESTIONS If Fly-by-Night decides to upgrade its fleet by using the PJ-2 exclusively, how many PJ-2 planes will it need to buy to meet the

QUESTIONS

If Fly-by-Night decides to upgrade its fleet by using the PJ-2 exclusively, how many PJ-2 planes will it need to buy to meet the federal government regulation requiring that an airline serving the Los Angeles New York route has the capability of carrying a minimum of 300,000 passengers per year? If the company decides to use PJ-3 exclusively, how many PJ-3 planes will it need to buy to meet this federal regulation? (Notice that the actual number of passengers that Fly-by-Night expects to carry is slightly higher if it uses the PJ-2 or PJ-3 than it presently carries using the PJ-1. The reason is that the larger- capacity planes will allow it to eliminate some of the overbooking problems it now faces with the PJ-1 during holiday periods. However, management feels that Fly-by-Night cannot significantly increase its ridership by buying increased capacity.)

Compute the net present value of the replacement option. First compute the ticket revenues that would be generated in each year over the 15-year horizon. Then compute the total operating costs that would be generated in each year over the same horizon. Operating costs include fuel, maintenance, upgrading, and personnel expenditures. Then estimate the depreciation charges and taxes. Finally, compute the total cash flow for each year. If the firm suffers a loss in any year in its Los Angeles New York operations, assume that it has other income in that year from which the loss can be deduced for tax purposes. Dont forget to add purchases of new planes and after-tax salvage values of old planes and other relevant incremental cash flows, e.g., opportunity cost of using currently owned PJ-1s, etc.

What would happen to the NPV of the replacement option if Fly-by-Night uses accelerated depreciation instead of straight-line depreciation? (No calculation necessary, briefly explain.)

What would happen to the NPV of the replacement option if the rate of inflation increases? (No calculation necessary, briefly explain.)

Compute the net present value for an option of not replacing and using old PJ-1s for the next 15 years.

Should James Baron go with the replacement option? What is the incremental NPV of the replacement decision (difference between the replacement option NPV as in part 2 and the not replacing option

NPV as in part 5)?

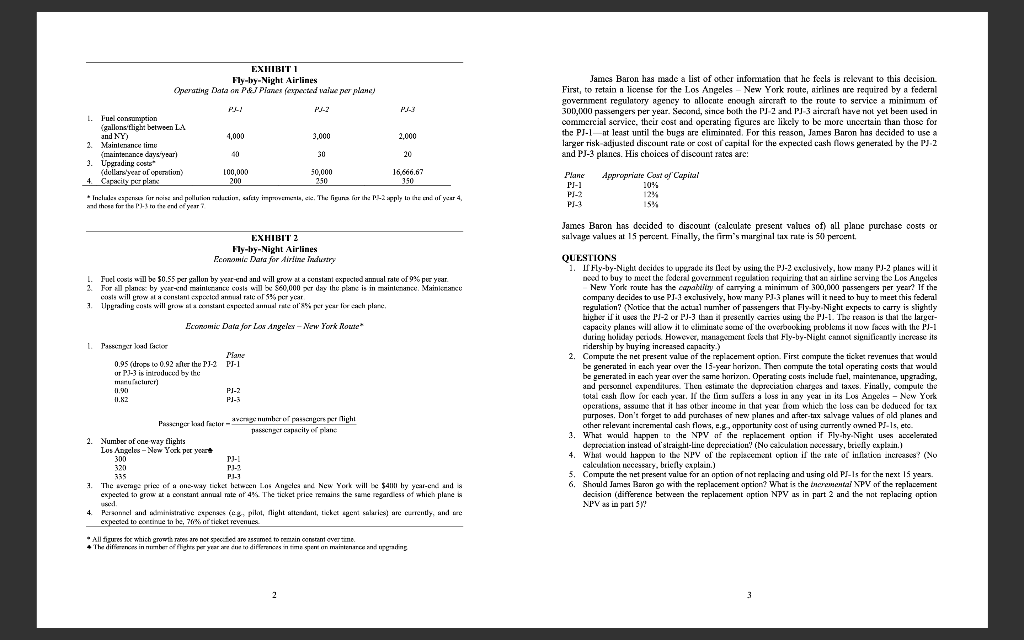

Fly-by-Night Airines Fly-by-Night Airliscs is a major commercial air carricr offcring passenger service between most large citics in the United States. One of its more profitable routes is between Los Angeles and New York. Competition on this roure is intense, and James Briron, supervisor of transcontinetal operations for fily-by-Night, is considering upgrating the quality of the fleet of airirall used on the Los Angeles - New York nul. As it has in the post, Fly-by-Night plans to purchase nll its planes fion P\&J Aircraft Company. P\&J markets three nircraft: (1) the old reliable PJ-1, for the lnst ten years the workhorse of the airline industry; (2) the soon-to-be intocluced P.J-2, currently in the test flight stige; and (3) the tcehnologically advaneed PJ-3, still in the design stage. Although PJ-2 and PJ-3 will not be nvnilable for service motil sometime in the futhire, P\&J is now tnking contingeney orders for these planes. It Fily by-Night is to have amy hope liot prompl delivery, it must order the planes today, even though it will not take clelivery or pay for them until sometime in the fulure. Fily-hy-Night is very interested in the oxwer models bocause thxy arc more fucl efficient and loss polluting reguire less mainteanoce, nod are mach quieter thou the old PJ1. Iily hy-Night currently uses live J-1 planes to service its loss Anyeles New York toule. These plancs were purchasod 10 years ago for a cost of $15 mullion per plabc; cach is being depreciated on a straight-line bnsis to a salvnge value of zero 0 ver a 25 -ye coovomic life from the tiste of purchase. Each PJ-1 plame ccuuld be sold curremtly at a market value of $8mrillicm. This market price for the PJ1 is expected to drop to $5 million by the cad of third year. James Baron is considering replacing the PJ-1 planes with cither the PJ-2 or the PJ-3. The PJ-2 will be available for delivery in three years and could gecernte its first cash flow from commencial service in the fourth year. The PJ-3 will be available for tielivery in six years and could generate its fust eash flow in the seventh year. To make an infonned decision, James Baron wants to know the NPV of the replacement option. He is using 15-year planoing borizon for his analysis. Under this replacemeat option, the firm will continue to use the PJ-1s fior three mure years, replace thern with the PJ-2s at the erxl of the third year and use those PJ-2s for 3 years after that, and then replace tho PJ-2s with the PJ-3s at the end of the sixth year, which will then be used for the remninder of the horizon 9 years. The purchase price for PJ-2 three years from now will be $20 million. This cast will he doprociatod on a straighteline basis over 12 years to a salvage value of $8 million. The P'J-2 is expocted to bave a market value at the end of the sixth year of $18 mullion. Six years from fiow, when the PJ-3 becomes available, it will cost 530 million per plane and will be depreciated on a straight-line hasis over nine years to a salvage value of $12 millom. To assist him in making this docision. James Baron has obtainod the data showit in Exhitrits I and 2 from acrospace eagineers at P&J and from tansportation cconomists at Fly-by-Night. The passeuger lood factors cone from a careful abalysis of future deanand and supply conditions and the begree af oxmpetition on the Las Angeles New York moute. Fly-by-Nights transportativa ecoromists feel that it is quite likely that the major oxmpetitors setving this romte will eventually all convert to the newer aircraft and that, to remnin competitive, Fly-by-Night will eveatually have to bo the same. They are umcertain whether the PJ-2 in PJ-3 will hecoime the mure popular plane, hut they feel that correctly guessinus which plane will gain long-num alceptance hy the flying public may be the key ko any change in market share on this roule. The future price of fuel is likely to be the key deterninast of the futare relative efficiebcy of these two pases. In geaera], however, the economists believe it will be very diflicult fior firms operating the l.os Anyeles - Vew York to change theit market share sulstantially in the fulure. James Baron has made a list of ocler information that he focls is relkvant to this decisjor First, to retain a license for the Los Angeles - New York route, airlines nre required by a federal government regulatory agency to nllocate enough aircraft to the route to service a minimum of 300,110 passengers per year. Secondi, since boch the P22 andl P2J3 airctat have not yet been Lsed in commercial service, their cost and operating figures are likely to be more unocrtain than those for the PJ-1 - it least uotil the bugs are eliminnted. For this resson, James Baron hns decided to use a larger risk-atljusted distount rate on eosst of capital for the expected cash flows generaled by the IJ. 2 and PJ3 planes. His choices of discount rates are: and these for the P.j. ta the end ef your 7 Fly-by-Night Airines Fly-by-Night Airliscs is a major commercial air carricr offcring passenger service between most large citics in the United States. One of its more profitable routes is between Los Angeles and New York. Competition on this roure is intense, and James Briron, supervisor of transcontinetal operations for fily-by-Night, is considering upgrating the quality of the fleet of airirall used on the Los Angeles - New York nul. As it has in the post, Fly-by-Night plans to purchase nll its planes fion P\&J Aircraft Company. P\&J markets three nircraft: (1) the old reliable PJ-1, for the lnst ten years the workhorse of the airline industry; (2) the soon-to-be intocluced P.J-2, currently in the test flight stige; and (3) the tcehnologically advaneed PJ-3, still in the design stage. Although PJ-2 and PJ-3 will not be nvnilable for service motil sometime in the futhire, P\&J is now tnking contingeney orders for these planes. It Fily by-Night is to have amy hope liot prompl delivery, it must order the planes today, even though it will not take clelivery or pay for them until sometime in the fulure. Fily-hy-Night is very interested in the oxwer models bocause thxy arc more fucl efficient and loss polluting reguire less mainteanoce, nod are mach quieter thou the old PJ1. Iily hy-Night currently uses live J-1 planes to service its loss Anyeles New York toule. These plancs were purchasod 10 years ago for a cost of $15 mullion per plabc; cach is being depreciated on a straight-line bnsis to a salvnge value of zero 0 ver a 25 -ye coovomic life from the tiste of purchase. Each PJ-1 plame ccuuld be sold curremtly at a market value of $8mrillicm. This market price for the PJ1 is expected to drop to $5 million by the cad of third year. James Baron is considering replacing the PJ-1 planes with cither the PJ-2 or the PJ-3. The PJ-2 will be available for delivery in three years and could gecernte its first cash flow from commencial service in the fourth year. The PJ-3 will be available for tielivery in six years and could generate its fust eash flow in the seventh year. To make an infonned decision, James Baron wants to know the NPV of the replacement option. He is using 15-year planoing borizon for his analysis. Under this replacemeat option, the firm will continue to use the PJ-1s fior three mure years, replace thern with the PJ-2s at the erxl of the third year and use those PJ-2s for 3 years after that, and then replace tho PJ-2s with the PJ-3s at the end of the sixth year, which will then be used for the remninder of the horizon 9 years. The purchase price for PJ-2 three years from now will be $20 million. This cast will he doprociatod on a straighteline basis over 12 years to a salvage value of $8 million. The P'J-2 is expocted to bave a market value at the end of the sixth year of $18 mullion. Six years from fiow, when the PJ-3 becomes available, it will cost 530 million per plane and will be depreciated on a straight-line hasis over nine years to a salvage value of $12 millom. To assist him in making this docision. James Baron has obtainod the data showit in Exhitrits I and 2 from acrospace eagineers at P&J and from tansportation cconomists at Fly-by-Night. The passeuger lood factors cone from a careful abalysis of future deanand and supply conditions and the begree af oxmpetition on the Las Angeles New York moute. Fly-by-Nights transportativa ecoromists feel that it is quite likely that the major oxmpetitors setving this romte will eventually all convert to the newer aircraft and that, to remnin competitive, Fly-by-Night will eveatually have to bo the same. They are umcertain whether the PJ-2 in PJ-3 will hecoime the mure popular plane, hut they feel that correctly guessinus which plane will gain long-num alceptance hy the flying public may be the key ko any change in market share on this roule. The future price of fuel is likely to be the key deterninast of the futare relative efficiebcy of these two pases. In geaera], however, the economists believe it will be very diflicult fior firms operating the l.os Anyeles - Vew York to change theit market share sulstantially in the fulure. James Baron has made a list of ocler information that he focls is relkvant to this decisjor First, to retain a license for the Los Angeles - New York route, airlines nre required by a federal government regulatory agency to nllocate enough aircraft to the route to service a minimum of 300,110 passengers per year. Secondi, since boch the P22 andl P2J3 airctat have not yet been Lsed in commercial service, their cost and operating figures are likely to be more unocrtain than those for the PJ-1 - it least uotil the bugs are eliminnted. For this resson, James Baron hns decided to use a larger risk-atljusted distount rate on eosst of capital for the expected cash flows generaled by the IJ. 2 and PJ3 planes. His choices of discount rates are: and these for the P.j. ta the end ef your 7

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts