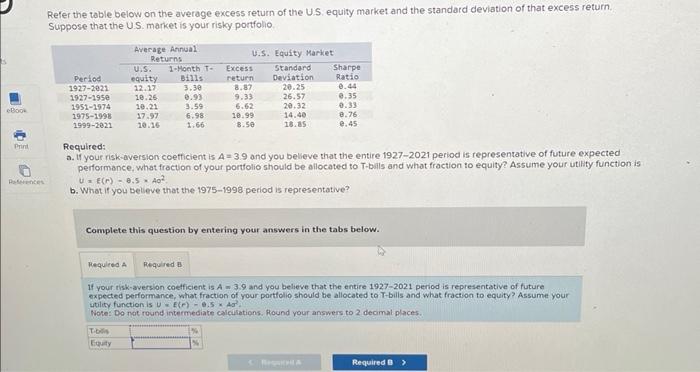

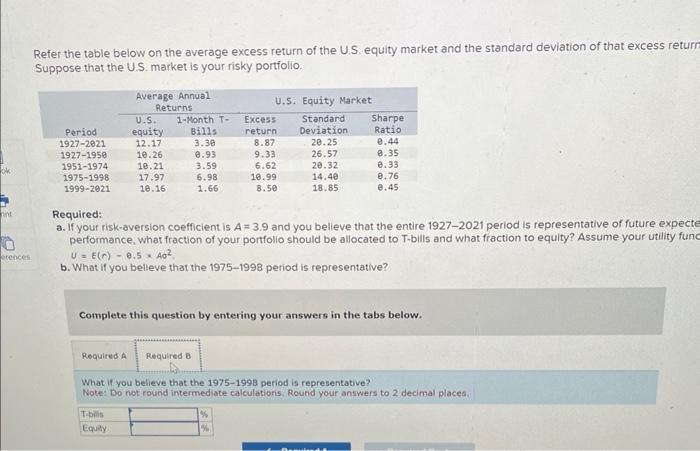

Question: Refer the table below on the average excess return of the US, equity market and the standard deviation of that excess return. Suppose that the

Refer the table below on the average excess return of the US, equity market and the standard deviation of that excess return. Suppose that the U.S. market is your risky portfolio. Required: a. If your risk-aversion coefficient is A=39 and you believe that the entire 19272021 period is representative of future expected performance, what frocton of your portfolio should be allocated to T-bals and what fraction to equity? Assume your utilify function is U=E(r)=8.5=AQ2 b. What if you believe that the 19751998 period is representative? Complete this question by entering your answers in the tabs below. If your risk-aversion coetficient is A =3.9 and you believe that the entire 19272021 period is representative of future expected performance, what fraction of your portfolio should be allocated to T-bilis and what fraction to equity? Assume your expected function is u=f(r)=e.5A2. Note: Do not round intermediate calculations. Round your answers to 2 decimal places. Refer the table below on the average excess return of the U.S. equity market and the standard deviation of that excess retur Suppose that the U.S. market is your risky portfolio. Required: a. If yout risk-aversion coefficient is A=3.9 and you believe that the entire 19272021 period is representative of future expect performance, what fraction of your portfolio should be allocated to T-bills and what fraction to equity? Assume your utility fun U=E(r)8.5A2 b. What if you belleve that the 1975-1998 period is representative? Complete this question by entering your answers in the tabs below. What if you believe that the 19751998 period is representative? Note: Do not round intermediate calculations, Round your answers to 2 decimal places. Refer the table below on the average excess return of the US, equity market and the standard deviation of that excess return. Suppose that the U.S. market is your risky portfolio. Required: a. If your risk-aversion coefficient is A=39 and you believe that the entire 19272021 period is representative of future expected performance, what frocton of your portfolio should be allocated to T-bals and what fraction to equity? Assume your utilify function is U=E(r)=8.5=AQ2 b. What if you believe that the 19751998 period is representative? Complete this question by entering your answers in the tabs below. If your risk-aversion coetficient is A =3.9 and you believe that the entire 19272021 period is representative of future expected performance, what fraction of your portfolio should be allocated to T-bilis and what fraction to equity? Assume your expected function is u=f(r)=e.5A2. Note: Do not round intermediate calculations. Round your answers to 2 decimal places. Refer the table below on the average excess return of the U.S. equity market and the standard deviation of that excess retur Suppose that the U.S. market is your risky portfolio. Required: a. If yout risk-aversion coefficient is A=3.9 and you believe that the entire 19272021 period is representative of future expect performance, what fraction of your portfolio should be allocated to T-bills and what fraction to equity? Assume your utility fun U=E(r)8.5A2 b. What if you belleve that the 1975-1998 period is representative? Complete this question by entering your answers in the tabs below. What if you believe that the 19751998 period is representative? Note: Do not round intermediate calculations, Round your answers to 2 decimal places

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts