Question: Read through the articles and data tables, then answer the three questions under required Part A, and the four questions under required Part B. CASE

Read through the articles and data tables, then answer the three questions under required Part A, and the four questions under required Part B.

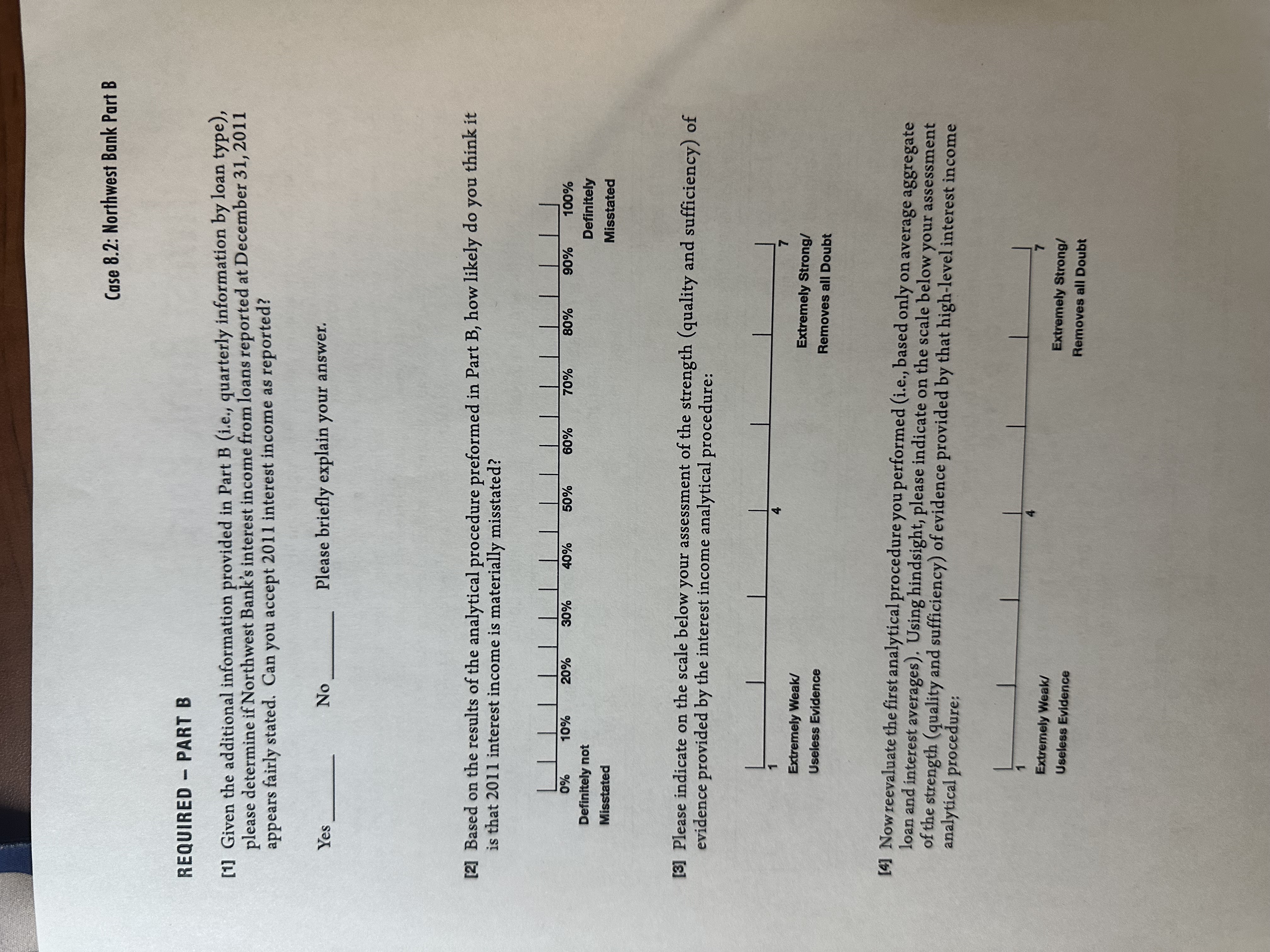

CASE 8.2 Northwest Bank Developing Expectations for Analytical Procedures MARK S. BEASLEY . FRANK A. BUCKLESS . STEVEN M. GLOVER . DOUGLAS F. PRAWITT LEARNING OBJECTIVES AwWhen emoonly After completing and discussing this case you should be able to Use analytical procedures as a reasonableness [3] Understand the relationship between the test of interest income precision of an expectation and the level of [2] Recognize factors that lead to the development assurance derived from an analytical procedure of more precise expectations [4] Understand the limitations of imprecise expectations BACKGROUND Northwest Bank (NWB) has banking operations in 35 communities in the states of Washington, Oregon, and Idaho. Headquarters for the bank are in Walla Walla, Washington. NWB's loan portfolio consists primarily of agricultural loans, commercial loans, real estate loans, and loans to individuals. Credit-granting authority is primarily centralized in Walla Walla; however, certain seasoned loan officers have decision authority for small loans in their local area. Loan portfolio performance, monitoring, and ongoing credit quality assessments are performed in Walla Walla for all loans. NWB has been an audit client for three years. Because of NWB's strong controls over bank loans, the audit team places high reliance on controls (i.e., control risk is assessed as low). The audit approach calls for the audit team to gain assurance on the fairness of loan interest income primarily through the performance of analytical procedures. Additional detailed testing will only be performed if analytical procedures suggest interest income is materially misstated. Total reported interest income for 2011 is $35,337,204, and reported net income for the bank is $12,484,000. A misstatement of $525,000 is considered material. In addition to comparing the 2010 interest income to 2009 interest income, last year's audit team also developed an expectation for loan interest income using the average loan volume multiplied by the weighted average interest rate. Last year's audit file indicates that the average loan volume agrees to numbers tested elsewhere in the audit file and that the interest rates used to compute the weighted average rate were comparable to rates published in a Washington State Banking Commission publication. The case was prepared by Mark S, Beasley, Ph.D. and Frank A, Buckless, Ph.D. of North Carolina State University and Steven M. Glover, Ph.D. and Douglas F. Prawitt, Ph.D. of Brigham Young University, as a basis for class discussion. It was adapted from an article authored by S. Glover, D. Prawitt, and J. Wilks appearing in the 25th Anniversary edition of Auditing: A Journal of Practice and Theory (2005). Northwest Bank is a fictitious company. All characters and names represented are fictitious; any similarity to existing companies or persons is purely coincidental. Copyright @ 2012 by Pearson Education, Inc., Upper Saddle River, NJ 07458 227Section 8: Analytical Procedures The following computation was performed last year. NWB's Loan Interest Analytical Procedure 2010 (in thousands) Average Loan Volume (or balance) 2010 $ 361,225 coloved Multiplied by Weighted Average Annual Interest Rate (2010) x 8.65% Computed 2010 Loan Interest Income per Audit $ 31,246 2010 Loan Interest Income per NWB $ 31,435 Difference (in thousands) $ 189 The following information was available for an analysis of the current audit year. NWB's Loan Interest Analytical Procedure Updated for 2011 (in thousands) Aggregate Loan Volume (or balance) as of Dec. 31, 2010 $ 388,110 Aggregate Loan Volume as of December 31, 2011 $ 383,860 OMOAT Average Loan Volume (or balance) for 2011 $ 385,985 Multiplied by Weighted Average Annual Interest Rate (2011) x 9.115% Computed 2011 Loan Interest Income $ 35,183 2011 Loan Interest Income per NWB $ 35,337 Difference (in thousands) $ 154 228Case 8.2: Northwest Bank REQUIRED - PART A [1] As part of the year-end audit and using the analytical-procedure approach similar to last year's audit (average loan volume multiplied by weighted-average interest rate), determine if Northwest Bank's interest income from loans reported at December 31, 2011 appears fairly stated. Do the results of the analytical procedure indicate that you accept 2011 interest income as reported? Yes No Please briefly explain your answer. [2] Based on the results of the analytical procedure, how likely is it that 2011 interest income is materially misstated? 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% Definitely not Definitely Misstated Misstated [3] Please indicate on the scale below your assessment of the strength (quality and sufficiency) of evidence provided by the interest income analytical procedure: Extremely Weak/ Extremely Strong/ Useless Evidence Removes all Doubt DO NOT CONTINUE ON TO PART B UNTIL INSTRUCTED TO DO SO STOP 229Section 8: Analytical Procedures Northwest Bank Part B Do NOT begin this part of the case until instructed to do so In an effort to develop a more precise (i.e., higher quality) expectation, you asked an associate to collect more detailed information, which is provided below. The quarterly rates are comparable to those reported in a Washington State Bank Commission publication. The quarterly loan volumes have been tied to audit work in other areas of the audit file. You decided not to have the associate track down detailed information for the "Individual and Other Loans" category because it is relatively small and is made up of heterogeneous loans. However, for the loans in the Individual and Other Loans category you do have the loan volume and weighted average interest rate as of December 31, 2010 and December 31, 2011. Recall that materiality for this area is $525,000. Commercial and Real Estate Individual and For the Year 2011 (balances in thousands) Agricultural Loans Loans Other Loans First Quarter Average Loan Volume (or Balance) $ 267,003 $ 99,998 See Info x Weighted Average Interest Rate (Qrtly) 2.15% 2.40% Below* Expected Interest Income, First Quarter 5,741 2,400 Second Quarter Average Loan Volume 263,868 101,200 See Info x Weighted Average Interest Rate (Qrtly) 2.08% 2.35% Below* Expected Interest Income, Second Quarter 2 5,488 2,378 Third Quarter Average Loan Volume 264,400 95,608 See Info x Weighted Average Interest Rate (Qrtly) 2.13% 2.35% Below Expected Interest income, Third Quarter 5,632 2,247 Fourth Quarter Average Loan Volume $ 266,510 $ 96,200 See Info x Weighted Average Interest Rate (Qrtly) 2.17% 2.43% Below* Expected Interest Income, Fourth Quarter 4 5,783 2,338 Annual Expected Interest Income by Loan Type based on Quarterly Data ( + 2 + 3+@ $ 22,644 $ 9,363 $ 2,515* Computed Total Interest Income per Audit $ 34,522 ($22,644 + $9,363 + $2,515, in thousands) 2011 Loan Interest Income per NWB $ 35,337 Difference (in thousands) $ 815 *Computation of Individual and Other Loans 12/31/2010 Average Annual Loan Volume 12/31/2011 Average $ 21,109 x Weighted Average Interest Rate $ 21, 152 $ 21,131 11.7% 12.1% 11.9% Annual Expected Interest, Individual and Other (in thousands) $ 2,515 230Case 8.2: Northwest Bank Part B REQUIRED - PART B [1] Given the additional information provided in Part B (i.e., quarterly information by loan type), please determine if Northwest Bank's interest income from loans reported at December 31, 2011 appears fairly stated. Can you accept 201 1 interest income as reported? Yes No Please briefly explain your answer. [2] Based on the results of the analytical procedure preformed in Part B, how likely do you think it is that 2011 interest income is materially misstated? 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% Definitely not Definitely Misstated Misstated [3] Please indicate on the scale below your assessment of the strength (quality and sufficiency) of evidence provided by the interest income analytical procedure: Extremely Weak/ Extremely Strong/ Useless Evidence Removes all Doubt [4] Now reevaluate the first analytical procedure you performed (i.e., based only on average aggregate loan and interest averages). Using hindsight, please indicate on the scale below your assessment of the strength (quality and sufficiency) of evidence provided by that high-level interest income analytical procedure: Extremely Weak/ Useless Evidence Extremely Strong/ Removes all Doubt

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Accounting Questions!