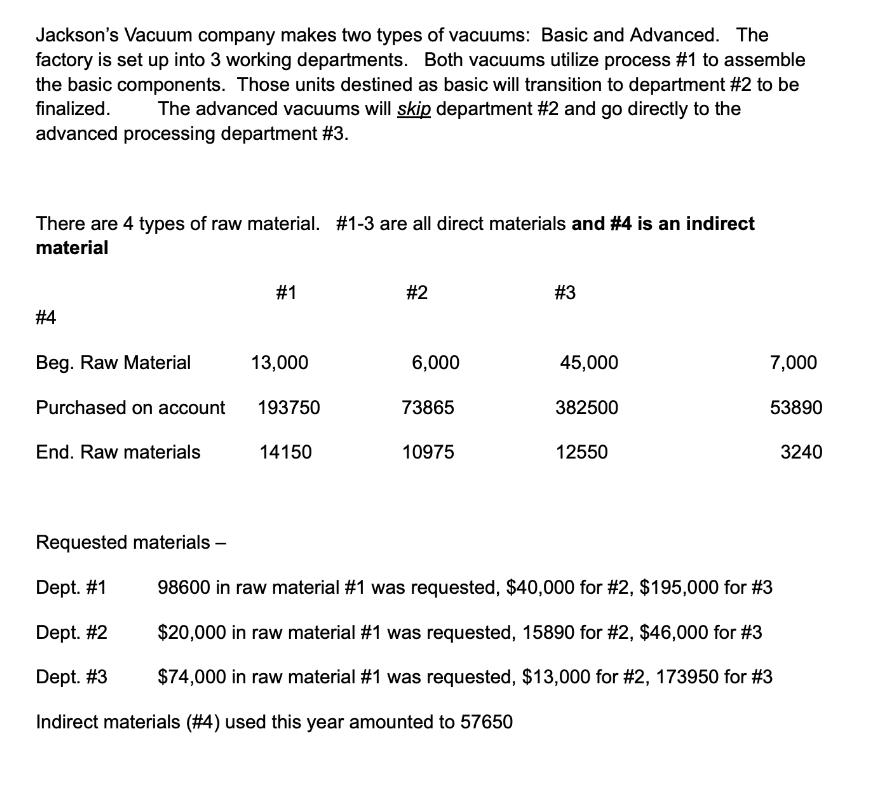

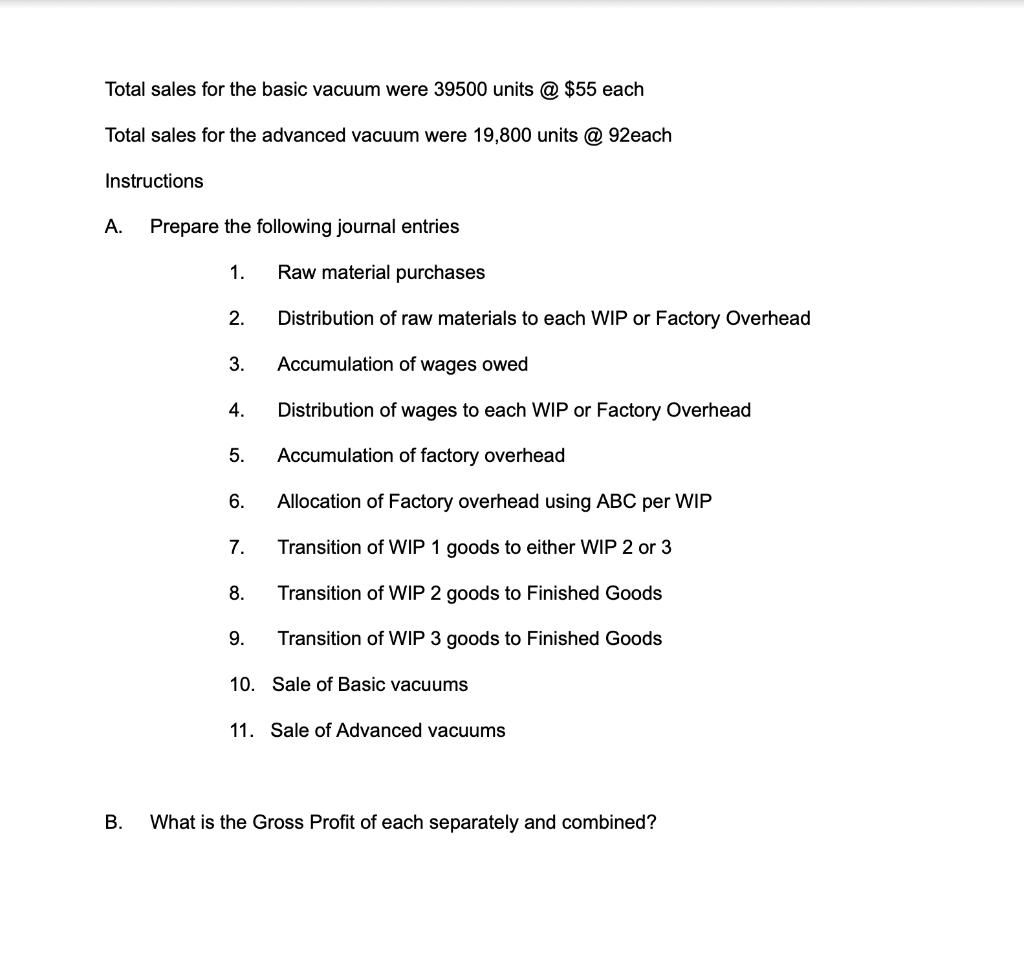

Jackson's Vacuum company makes two types of vacuums: Basic and Advanced. The factory is set up...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

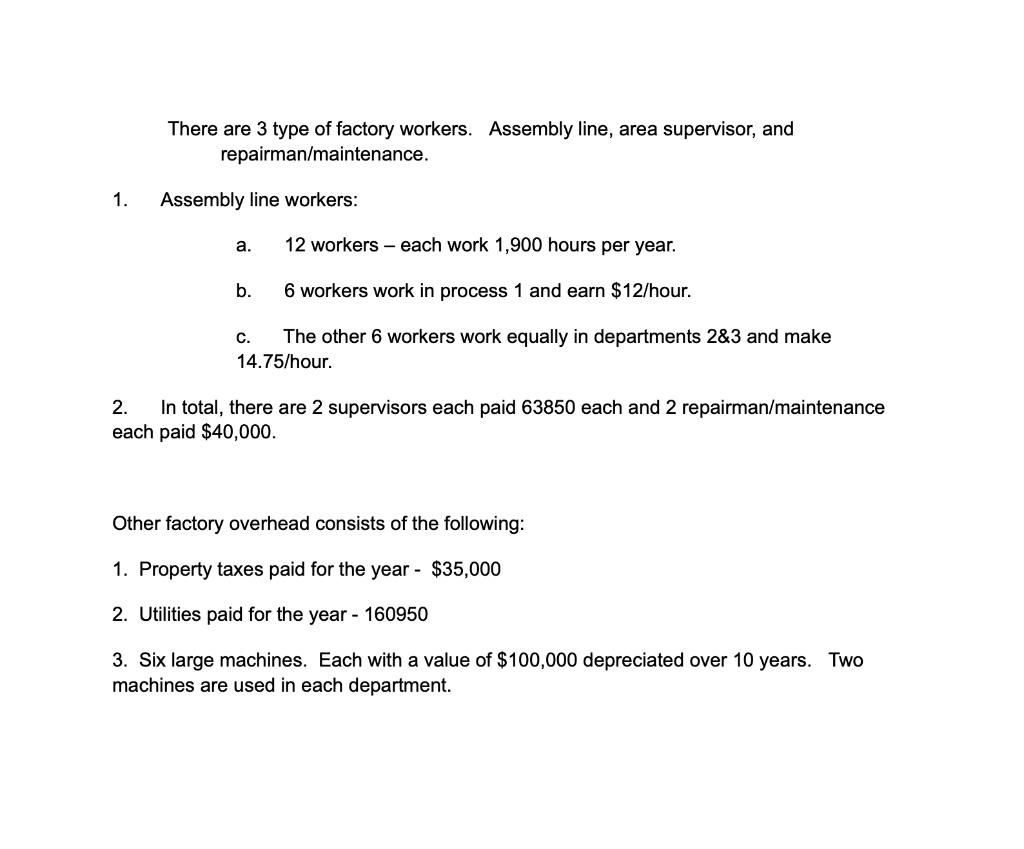

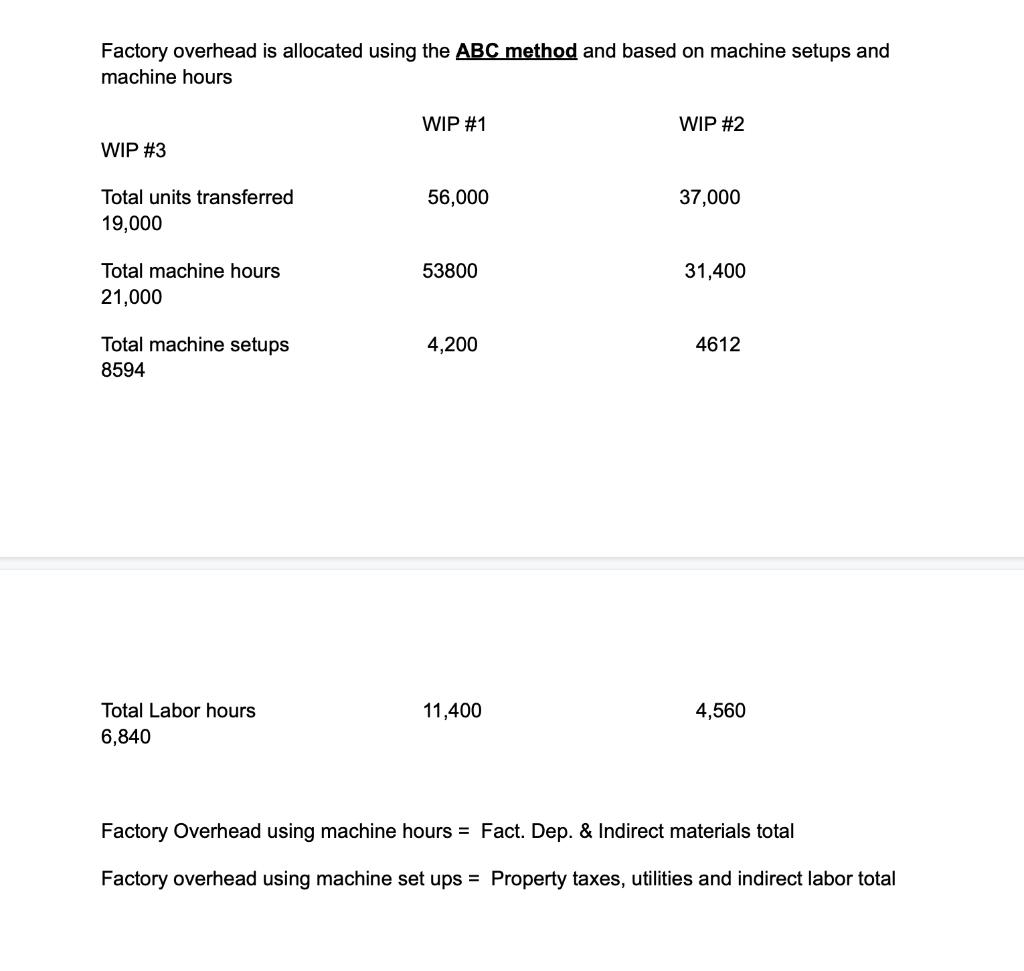

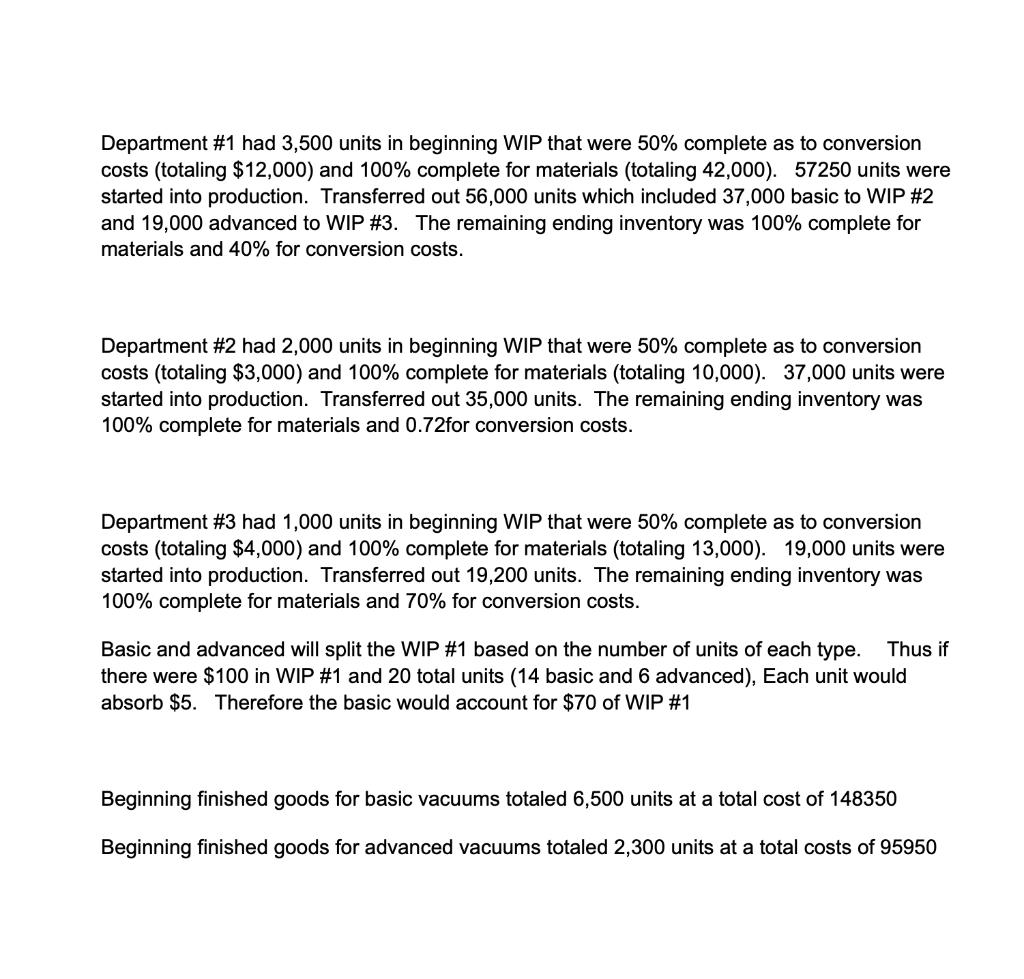

Jackson's Vacuum company makes two types of vacuums: Basic and Advanced. The factory is set up into 3 working departments. Both vacuums utilize process #1 to assemble the basic components. Those units destined as basic will transition to department #2 to be finalized. The advanced vacuums will skip department #2 and go directly to the advanced processing department #3. There are 4 types of raw material. #1-3 are all direct materials and # 4 is an indirect material #4 Beg. Raw Material Purchased on account End. Raw materials #1 13,000 193750 14150 #2 6,000 73865 10975 #3 45,000 382500 12550 7,000 53890 Requested materials - Dept. #1 Dept. #2 98600 in raw material #1 was requested, $40,000 for #2, $195,000 for #3 $20,000 in raw material #1 was requested, 15890 for #2, $46,000 for #3 $74,000 in raw material #1 was requested, $13,000 for #2, 173950 for #3 Indirect materials (#4) used this year amounted to 57650 Dept. #3 3240 1. There are 3 type of factory workers. Assembly line, area supervisor, and repairman/maintenance. Assembly line workers: 12 workers each work 1,900 hours per year. 6 workers work in process 1 and earn $12/hour. The other 6 workers work equally in departments 2&3 and make 14.75/hour. a. b. C. 2. In total, there are 2 supervisors each paid 63850 each and 2 repairman/maintenance each paid $40,000. Other factory overhead consists of the following: 1. Property taxes paid for the year - $35,000 2. Utilities paid for the year 160950 3. Six large machines. Each with a value of $100,000 depreciated over 10 years. Two machines are used in each department. Factory overhead is allocated using the ABC method and based on machine setups and machine hours WIP #3 Total units transferred 19,000 Total machine hours 21,000 Total machine setups 8594 Total Labor hours 6,840 WIP #1 56,000 53800 4,200 11,400 WIP #2 37,000 31,400 4612 4,560 Factory Overhead using machine hours = Fact. Dep. & Indirect materials total Factory overhead using machine set ups = Property taxes, utilities and indirect labor total Department #1 had 3,500 units in beginning WIP that were 50% complete as to conversion costs (totaling $12,000) and 100% complete for materials (totaling 42,000). 57250 units were started into production. Transferred out 56,000 units which included 37,000 basic to WIP #2 and 19,000 advanced to WIP #3. The remaining ending inventory was 100% complete for materials and 40% for conversion costs. Department #2 had 2,000 units in beginning WIP that were 50% complete as to conversion costs (totaling $3,000) and 100% complete for materials (totaling 10,000). 37,000 units were started into production. Transferred out 35,000 units. The remaining ending inventory was 100% complete for materials and 0.72for conversion costs. Department #3 had 1,000 units in beginning WIP that were 50% complete as to conversion costs (totaling $4,000) and 100% complete for materials (totaling 13,000). 19,000 units were started into production. Transferred out 19,200 units. The remaining ending inventory was 100% complete for materials and 70% for conversion costs. Basic and advanced will split the WIP #1 based on the number of units of each type. Thus if there were $100 in WIP #1 and 20 total units (14 basic and 6 advanced), Each unit would absorb $5. Therefore the basic would account for $70 of WIP #1 Beginning finished goods for basic vacuums totaled 6,500 units at a total cost of 148350 Beginning finished goods for advanced vacuums totaled 2,300 units at a total costs of 95950 Total sales for the basic vacuum were 39500 units @ $55 each Total sales for the advanced vacuum were 19,800 units @ 92each Instructions A. B. Prepare the following journal entries Raw material purchases 1. 2. 3. 4. 5. 6. 7. 8. 9. Distribution of raw materials to each WIP or Factory Overhead Accumulation of wages owed Distribution of wages to each WIP or Factory Overhead Accumulation of factory overhead Allocation of Factory overhead using ABC per WIP Transition of WIP 1 goods to either WIP 2 or 3 Transition of WIP 2 goods to Finished Goods Transition of WIP 3 goods to Finished Goods 10. Sale of Basic vacuums 11. Sale of Advanced vacuums What is the Gross Profit of each separately and combined? Jackson's Vacuum company makes two types of vacuums: Basic and Advanced. The factory is set up into 3 working departments. Both vacuums utilize process #1 to assemble the basic components. Those units destined as basic will transition to department #2 to be finalized. The advanced vacuums will skip department #2 and go directly to the advanced processing department #3. There are 4 types of raw material. #1-3 are all direct materials and # 4 is an indirect material #4 Beg. Raw Material Purchased on account End. Raw materials #1 13,000 193750 14150 #2 6,000 73865 10975 #3 45,000 382500 12550 7,000 53890 Requested materials - Dept. #1 Dept. #2 98600 in raw material #1 was requested, $40,000 for #2, $195,000 for #3 $20,000 in raw material #1 was requested, 15890 for #2, $46,000 for #3 $74,000 in raw material #1 was requested, $13,000 for #2, 173950 for #3 Indirect materials (#4) used this year amounted to 57650 Dept. #3 3240 1. There are 3 type of factory workers. Assembly line, area supervisor, and repairman/maintenance. Assembly line workers: 12 workers each work 1,900 hours per year. 6 workers work in process 1 and earn $12/hour. The other 6 workers work equally in departments 2&3 and make 14.75/hour. a. b. C. 2. In total, there are 2 supervisors each paid 63850 each and 2 repairman/maintenance each paid $40,000. Other factory overhead consists of the following: 1. Property taxes paid for the year - $35,000 2. Utilities paid for the year 160950 3. Six large machines. Each with a value of $100,000 depreciated over 10 years. Two machines are used in each department. Factory overhead is allocated using the ABC method and based on machine setups and machine hours WIP #3 Total units transferred 19,000 Total machine hours 21,000 Total machine setups 8594 Total Labor hours 6,840 WIP #1 56,000 53800 4,200 11,400 WIP #2 37,000 31,400 4612 4,560 Factory Overhead using machine hours = Fact. Dep. & Indirect materials total Factory overhead using machine set ups = Property taxes, utilities and indirect labor total Department #1 had 3,500 units in beginning WIP that were 50% complete as to conversion costs (totaling $12,000) and 100% complete for materials (totaling 42,000). 57250 units were started into production. Transferred out 56,000 units which included 37,000 basic to WIP #2 and 19,000 advanced to WIP #3. The remaining ending inventory was 100% complete for materials and 40% for conversion costs. Department #2 had 2,000 units in beginning WIP that were 50% complete as to conversion costs (totaling $3,000) and 100% complete for materials (totaling 10,000). 37,000 units were started into production. Transferred out 35,000 units. The remaining ending inventory was 100% complete for materials and 0.72for conversion costs. Department #3 had 1,000 units in beginning WIP that were 50% complete as to conversion costs (totaling $4,000) and 100% complete for materials (totaling 13,000). 19,000 units were started into production. Transferred out 19,200 units. The remaining ending inventory was 100% complete for materials and 70% for conversion costs. Basic and advanced will split the WIP #1 based on the number of units of each type. Thus if there were $100 in WIP #1 and 20 total units (14 basic and 6 advanced), Each unit would absorb $5. Therefore the basic would account for $70 of WIP #1 Beginning finished goods for basic vacuums totaled 6,500 units at a total cost of 148350 Beginning finished goods for advanced vacuums totaled 2,300 units at a total costs of 95950 Total sales for the basic vacuum were 39500 units @ $55 each Total sales for the advanced vacuum were 19,800 units @ 92each Instructions A. B. Prepare the following journal entries Raw material purchases 1. 2. 3. 4. 5. 6. 7. 8. 9. Distribution of raw materials to each WIP or Factory Overhead Accumulation of wages owed Distribution of wages to each WIP or Factory Overhead Accumulation of factory overhead Allocation of Factory overhead using ABC per WIP Transition of WIP 1 goods to either WIP 2 or 3 Transition of WIP 2 goods to Finished Goods Transition of WIP 3 goods to Finished Goods 10. Sale of Basic vacuums 11. Sale of Advanced vacuums What is the Gross Profit of each separately and combined? Jackson's Vacuum company makes two types of vacuums: Basic and Advanced. The factory is set up into 3 working departments. Both vacuums utilize process #1 to assemble the basic components. Those units destined as basic will transition to department #2 to be finalized. The advanced vacuums will skip department #2 and go directly to the advanced processing department #3. There are 4 types of raw material. #1-3 are all direct materials and # 4 is an indirect material #4 Beg. Raw Material Purchased on account End. Raw materials #1 13,000 193750 14150 #2 6,000 73865 10975 #3 45,000 382500 12550 7,000 53890 Requested materials - Dept. #1 Dept. #2 98600 in raw material #1 was requested, $40,000 for #2, $195,000 for #3 $20,000 in raw material #1 was requested, 15890 for #2, $46,000 for #3 $74,000 in raw material #1 was requested, $13,000 for #2, 173950 for #3 Indirect materials (#4) used this year amounted to 57650 Dept. #3 3240 1. There are 3 type of factory workers. Assembly line, area supervisor, and repairman/maintenance. Assembly line workers: 12 workers each work 1,900 hours per year. 6 workers work in process 1 and earn $12/hour. The other 6 workers work equally in departments 2&3 and make 14.75/hour. a. b. C. 2. In total, there are 2 supervisors each paid 63850 each and 2 repairman/maintenance each paid $40,000. Other factory overhead consists of the following: 1. Property taxes paid for the year - $35,000 2. Utilities paid for the year 160950 3. Six large machines. Each with a value of $100,000 depreciated over 10 years. Two machines are used in each department. Factory overhead is allocated using the ABC method and based on machine setups and machine hours WIP #3 Total units transferred 19,000 Total machine hours 21,000 Total machine setups 8594 Total Labor hours 6,840 WIP #1 56,000 53800 4,200 11,400 WIP #2 37,000 31,400 4612 4,560 Factory Overhead using machine hours = Fact. Dep. & Indirect materials total Factory overhead using machine set ups = Property taxes, utilities and indirect labor total Department #1 had 3,500 units in beginning WIP that were 50% complete as to conversion costs (totaling $12,000) and 100% complete for materials (totaling 42,000). 57250 units were started into production. Transferred out 56,000 units which included 37,000 basic to WIP #2 and 19,000 advanced to WIP #3. The remaining ending inventory was 100% complete for materials and 40% for conversion costs. Department #2 had 2,000 units in beginning WIP that were 50% complete as to conversion costs (totaling $3,000) and 100% complete for materials (totaling 10,000). 37,000 units were started into production. Transferred out 35,000 units. The remaining ending inventory was 100% complete for materials and 0.72for conversion costs. Department #3 had 1,000 units in beginning WIP that were 50% complete as to conversion costs (totaling $4,000) and 100% complete for materials (totaling 13,000). 19,000 units were started into production. Transferred out 19,200 units. The remaining ending inventory was 100% complete for materials and 70% for conversion costs. Basic and advanced will split the WIP #1 based on the number of units of each type. Thus if there were $100 in WIP #1 and 20 total units (14 basic and 6 advanced), Each unit would absorb $5. Therefore the basic would account for $70 of WIP #1 Beginning finished goods for basic vacuums totaled 6,500 units at a total cost of 148350 Beginning finished goods for advanced vacuums totaled 2,300 units at a total costs of 95950 Total sales for the basic vacuum were 39500 units @ $55 each Total sales for the advanced vacuum were 19,800 units @ 92each Instructions A. B. Prepare the following journal entries Raw material purchases 1. 2. 3. 4. 5. 6. 7. 8. 9. Distribution of raw materials to each WIP or Factory Overhead Accumulation of wages owed Distribution of wages to each WIP or Factory Overhead Accumulation of factory overhead Allocation of Factory overhead using ABC per WIP Transition of WIP 1 goods to either WIP 2 or 3 Transition of WIP 2 goods to Finished Goods Transition of WIP 3 goods to Finished Goods 10. Sale of Basic vacuums 11. Sale of Advanced vacuums What is the Gross Profit of each separately and combined? Jackson's Vacuum company makes two types of vacuums: Basic and Advanced. The factory is set up into 3 working departments. Both vacuums utilize process #1 to assemble the basic components. Those units destined as basic will transition to department #2 to be finalized. The advanced vacuums will skip department #2 and go directly to the advanced processing department #3. There are 4 types of raw material. #1-3 are all direct materials and # 4 is an indirect material #4 Beg. Raw Material Purchased on account End. Raw materials #1 13,000 193750 14150 #2 6,000 73865 10975 #3 45,000 382500 12550 7,000 53890 Requested materials - Dept. #1 Dept. #2 98600 in raw material #1 was requested, $40,000 for #2, $195,000 for #3 $20,000 in raw material #1 was requested, 15890 for #2, $46,000 for #3 $74,000 in raw material #1 was requested, $13,000 for #2, 173950 for #3 Indirect materials (#4) used this year amounted to 57650 Dept. #3 3240 1. There are 3 type of factory workers. Assembly line, area supervisor, and repairman/maintenance. Assembly line workers: 12 workers each work 1,900 hours per year. 6 workers work in process 1 and earn $12/hour. The other 6 workers work equally in departments 2&3 and make 14.75/hour. a. b. C. 2. In total, there are 2 supervisors each paid 63850 each and 2 repairman/maintenance each paid $40,000. Other factory overhead consists of the following: 1. Property taxes paid for the year - $35,000 2. Utilities paid for the year 160950 3. Six large machines. Each with a value of $100,000 depreciated over 10 years. Two machines are used in each department. Factory overhead is allocated using the ABC method and based on machine setups and machine hours WIP #3 Total units transferred 19,000 Total machine hours 21,000 Total machine setups 8594 Total Labor hours 6,840 WIP #1 56,000 53800 4,200 11,400 WIP #2 37,000 31,400 4612 4,560 Factory Overhead using machine hours = Fact. Dep. & Indirect materials total Factory overhead using machine set ups = Property taxes, utilities and indirect labor total Department #1 had 3,500 units in beginning WIP that were 50% complete as to conversion costs (totaling $12,000) and 100% complete for materials (totaling 42,000). 57250 units were started into production. Transferred out 56,000 units which included 37,000 basic to WIP #2 and 19,000 advanced to WIP #3. The remaining ending inventory was 100% complete for materials and 40% for conversion costs. Department #2 had 2,000 units in beginning WIP that were 50% complete as to conversion costs (totaling $3,000) and 100% complete for materials (totaling 10,000). 37,000 units were started into production. Transferred out 35,000 units. The remaining ending inventory was 100% complete for materials and 0.72for conversion costs. Department #3 had 1,000 units in beginning WIP that were 50% complete as to conversion costs (totaling $4,000) and 100% complete for materials (totaling 13,000). 19,000 units were started into production. Transferred out 19,200 units. The remaining ending inventory was 100% complete for materials and 70% for conversion costs. Basic and advanced will split the WIP #1 based on the number of units of each type. Thus if there were $100 in WIP #1 and 20 total units (14 basic and 6 advanced), Each unit would absorb $5. Therefore the basic would account for $70 of WIP #1 Beginning finished goods for basic vacuums totaled 6,500 units at a total cost of 148350 Beginning finished goods for advanced vacuums totaled 2,300 units at a total costs of 95950 Total sales for the basic vacuum were 39500 units @ $55 each Total sales for the advanced vacuum were 19,800 units @ 92each Instructions A. B. Prepare the following journal entries Raw material purchases 1. 2. 3. 4. 5. 6. 7. 8. 9. Distribution of raw materials to each WIP or Factory Overhead Accumulation of wages owed Distribution of wages to each WIP or Factory Overhead Accumulation of factory overhead Allocation of Factory overhead using ABC per WIP Transition of WIP 1 goods to either WIP 2 or 3 Transition of WIP 2 goods to Finished Goods Transition of WIP 3 goods to Finished Goods 10. Sale of Basic vacuums 11. Sale of Advanced vacuums What is the Gross Profit of each separately and combined? Jackson's Vacuum company makes two types of vacuums: Basic and Advanced. The factory is set up into 3 working departments. Both vacuums utilize process #1 to assemble the basic components. Those units destined as basic will transition to department #2 to be finalized. The advanced vacuums will skip department #2 and go directly to the advanced processing department #3. There are 4 types of raw material. #1-3 are all direct materials and # 4 is an indirect material #4 Beg. Raw Material Purchased on account End. Raw materials #1 13,000 193750 14150 #2 6,000 73865 10975 #3 45,000 382500 12550 7,000 53890 Requested materials - Dept. #1 Dept. #2 98600 in raw material #1 was requested, $40,000 for #2, $195,000 for #3 $20,000 in raw material #1 was requested, 15890 for #2, $46,000 for #3 $74,000 in raw material #1 was requested, $13,000 for #2, 173950 for #3 Indirect materials (#4) used this year amounted to 57650 Dept. #3 3240 1. There are 3 type of factory workers. Assembly line, area supervisor, and repairman/maintenance. Assembly line workers: 12 workers each work 1,900 hours per year. 6 workers work in process 1 and earn $12/hour. The other 6 workers work equally in departments 2&3 and make 14.75/hour. a. b. C. 2. In total, there are 2 supervisors each paid 63850 each and 2 repairman/maintenance each paid $40,000. Other factory overhead consists of the following: 1. Property taxes paid for the year - $35,000 2. Utilities paid for the year 160950 3. Six large machines. Each with a value of $100,000 depreciated over 10 years. Two machines are used in each department. Factory overhead is allocated using the ABC method and based on machine setups and machine hours WIP #3 Total units transferred 19,000 Total machine hours 21,000 Total machine setups 8594 Total Labor hours 6,840 WIP #1 56,000 53800 4,200 11,400 WIP #2 37,000 31,400 4612 4,560 Factory Overhead using machine hours = Fact. Dep. & Indirect materials total Factory overhead using machine set ups = Property taxes, utilities and indirect labor total Department #1 had 3,500 units in beginning WIP that were 50% complete as to conversion costs (totaling $12,000) and 100% complete for materials (totaling 42,000). 57250 units were started into production. Transferred out 56,000 units which included 37,000 basic to WIP #2 and 19,000 advanced to WIP #3. The remaining ending inventory was 100% complete for materials and 40% for conversion costs. Department #2 had 2,000 units in beginning WIP that were 50% complete as to conversion costs (totaling $3,000) and 100% complete for materials (totaling 10,000). 37,000 units were started into production. Transferred out 35,000 units. The remaining ending inventory was 100% complete for materials and 0.72for conversion costs. Department #3 had 1,000 units in beginning WIP that were 50% complete as to conversion costs (totaling $4,000) and 100% complete for materials (totaling 13,000). 19,000 units were started into production. Transferred out 19,200 units. The remaining ending inventory was 100% complete for materials and 70% for conversion costs. Basic and advanced will split the WIP #1 based on the number of units of each type. Thus if there were $100 in WIP #1 and 20 total units (14 basic and 6 advanced), Each unit would absorb $5. Therefore the basic would account for $70 of WIP #1 Beginning finished goods for basic vacuums totaled 6,500 units at a total cost of 148350 Beginning finished goods for advanced vacuums totaled 2,300 units at a total costs of 95950 Total sales for the basic vacuum were 39500 units @ $55 each Total sales for the advanced vacuum were 19,800 units @ 92each Instructions A. B. Prepare the following journal entries Raw material purchases 1. 2. 3. 4. 5. 6. 7. 8. 9. Distribution of raw materials to each WIP or Factory Overhead Accumulation of wages owed Distribution of wages to each WIP or Factory Overhead Accumulation of factory overhead Allocation of Factory overhead using ABC per WIP Transition of WIP 1 goods to either WIP 2 or 3 Transition of WIP 2 goods to Finished Goods Transition of WIP 3 goods to Finished Goods 10. Sale of Basic vacuums 11. Sale of Advanced vacuums What is the Gross Profit of each separately and combined? Jackson's Vacuum company makes two types of vacuums: Basic and Advanced. The factory is set up into 3 working departments. Both vacuums utilize process #1 to assemble the basic components. Those units destined as basic will transition to department #2 to be finalized. The advanced vacuums will skip department #2 and go directly to the advanced processing department #3. There are 4 types of raw material. #1-3 are all direct materials and # 4 is an indirect material #4 Beg. Raw Material Purchased on account End. Raw materials #1 13,000 193750 14150 #2 6,000 73865 10975 #3 45,000 382500 12550 7,000 53890 Requested materials - Dept. #1 Dept. #2 98600 in raw material #1 was requested, $40,000 for #2, $195,000 for #3 $20,000 in raw material #1 was requested, 15890 for #2, $46,000 for #3 $74,000 in raw material #1 was requested, $13,000 for #2, 173950 for #3 Indirect materials (#4) used this year amounted to 57650 Dept. #3 3240 1. There are 3 type of factory workers. Assembly line, area supervisor, and repairman/maintenance. Assembly line workers: 12 workers each work 1,900 hours per year. 6 workers work in process 1 and earn $12/hour. The other 6 workers work equally in departments 2&3 and make 14.75/hour. a. b. C. 2. In total, there are 2 supervisors each paid 63850 each and 2 repairman/maintenance each paid $40,000. Other factory overhead consists of the following: 1. Property taxes paid for the year - $35,000 2. Utilities paid for the year 160950 3. Six large machines. Each with a value of $100,000 depreciated over 10 years. Two machines are used in each department. Factory overhead is allocated using the ABC method and based on machine setups and machine hours WIP #3 Total units transferred 19,000 Total machine hours 21,000 Total machine setups 8594 Total Labor hours 6,840 WIP #1 56,000 53800 4,200 11,400 WIP #2 37,000 31,400 4612 4,560 Factory Overhead using machine hours = Fact. Dep. & Indirect materials total Factory overhead using machine set ups = Property taxes, utilities and indirect labor total Department #1 had 3,500 units in beginning WIP that were 50% complete as to conversion costs (totaling $12,000) and 100% complete for materials (totaling 42,000). 57250 units were started into production. Transferred out 56,000 units which included 37,000 basic to WIP #2 and 19,000 advanced to WIP #3. The remaining ending inventory was 100% complete for materials and 40% for conversion costs. Department #2 had 2,000 units in beginning WIP that were 50% complete as to conversion costs (totaling $3,000) and 100% complete for materials (totaling 10,000). 37,000 units were started into production. Transferred out 35,000 units. The remaining ending inventory was 100% complete for materials and 0.72for conversion costs. Department #3 had 1,000 units in beginning WIP that were 50% complete as to conversion costs (totaling $4,000) and 100% complete for materials (totaling 13,000). 19,000 units were started into production. Transferred out 19,200 units. The remaining ending inventory was 100% complete for materials and 70% for conversion costs. Basic and advanced will split the WIP #1 based on the number of units of each type. Thus if there were $100 in WIP #1 and 20 total units (14 basic and 6 advanced), Each unit would absorb $5. Therefore the basic would account for $70 of WIP #1 Beginning finished goods for basic vacuums totaled 6,500 units at a total cost of 148350 Beginning finished goods for advanced vacuums totaled 2,300 units at a total costs of 95950 Total sales for the basic vacuum were 39500 units @ $55 each Total sales for the advanced vacuum were 19,800 units @ 92each Instructions A. B. Prepare the following journal entries Raw material purchases 1. 2. 3. 4. 5. 6. 7. 8. 9. Distribution of raw materials to each WIP or Factory Overhead Accumulation of wages owed Distribution of wages to each WIP or Factory Overhead Accumulation of factory overhead Allocation of Factory overhead using ABC per WIP Transition of WIP 1 goods to either WIP 2 or 3 Transition of WIP 2 goods to Finished Goods Transition of WIP 3 goods to Finished Goods 10. Sale of Basic vacuums 11. Sale of Advanced vacuums What is the Gross Profit of each separately and combined?

Expert Answer:

Answer rating: 100% (QA)

Journal entries 1 For accumulation of overhead General Journal Debit Credit Factory overhead 521300 ... View the full answer

Related Book For

Horngrens Financial and Managerial Accounting

ISBN: 978-0133866292

5th edition

Authors: Tracie L. Nobles, Brenda L. Mattison, Ella Mae Matsumura

Posted Date:

Students also viewed these accounting questions

-

Work through the following guiding questions and attempt to develop how might we questions and what if questions for an issue of your choice. (You can use the discussion forum to work through your...

-

The following questions are adapted from a variety of sources including questions developed by the AICPA Board of Examiners and those used in the Kaplan CPA Review Course to study investments while...

-

Using the questions asked in evaluating any questionnaire design (see Exhibit 8.5) evaluate the Santa Fe Grill Restaurant questionnaire at the end of this chapter. Write a one page assessment report....

-

I am learning intermediate accounting and how to account for leases. I have a question about the calculation of present value for the right to use of the lease. my example specifically has a...

-

Based on panel a in figure, show that Angela would accept the BOGOF promotion or the half-price promotion. Show that she may choose to stay either three or four nights with the half-price promotion...

-

The angular velocity vector of a football which has just been kicked is horizontal, and its axis of symmetry OC is oriented as shown. Knowing that the magnitude of the angular velocity is 200 rpm and...

-

An often-ignored concept in breach of contract is the availability, if any, of the award of punitive damages. Often, cases incorporate both breach of contract and tort actions. The tort actions...

-

Wal-Mart Stores (Walmart) is the worlds largest retailer. It employs an everyday low price strategy and operates stores as three business segments: Wal-Mart Stores U.S., International, and Sams Club....

-

3. 1. Find the volume of the figures below. 2. Answer: Answer: 8.5 ft 4 ft. 2.5 ft. 7 cm. 14 cm. 6 cm. 4. 12 in 4 in. Answer: 9 in. Juice Answer: 6.5 in. 3 in. 2.5 in. 5 in.. 3 in.

-

Jones Company Edward Jones started the Jones Company Limited (JCL) as a sole proprietorship. It was later incor-- porated; ownership is now 50 percent controlled by Mr. Jones, who is 71 years old,...

-

Octavio Vazquez Corporation has two service departments, Power and Maintenance, and two production departments, Painting, and Polishing. The following data have been estimated for next years...

-

In a vacuum chamber you can throw a ball upwards from 1 . 5 0 m on earth before it reaches its highest point at 8 . 0 0 m and begins its descent, assume g = 9 . 8 0 m / s 2 . How much further could...

-

Set estion 1 of 2 < > 20/40 E Using the same case, calculate the independent effects of a 2 percent increase in Gross Margin, a 2 percent decrease in the Tax Rate, and a 5 percent decrease in Sales....

-

hello please can you help me with the following JAVA CODING Specifications You must define a class named MediaRentalManager (we did not provide it) that implements the MediaRentalManagerInt interface...

-

7. Based on the information in the table below, which displays the output from an estimation of the Fama French 3-factor model for Costco (COST), answer the following questions. Regression Statistics...

-

Organization A and Organization B are two contending organizations in a similar industry. Organization A has a higher overall revenue, however Organization B has a higher resource turnover...

-

Parkin Industries, a U.S. company, acquired a wholly-owned subsidiary, located in Italy, at the beginning of the current year, for 200,000. The subsidiary's functional currency is the euro. The...

-

Consider the data for Russell Department Stores presented in Problem P15-35B. Problem P15-35B Requirements 1. Prepare a common-size income statement and balance sheet for Russell. The first column of...

-

Summer Fun manufactures flotation vests in Tampa, Florida. Summer Funs contribution margin income statement for the month ended December 31, 2016, contains the following data: Suppose Over-town...

-

Princess has acquired several other companies. Assume that Princess purchased Kettle for $11,000,000 cash. The book value of Kettles assets is $12,000,000 (market value, $16,000,000), and it has...

-

Sumitomo Cable manufactures various types of aluminum and copper cables which it sells directly to retail outlets through its distribution channels. The manufacturing process for producing cables...

-

The Cooper Furniture Company of Potomac, Maryland, assembles two types of chairs (Recliners and Rockers). Separate assembly lines are used for each type of chair. Classify each cost item (AI) as...

-

The following data are for Marvin Department Store. The account balances (in thousands) are for 2017. 1. Compute (a) the cost of goods purchased and (b) the cost of goods sold. 2. Prepare the income...

Study smarter with the SolutionInn App