Question: Questions : Why did Palm computing's first product fail? Why should someone finance Palm Computing? Which financing option should Palm Computing choose? What is their

Questions :

Why did Palm computing's first product fail?

Why should someone finance Palm Computing?

Which financing option should Palm Computing choose? What is their cash requirement?

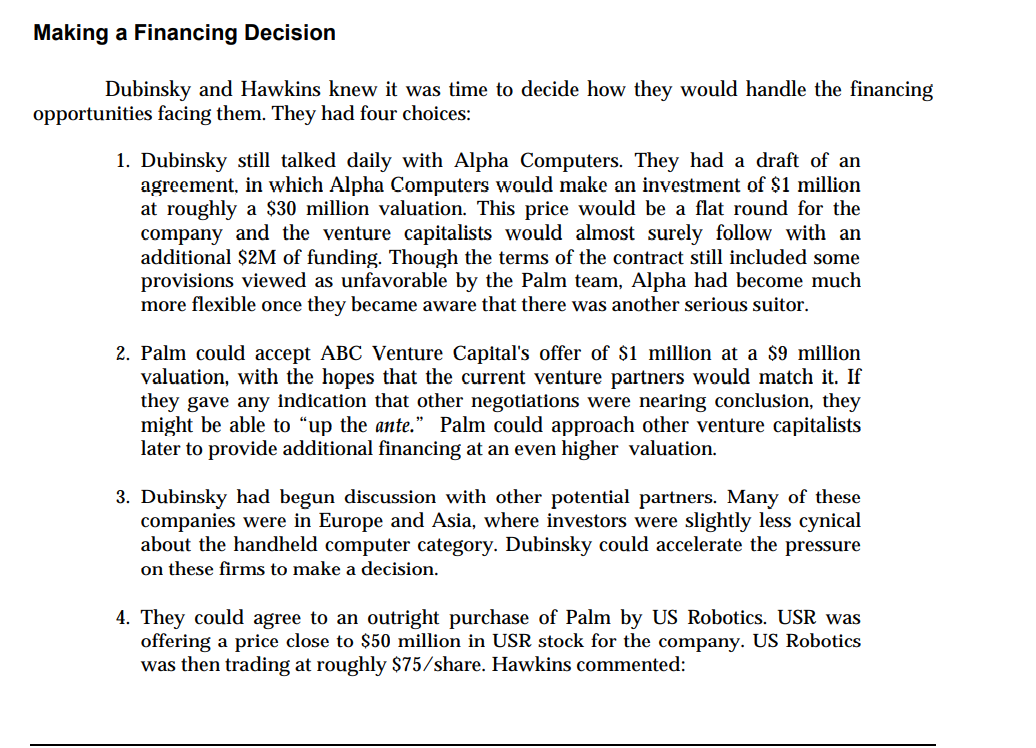

Palm Computing, Inc. 1995: Financing Challenges Donna Dubinsky paced the floor of her Los Altos, California office, talking quickly and pausing only when Jeff Hawkins interjected a comment. They were reviewing the top secret meeting they had held the day before with Jon Zakin of Chicago-based U.S. Robotics (USR). Dubinsky and Hawkins did not yet want anyone to know they were even considering a USR purchase of Palm, so the two of them, along with Ed Colligan, Palm's Vice President of Marketing, met Zakin near the airport and listened to what he had to say about USR. They were surprised by how quickly talks with USR had escalated from a simple equity investment to outright purchase. Only a week before, Dubinsky and Hawkins had met Zakin for dinner at the Fish Market and what began as a low key discussion about a possible USR investment in Palm led to his proposal that USR acquire Palm. Dubinsky wanted to get Hawkins' thoughts on Zakin's offer as soon as possible. Though she was the president and CEO of Palm Computing, any business decision of this magnitude would be made only after the two had fully discussed and agreed upon the final direction. Hawkins was, after all, the company's founder, chairman, chief technology officer, and major shareholder, as well as a trusted friend. USR's proposal was only one of several financing offers that they would be considering and each of the options came with its own unique risks and rewards. Dubinsky moved to the white board on the office wall and began marking off columns. Hawkins leaned back in his chair as she scrawled Objectives along the left hand side and began filling in brief notes, dates, and dollar amounts. Across the top, she added Venture Capital, Alpha Computers?, USR, and Other. In spite of the fact that the last 15 months of searching for capital had been exhausting, Dubinsky was exhilarated on that late August afternoon in 1995. She knew, without a doubt, that funding for the final stages of development and marketing of Palm Computing's organizer (code named Touchdown) would be available. Despite many roadblocks and some deadends in the process, she had persisted and had developed several financing alternatives. The idea of selling the company had not even been one of them when she started the capital search in mid-1994, but now that the USR offer was on the table, she decided it was worth evaluating along with Palm's other options. The Origins of Palm Computing Jeff Hawkins' technical background was strong - he earned his BSEE from Cornell University in 1979 and worked with Intel before joining GRID Systems as a software designer in 1982 but it was his insatiable curiosity about how the brain works that set him apart. Hawkins left GRID in 1986 to pursue a Ph.D. in biophysics at Berkeley. Though not everything about the program was satisfying, his studies in neurobiology at the university provided new insights about how the brain's pattern recognition might work. He developed and patented an algorithm that served as the basis for a unique handwriting recognition software he later developed. When Hawkins returned to GRID in 1988, he licensed his patented technology to the firm and began the work of creating commercial products based on it - primarily, handheld computing devices for store-door delivery systems and related applications. His pioneering work in pen-based computing in the late 1980's brought recognition to GRID and made Hawkins something of an industry star. Their initial success attracted the attention of much bigger players. NEC, NCR, Samsung, Sanyo, and IBM were among those who announced their intent to develop similar products. Hawkins believed that there was an even more attractive market for consumer products that could deliver the same functionality simply and cheaply. He realized, however, that GRiD was too focused on commercial markets to pursue that line of products. He decided to take his new business idea directly to GRID's new parent company, Tandy. Because Tandy's acquisition of GRID in 1989 was intended to give the national electronics retailer access to a steady stream of new consumer products, Hawkins felt confident that there would be interest in his proposal. He was right. Tandy's senior management liked the product idea and offered to set up a separate division for its development. Hawkins, however, came to the conclusion that a large organization was not the right place for the project. He turned the Tandy offer down and announced his decision to pursue the venture as an independent start-up. The Origins of Palm Computing Jeff Hawkins' technical background was strong - he earned his BSEE from Cornell University in 1979 and worked with Intel before joining GRID Systems as a software designer in 1982 but it was his insatiable curiosity about how the brain works that set him apart. Hawkins left GRID in 1986 to pursue a Ph.D. in biophysics at Berkeley. Though not everything about the program was satisfying, his studies in neurobiology at the university provided new insights about how the brain's pattern recognition might work. He developed and patented an algorithm that served as the basis for a unique handwriting recognition software he later developed. When Hawkins returned to GRID in 1988, he licensed his patented technology to the firm and began the work of creating commercial products based on it - primarily, handheld computing devices for store-door delivery systems and related applications. His pioneering work in pen-based computing in the late 1980's brought recognition to GRID and made Hawkins something of an industry star. Their initial success attracted the attention of much bigger players. NEC, NCR, Samsung, Sanyo, and IBM were among those who announced their intent to develop similar products. Hawkins believed that there was an even more attractive market for consumer products that could deliver the same functionality simply and cheaply. He realized, however, that GRiD was too focused on commercial markets to pursue that line of products. He decided to take his new business idea directly to GRID's new parent company, Tandy. Because Tandy's acquisition of GRID in 1989 was intended to give the national electronics retailer access to a steady stream of new consumer products, Hawkins felt confident that there would be interest in his proposal. He was right. Tandy's senior management liked the product idea and offered to set up a separate division for its development. Hawkins, however, came to the conclusion that a large organization was not the right place for the project. He turned the Tandy offer down and announced his decision to pursue the venture as an independent start-up. Building Palm's Resource Base Hawkins' recognition as a visionary in his field helped open venture capital doors for him. He had already begun discussions with one Silicon Valley venture firm when he got a call from Bruce Dunlevie, a VC at Merrill, Pickard, Anderson and Eyre. Dunlevie sat on the board of GeoWorks, an operating systems software company in Berkeley that Hawkins had contacted in his search for the right platform on which to build his software. When the president of that firm mentioned Hawkins' interest in partnering with GeoWorks to develop the operating system for his new handheld computing project, Dunlevie's ears perked up. He decided to follow up with a visit to Hawkins - both to get a potential customer's critique of GeoWorks products and to find out more about the new computing device. By the fall of 1991, Merrill Pickard and Sutter Hill Partners had committed $500,000 each to the new venture. Both firms were to be represented on the board and to share the lead investor role. Once Tandy acknowledged that Hawkins would not work within the organization, the CEO decided to invest $300,000 in the start-up. The investment not so much a financial move but rather was intended to provide access to the new products that might come out of the venture. Hawkins accepted the Tandy investment somewhat reluctantly. He was nervous about possible limits such a partnership might impose on Palm Computing in the future. He agreed to the investment as a condition of getting cross licensing agreements for the technology enhancements he had made at GRID, but he put a cap on Tandy's equity ownership (10%) and granted board observer rights only. Hawkins' strategic decision to concentrate all his efforts on software development meant that he needed to find partners to provide the operating software, to design and manufacture the hardware, and to market and distribute the bundled product. He would, in effect, have to build and manage a new value chain and he would, to some extent, have to entrust Palm's success to the best efforts of its partners. Howard Elias, special assistant to Tandy's CEO, helped Hawkins build working relationships with key partners. Though Hawkins located and engaged Geoworks (operating system software) on his own, Elias was the one who was able to bring Casio (hardware engineering and manufacturing), and Tandy (distribution) into the venture. Jeff Hawkins brought his vision, experience, and patent to the new venture. What he didn't bring was general management experience. Driven by his passion for the technology and anxious to devote all his energy to developing it, Hawkins was determined to find a president/CEO to run the business once he had closed the financing successfully and found the necessary development partners. He intended to remain as company chairman and to play a major role in decision making, so he was particularly concerned that the new company president be a good fit with his style and values. Building the Palm Computing Organization Donna Dubinsky graduated from Yale in 1977 with a degree in history. After two years working in commercial banking, she went on to earn her MBA at Harvard Business School. During her second year, she decided to explore opportunities in the then-emerging high technology industry. She was particularly interested in Apple Computer which had recently scored a hit with the introduction of its user-friendly PC's. When she approached the company, she was told that Apple was not interested in non-technical MBAs, but Dubinsky persisted, won an interview, and was hired as customer support liaison. The company grew rapidly, but Dubinsky's responsibilities expanded even more quickly. Named director of distribution and sales administration in 1984, she struggled to bring order to the inventory management and distribution processes and, in spite of initial resistance to systems building, achieved remarkable success. In 1987, Apple asked Dubinsky's boss, Bill Campbell, to head up a freestanding new venture, Claris Corporation, that was charged with developing software for the Macintosh computers. Campbell thought Dubinsky was exactly the kind of person he wanted to have on the senior management team of the new venture. He invited her to join the Claris team as Vice President of International. She jumped at the opportunity to take responsibility for sales, marketing, and distribution of the products outside the U.S. market and she grew her division's sales to 50% of total revenues in four years. When Apple re-purchased Claris's stock in 1989, Dubinsky's founder stock brought a substantial payoff and she decided to take a sabbatical year in Paris to study French and spend some time teaching in an MBA program there. She returned to California in the spring of 1992, refreshed and ready to step into the top spot in a yet-to be-identified high tech start-up. Her first call, after unpacking her bags, was to Bill Campbell. Since Dubinsky earned the bulk of her management experience under Campbell's tutelage, she knew that she would need his endorsement if she were to be hired as president of a fledgling high tech company. Campbell agreed to support her CEO search and he recommended she meet with Bruce Dunlevie, a venture capitalist he thought would be likely to know about many of the start-ups that would interest Dubinsky. The Hawkins-Dubinsky Team Coincidentally, Hawkins became interested in Dubinsky for the position of President/CEO of Palm when a candidate for another position brought up her name. Although Hawkins had already talked to 12 candidates for President/CEO of Palm and was very close to making a decision, he called Dubinsky. When Dubinsky and Hawkins met, they liked each other immediately and, after rigorous reference checking on both sides, agreed to partner in the venture. Dubinsky joined Palm in June, 1992. She recalled her decision: I started checking his references and when I called around I heard the kind of things I hoped people would say about me. Very genuine, down-to-earth, no bull, high integrity.' Exactly the things I value. It struck me we would be good partners. We share the same values and the same goals. That's what makes it work. Dunlevie noted that it was the intangibles rather than Dubinsky's rsum that won her the job: Every other candidate that we spent time with had (on paper) better qualifications for the job than she did. In that way, she was the least qualified, but she was also the best fit. She had the best chemistry with Jeff, best grasp of the market and she had something to prove. From the beginning the two formed a strong partnership. Organizing and Mobilizing Palm Second Round Financing Completed Dubinsky's first tasks were closely related. She was charged with developing a more formal business plan and raising an additional $3 million. In addition, she was expected to coordinate product specification and development with GeoWorks, Casio, and Tandy and to find appropriate staffing. Things moved along on schedule. With the finished plan in hand and partners on board, the second round financing was completed in September 1992. San Francisco-based Newtek Ventures provided $1.5 million and Sutter Hill and Merrill Pickard, participating pro rata, provided the rest. Working Partnerships Elias took the lead in structuring licensing agreements with Geoworks for the jointly-produced Zoomer software but Palm and Geoworks negotiated their own terms for other projects on a job-by-job basis. Palm set up a separate licensing agreement with Geoworks to develop the PalmConnect application software which would provide a data link between the handheld device and a desktop computer. The two firms worked together to develop and market new proposals to Sharp and other potential customers. Casio Japan joined the partnership at Tandy's request. The hardware manufacturer agreed to build the device and to pay royalties to Palm. Casio committed to manufacture 30,000 units during the last quarter of 1993, based on Tandy's order for 15,000 and its own estimate of sales through Casio distributors. Dubinsky coordinated Palm product development with Geoworks, Casio and Tandy throughout 1992 and into early 1993. Hardware design and operating software specifications had to be closely aligned with the new applications software that Palm was developing. Dubinsky remembers some of the challenges: There were six companies creating the Zoomer: Tandy, Casio, Geoworks, Intuit (which did a financial application), America Online and us--we had six companies sitting around the table negotiating every little detail. Though the parties disagreed on some details, the project was entirely cooperative in the early stages. The partners expected to collaborate on subsequent versions of the Zoomer, but the contract was open-ended as to the nature and timing of additional product introductions. Competitive Environment In early 1993, Apple Computer announced the Newton, the first of the palm size computers to be introduced. The Newton's shipment in August 1993 caught Palm off guard, not because Hawkins and Dubinsky were unaware of the Apple project, but because all intelligence reports indicated that the product was not yet ready for the market. Close on the heels of the Newton, the Zoomer had been announced in June 1993 but did not ship until October. The Newton generated tremendous interest, but its performance did not meet expectations. Likewise, although it received less attention, the Zoomer was viewed as slow, poorly positioned, and not well-connected to the PC. The press heaped criticism on Apple and the entire product category. Apple's premature launch slowed demand across the entire category. Dunlevie says: The Newton was introduced a month or two before the Zoomer and had been lampooned by everybody from Gary Trudeau to industry analysts for being fraudulent. By the time Palm's Zoomer was introduced, between negative feeling about the handheld computer category and the product's own deficiencies, it didn't have a fighting chance. The Zoomer reached the shelves for the Christmas 1993 season, but sales were disappointingly slow. Only 10,000 units were sold through early January...far below anticipated volume. Dubinsky remembers her frustration: After those dismal holiday sales, the category got very cold. It didn't matter that we were one of the cleverest companies in the category. We felt we had shipped an acceptable first generation product and we knew how to improve it, but the world felt we were in a dog category. These poorly received products were not the only failures in the handheld category. Taking into account some earlier failures, the Newton/Zoomer disaster, and other concurrent market efforts, Dubinsky estimated that approximately $1 billion were lost by industry participants in handheld product development. Moving On In spite of disappointing revenues, Palm started 1994 sufficient cash to meet the needs of the company for the next 6-9 months. The company was in good financial shape because Dubinsky had gone into the marketplace to secure a third round of funding before the Zoomer reached the retail shelves. She and Hawkins took a very conservative approach to cash, always raising money earlier rather than later. Second round investor Barry Weinman of Newtek had put her in touch with Credit Lyonnais in France which, with the original investors, committed third round funding of $3 million in late 1993 -- to close in January 1994. Palm's valuation for this round of financing was $30 million. As the closing date drew near, Credit Lyonnais began having second thoughts and talked about pulling out of the deal. The disappointing Zoomer sales numbers were beginning to come in just as Credit Lyonnais was trying to exit the venture capital business. Between signing the commitment letter and executing the final documents, Credit Lyonnais tried to renege on the deal, but Dubinsky was firm about holding them to the contract and, with some protestations, the deal went through as scheduled. The next question was, What should Palm do with the money?" There were still modest royalties coming in on the basic software ( $8 on the sale of each $600 unit) but the company had expected to generate most of its revenues and profits from follow-on products. The $129 PalmConnect which enabled Zoomer users to transfer information back and forth between their PCs and the Zoomer would yield more than a 50% gross margin, even after selling it through the distribution channel at 30% off suggested retail. Graffiti software which Palm began selling to other PDA (personal digital assistant) owners whose handwriting recognition was underperforming represented another product category. In spite of rave reviews in the press for these products, the limited sales in the PDA category meant that Graffiti sales were unlikely to be significant. The success of Palm's peripheral products depended on the development of an installed base of users. However excellent the gross margins might be, that meant little if the revenue line remained small. The Frustrations of Partnering When the Zoomer was being introduced in late 1993, Palm's VP of Marketing, Ed Colligan, pressed for aggressive marketing support, but he had to rely on Casio and Tandy to execute it. Neither partner put significant resources into the product launch, though Tandy developed some advertising promotions and took January markdowns. These, unfortunately, were a case of too little, too late." Dunlevie remarked: The Zoomer was certainly not a well-merchandised and marketed product and I think, in the final analysis, not a particularly well-conceived and implemented product...The product that came to market was only halfheartedly pushed by both Casio and Tandy. With approximately 20,000 units still in the distribution pipeline, Casio refused to commit to the second generation product, the Zoomer II, that the development team had planned to start on in early 1994. Palm had already moved ahead and was well into its new software development. Hawkins and Dubinsky pressed their partners to begin the work necessary to assure a new (and greatly improved) product would be available for sale by fall 1994. Hawkins and Dubinsky knew that, without Casio's cooperation, the plan would unravel. To overcome Casio's objections to obsoleting its current product, Palm proposed a plan to re-fit the existing hardware units with a new chip and Version 2 of the Palm software. Casio resisted any move that could involve a write-down and flatly refused to go forward until the original Zoomers cleared the pipeline. The Geoworks partnership was also frustrating. Dubinsky frequently clashed with Geoworks over priorities, pricing, joint selling and applications specifications. Even when collaborating on projects, the two firms sometimes competed for what Geoworks perceived as the limited software budget that hardware developers were willing to commit. Dubinsky and Geoworks executives disagreed about whether to sell their products bundled or unbundled and how to negotiate pricing for the two separate programs. Their differences came to a head in early 1994 when Dubinsky attended a meeting with Geoworks and Casio to try to convince Casio to move forward with Zoomer II. On the drive to the meeting, Dubinsky called the CEO of Geoworks to re-confirm that they were in lockstep. At the meeting, however, Geowork's head of sales pulled Dubinsky aside and told her they changed their mind and they were not going to support Zoomer II. Dubinsky was unable to sway Casio or Geoworks at this point. Dubinsky finally accepted the fact that Palm and Geoworks had different needs and priorities that made joint decision-making difficult. Both companies were aware that they could easily become competitors as Geoworks moved into the more lucrative applications software arena. By mid-1994, Palm began developing other platforms and turned its attention from Geoworks. With neither Casio nor Sharp willing to proceed on new hardware. Dubinsky and Hawkins were actively seeking new manufacturing partnerships. During this period Palm also published connectivity software for two Hewlett Packard handheld devices. The management team considered the idea of devoting itself to becoming a connectivity software player. Dubinsky started pitching this idea to other handheld partners and companies with existing devices. After exploring the market for connectivity software for handheld devices however, Dubinsky and Hawkins concluded that there were not enough handheld devices in use to matter. Even with a high "attach rate, the business opportunity was simply too small. A Retro-Perspective The Palm team was frustrated. They believed aggressiveness in getting to market with the next generation of Palm products was critical to its success, but all their partners had cold feet. After failing to get cooperation from Palm's original partners, Dubinsky talked to every major player in handheld computing, but to no avail. At a spring, 1994 meeting with investor Bruce Dunlevie, Dubinsky and Hawkins complained about the inability of their partners to execute. Dunlevie reminded them of the industry wisdom that made software companies so dependent on hardware companies and seemed to stand in the way of Palm independence: In a world of Microsoft, Intel, Compaq, IBM, Acer and Dell, the de facto wisdom of the day was that there were those who did semiconductors and those who did disk drives and those who did software and those who did boxes. PDA was a box. Trying to do all of those at the same time was ill-advised. Building hardware was expensive; it involved, at a minimum, one half million dollar investment in tooling, plus capital commitments for inventory, and subsequent infrastructure for repair and maintenance. This wisdom did not stop Dunlevie from challenging the pair to build the whole product, including hardware and software, themselves: I said to Jeff, You know how to do this and you are telling me the guys at Tandy certainly don't; the guys at Casio don't; the guys at Sharp don't. Why don't we go do it? You're the person who needs to design this product--whatever it is you think ought to get built. We should not leave our destiny in the hands of partners who don't share your vision. We better do it ourselves." Reflecting on why he took this perspective, Dunlevie said, We could hang out and bleed to death or we could bet the company on a riskier strategy. Looking for New Partners By August 1994, Hawkins completed the specifications for the new product's functionality and a mock-up. They code-named the product Touchdown and planned to ship it in January 1996. The Palm team was convinced that it could deliver all the components of the product as an integrated system, including the operating system, applications software, desktop software and hardware, by outsourcing some of the steps to partners. Hawkins was very clear on the product design goals: We set as our goal $299, shirt pocket size, focused on connectivity as the fundamental functionality. Every feature that did not meet these criteria did not go in. Colligan's marketing team categorized the product as a connected organizer, eschewing grander descriptions that might oversell the product Touchdown would be able to interface with the user's personal computer via a cradle connected to the serial port, which was also a departure from the conventional wisdom of the day. Conventional wisdom opined that any device that was handheld had to go over a wireless network to get e-mail or act as a phone. Hawkins' solution was simpler, lower cost and connected to the PC seamlessly. With the third round financing in the bank, the short-term cash position of the company was secure. Dubinsky had kept the burn rate of the company at $250,000 per month, about a quarter of what her competitors were struggling to manage. Because the team believed that cost of goods for the device itself would only be about $100 (unlike the $1000-$1500 cost of goods for a personal computer), inventory risk and working capital requirements would be relatively low. By Dubinsky's estimates, Palm would have the economic wherewithal to finish development of the new concept, but would not have sufficient cash to build inventory or market the product. Dubinsky knew she would need additional financial backing to launch Touchdown. One of Palm's investors felt strongly about having a corporate partner with a big name, believing that as long as a company with strong marketing and distribution capabilities had money at stake, it would work hard to make Palm succeed. With this in mind, Dubinsky set out to raise a total of $5 million. She believed if they could get $1-2 million from a corporate partner, venture capitalists would provide the rest. Dubinsky looked at several categories of potential partners, including communications equipment providers and personal computer manufacturers. She eliminated companies with which they had already partnered with poor results (Casio and Sharp). She also eliminated companies with competing products, such as Hewlett Packard. Telecommunications companies such as Erricson, Nokia, Motorola, and even companies like Tatung, Samsung, Glenayre, Qualcomm and US Robotics seemed to have the most obvious synergy. Because of their long-standing relationship, Dubinsky approached Radio Shack first. She wanted a commitment from them to distribute the new product through their 6000 outlets. Once she had that commitment in hand, she planned to find a manufacturing partner. However, because of their unsuccessful experience with the Zoomer, Radio Shack was not interested. Dubinsky would have to look elsewhere. Megacommunications International Dubinsky had begun pursuing other financing leads when Megacommunications International approached her in the Fall of 1994. Megacommunications' paging division was interested in developing a smart pager but it needed operating system software to do that. Palm's technology appeared to be just what they were looking for. The starting premise, from which the two parties assumed they could build an agreement, was that Palm would develop the operating system that would serve as Megacommunications' platform for its smart pager and Palm would create an organizer. Palm would develop organizer applications software and the organizer hardware, while Megacommunications would devote its efforts to the paging applications. Confident that a relationship between Megacommunications and Palm was probable, Dubinsky explored the possibility of working with other Megacommunications divisions as well. Hawkins had actually designed into the Touchdown hardware several components supplied by Megacommunications. Because of the customer-supplier relationship, Dubinsky thought it made sense for the component division to invest in Palm. She tried to division management to commit $1 million to Palm, but they declined. Dubinsky also worked with Megacommunications' central business development group. The head of the development group enthusiastically supported efforts to build a relationship between the two companies. With their help, Dubinsky talked to the cellular telephone manufacturing division about using Palm's operating system. Although she maintained discussions with several divisions, a relationship with the paging division seemed most likely. An agreement looked so promising that Dubinsky stopped pursuing other leads. But six months later, talks between Palm and Megacommunications began to founder. Palm had expected Megacommunications would make an equity investment in the company and, in return, Palm would license its operating system to Megacommunications' paging division. Megacommunications, on the other hand, wanted complete ownership and use of the intellectual property, including Palm's source code and hardware design though they were willing to license it back to Palm for the connected organizer. Megacommunications believed that in order to base their product on an operating system, they had to own that software. Palm was not willing to give up control over development of their operating system, which was Dubinsky and Hawkins saw as the heart of the company. Dubinsky realized it was time to end the negotiations and look elsewhere for financing There were many wonderful connections across the company. It was a no-brainer. Yet I couldn't get them to do a deal. At the end of the year, we realized we had to walk away. Dubinsky reflected on her single-minded pursuit of Megacommunications as a partner: We were approaching investor/partners serially, which was a big mistake. But you get so wrapped up in one, it's very hard, particularly with Megacommunications, International, where you're working with so many divisions at once. Alpha Computers In October 1994, an executive who had previous dealings with Hawkins called him from Alpha Computers, a large PC manufacturer. Alpha Computers wanted to sell a handheld product that would be more like a PC accessory than a stand-alone product. Unbeknownst to them, their concept was very close to what Palm had already developed. When they heard Hawkin's presentation on Touchdown, they loved it. By February 1995, a term sheet between the two companies was nearly complete. Dubinsky, who had, by this time, ended talks with Megacommunications, turned all her energy to completing the Alpha Computers deal. She had assurances from the head of the business unit at Alpha Computers that they were committed to doing the deal, but four months later, virtually no progress had been made in finalizing the contract. Palm and Alpha Computers disagreed on several important issues. For example, Alpha Computers planned to distribute product under its own label and Palm was free to distribute under its own brand name, but Alpha Computers insisted on a clause in the contract that insured the two partners would always launch joint products at the same time. Palm believed it could be stymied if Alpha Computers decided to delay a launch for any reason. There were also disagreements about channel differentiation and source code issues. Dubinsky began to see that the two companies had fundamentally different views of the deal. She believed that Palm was creating a product that would be supplied on an OEM basis (original equipment manufacturer, i.e. built by Palm but sold under the Alpha label) to Alpha Computers, but she came to realize that Alpha Computers had another vision. They saw Palm as a supplier that had come up with an idea that would soon be an Alpha Computers' product. Alpha Computers maintained that their endorsement and marketing clout were all that were needed to make the product a success. Dubinsky remembered: We went on and on and on. They put this finance guy in charge of the negotiations. His attitude was that Alpha Computers was clearly in the driver's seat. He kept adding protections and regulations and policies and the agreement started getting bigger and heavier and more complex...It seemed that the negotiation goal was one of protecting Alpha instead of maximizing the opportunity. Widening the Net While talks with Alpha Computers were under way, Hawkins and his developers had moved from writing software to making tooling decisions in preparation for building the devices. They were fast approaching the time when Palm would need to spend money on manufacturing, inventory, sales staff, and a marketing launch. In addition to negotiating with Alpha, Dubinsky was talking with other potential capital providers. She approached several venture capitalists, looking for a total of $2-3 million, but the VC community remained very lukewarm on the handheld computer category. One venture capital firm, ABC Venture Capital, did offer financing at a $9 million valuation (compared to Credit Lyonnais' $30 million valuation on the previous round). Dubinsky observed that this valuation was about equal to the liquidation value of the company, but she planned to approach her current investors to see if they would agree to raising a small amount at this valuation so that the product could be launched. Additional cash could be raised later at a higher valuation based on the results of Touchdown's early market performance. Another Opportunity Knocks with US Robotics Dubinsky had identified US Robotics as a partner candidate during the early stages of her search. Some synergy already existed between USR and Palm, since Palm intended to integrate a modem into the Touchdown eventually. Dubinsky had a friend who was an investment banker at Hambrecht and Quist, a leading technology investment bank. This friend had done a lot of work on USR's initial public offering and she agreed to provide Dubinsky with an introduction to USR. Though it took awhile to schedule a meeting with Jon Zakin, the Senior Vice President of Business Development at USR, Hawkins and Colligan finally met up with him in Salt Lake City. Zakin was actively searching for big, new investment opportunities. He loved the Touchdown product and decided, almost on the spot, that he wanted to work out some sort of deal with Palm. Palm originally proposed a $5 million investment by US Robotics. It was from this starting point that they all agreed to meet at the Fish Market for dinner two weeks later. This original proposal called for USR to make an investment in Palm. In the deal that Zakin originally envisioned, Palm's second generation product would provide a cavity into which the PCM/CIA modem division of USR, called Megahertz, would put modems. Soon after the dinner meeting, however, Zakin's enthusiasm for Palm's product and the company continued to grow. He called Dubinsky at home shortly after the Fish Market dinner broke up to propose an outright purchase of the whole company. Even though it was a weekend, Dubinsky immediately called Hawkins, and the two met at Dubinsky's community swimming pool the next day to discuss the proposal while their kids swam. Selling the company was not an option the Palm team had been seeking, but the substantial cash investment proposed by Zakin was appealing. After discussions with Hawkins and Colligan, Dubinsky began to talk seriously with Zakin about the terms of a purchase. She gave USR 30 days to commit, during which time she agreed not to talk to other potential investors. USR offered a purchase price of close to $50 million in USR stock for Palm. Zakin promised that Palm would operate as an independent division. Dubinsky would be on USR's executive staff and the new parent would put as much investment money into Palm as was needed. Zakin claimed that Palm would be a key part of USR's future. USR showed far more flexibility than Dubinsky had found in her negotiations with other partners. Issues seemed to be handled quickly and cordially. Whenever something came up that was difficult resolve in the tight timeframe in which they were rking, Zakin assured them, Don't worry. We'll do the right thing." Dubinsky remembered the lure of doing a deal with USR: We've been pitching this deal and selling the product for a year and a half against huge odds, against skeptical audiences, and here we have this guy Zakin who says, I believe, and I'll pay what it takes to get it, and I want to make this big.' This was attractive to us-- somebody who has faith, somebody who doesn't think we are nuts. Making a Financing Decision Dubinsky and Hawkins knew it was time to decide how they would handle the financing opportunities facing them. They had four choices: 1. Dubinsky still talked daily with Alpha Computers. They had a draft of an agreement, in which Alpha Computers would make an investment of $1 million at roughly a $30 million valuation. This price would be a flat round for the company and the venture capitalists would almost surely follow with an additional $2M of funding. Though the terms of the contract still included some provisions viewed as unfavorable by the Palm team, Alpha had become much more flexible once they became aware that there was another serious suitor. 2. Palm could accept ABC Venture Capital's offer of $1 million at a $9 million valuation, with the hopes that the current venture partners would match it. If they gave any indication that other negotiations were nearing conclusion, they might be able to "up the ante. Palm could approach other venture capitalists later to provide additional financing at an even higher valuation. 3. Dubinsky had begun discussion with other potential partners. Many of these companies were in Europe and Asia, where investors were slightly less cynical about the handheld computer category. Dubinsky could accelerate the pressure on these firms to make a decision. 4. They could agree to an outright purchase of Palm by US Robotics. USR was offering a price close to $50 million in USR stock for the company. US Robotics was then trading at roughly $75/share. Hawkins commentedStep by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock