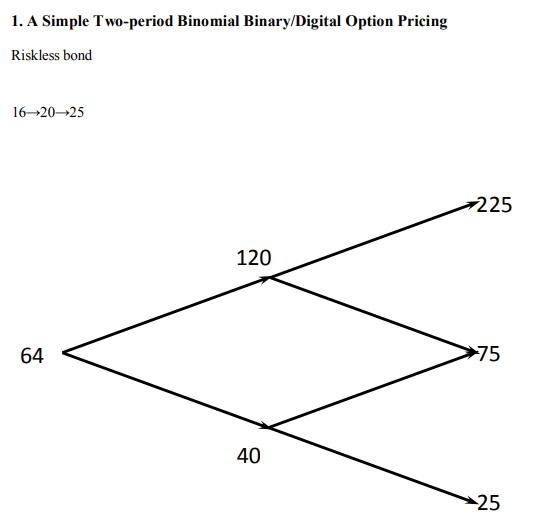

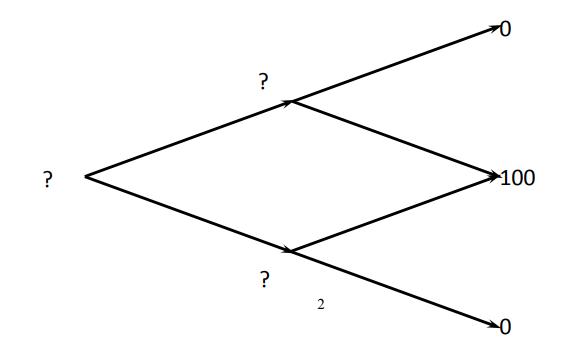

Derivative security (European binary/digital option paying 100 when the stock price is between 50 and 100 and

Fantastic news! We've Found the answer you've been seeking!

Question:

Derivative security (European binary/digital option paying 100 when the stock price is between 50 and 100 and paying zero otherwise). Each step is 12 months

The actual probabilities are 1/3 for up and 2/3 for down at each node.

a. (3 points) What are the risk-neutral probabilities of up and down?

b. (3 points) What is the value of the binary option at each node?

c. (3 points) In the portfolio strategy that replicates the binary option, what are the holdings in the stock and the bond at each node?

Expert Answer:

Related Book For

Physics

ISBN: 978-0077339685

2nd edition

Authors: Alan Giambattista, Betty Richardson, Robert Richardson

Posted Date: