Question: regarding the following case study answer the 4 question in the last pic banking institutions in the GCC reeson puts moen importance on the cability

![infrastructure projects effectively [19] Table 1. Financial Trintitution Asets in CCC and](https://s3.amazonaws.com/si.experts.images/answers/2024/07/66a5c4cdefc08_85366a5c4cd8180b.jpg)

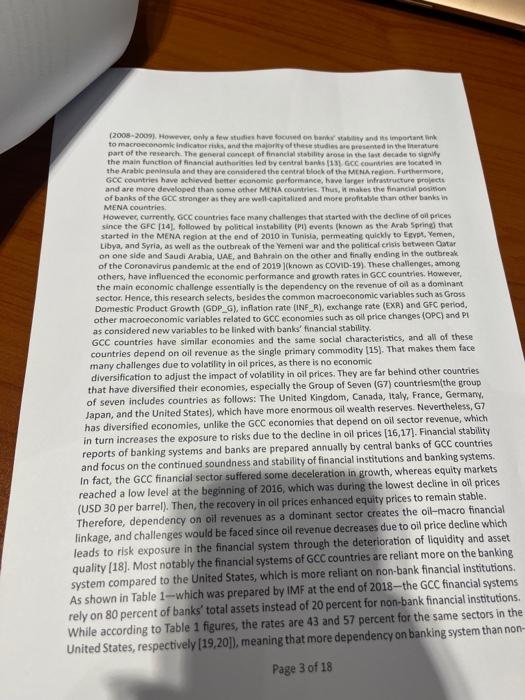

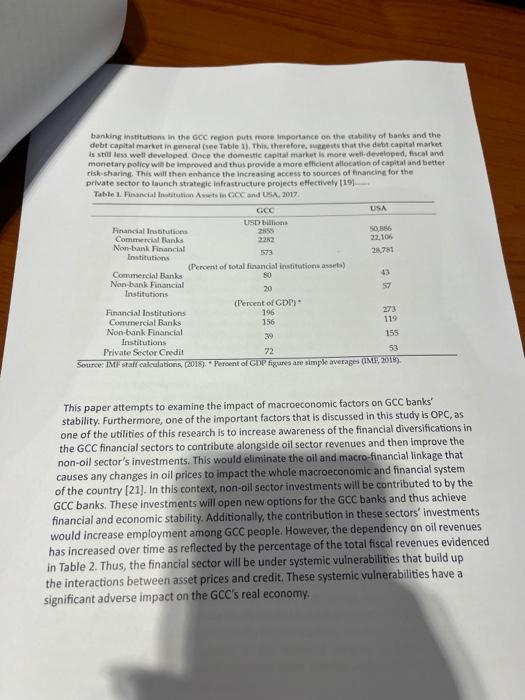

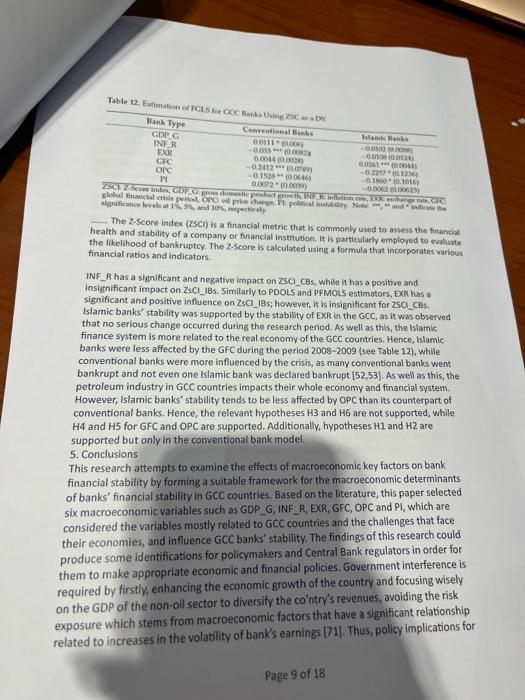

banking institutions in the GCC reeson puts moen importance on the cability of baeks and the debt capital market in eseneral (see Table i). Thic, therefore, incesits that the debt capital market is still less well developed. Once the domestic capital market is inore well-developed, flucal and. monetary policy wil be improved and thus provide a mote efficient allocation of capital and better risk-sharing. This will then eahance the increasing access to sources of financina for the private sector to launch strategic infrastructure projects effectively [19] Table 1. Financial Trintitution Asets in CCC and UsA, 2017. This paper attempts to examine the impact of macroeconomic factors on GCC banks' stability. Furthermore, one of the important factors that is discussed in this study is OPC, as one of the utilities of this research is to increase awareness of the financial diversifications in the GCC financial sectors to contribute alongside oil sector revenues and then improve the non-oil sector's investments. This would eliminate the oil and macro-financial linkage that causes any changes in oil prices to impact the whole macroeconomic and financial system of the country [21]. In this context, non-oll sector investments will be contributed to by the GCC banks. These investments will open new options for the GCC banks and thus achieve financial and economic stability, Additionally, the contribution in these sectors' investments would increase employment among GCC people. However, the dependency on oil revenues has increased over time as reflected by the percentage of the total fiscal revenues evidenced in Table 2. Thus, the financial sector will be under systemic vulnerabilities that build up the interactions between asset prices and credit. These systemic vulnerabilities have a significant adverse impact on the GCC's real economy. Table 12. Eatimation of rcts The 2-5core index (25CI) is a financial metric that is commonly used to assess the financial health and stability of a company or financial institution. It is particularly employed to evaluate the likelihood of bankruptcy. The Z-Score is calculated using a formula that incorporates various financial ratios and indicators. INF_ R has a significant and negative impact on ZSC_CBs, while it has a positive and insignificant impact on ZsCI.jBs. Similarly to PDOLS and PFMOLS estimators, EXR has a significant and positive influence on ZsCI_185; however, it is insignificant for 25ClCCBs. Islamic banks' stability was supported by the stability of EXR in the GCC, as it was observed that no serious change occurred during the research period. As well as this, the Islamic finance system is more related to the real economy of the GCC countries. Hence, Islamic banks were less affected by the GFC during the period 2008-2009 (see Table 12), while conventional banks were more influenced by the crisis, as many corventional banks went bankrupt and not even one Islamic bank was declared bankrupt [52,53]. As well as this, the petroleum industry in GCC countries impacts their whole economy and financial system. However, Islamic banks' stability tends to be less affected by OPC than its counterpart of conventional banks. Hence, the relevant hypotheses H3 and H6 are not supported, while H4 and H5 for GFC and OPC are supported. Additionally, hypotheses H1 and H2 are supported but only in the conventional bank model. 5. Conclusions This research attempts to examine the effects of macroeconomic key factors on bank financial stability by forming a suitable framework for the macroeconomic determinants of banks' financial stability in GCC countries. Based on the literature, this paper selected six macroeconomic variables such as GDP_G, INF_R, EXR, GFC, OPC and PI, which are considered the variables mostly related to GCC countries and the challenges that face their economies, and influence GCC banks' stablity. The findings of this research could oroduce some identifications for policymakers and Central Bank regulators in order for hem to make appropriate economic and financial policies. Government interference is equired by firstly, enhancing the economic growth of the country and focusing wisely n the GDP of the non-oil sector to diversify the co'ntry's revenues, avoiding the risk. kposure which stems from macroeconomic factors that have a significant relationship lated to increases in the volatility of bank's earnings [71]. Thus, policy implications for macroeconomic variables, as an externat influence, need government inferference in the GCC countries and need control of the banking sector, starting wht Centrat Banks and other financial authorities. The findings of this research provide some strategies that enable bank management to create good investment decislons. Hence, increasing awareness of the financial diversifications in the GCC financial sectors to contribute alongside oll sector revenues and then improving non-oil sector investments. This would eliminate the oil and macro-financial linkage, which causes am changes in oll prices to impact the whole macroeconomic and financial system of the country. In this context, non-oil sector imvestments will be contributed to by the GCC banks in order to withstand the adverse impacts of macroeconomic key. factors during the vulnerabilities of macroeconomic factors. Thus, increasing the financial stability of the GCC banks and ensuring that confidence in the whole GCC banking system will be enhanced. As well as this, this research provides the investment policymakers in GCC banks with an understanding to develop new financial strategic plans to enhance investment awareness, raising the level of financial and investment culture among various segments of society, which is consistent with the plans and programs in the GCC future visions such as the Saudi Arabia Vision 2030. Thus, this will contribute to strengthening the investment market in all GCC countries and also create new real jobs and investment opportunities for interested businessmen and businesswomen. As well as this, it wil increase the level of financial and investment culture among the gulf society, and open new opportunities for youth to join the labor market, including the oil and non-oll sectors. The limitations of this research can be summarized in two sentences. First, this paper ignored non-banking institutions, as it focused on banking institutions (conventional and Islamic banks), therefore the results of this research will not be applicable to non-banking institutions. Second, this paper excluded Sultanate Oman, a country member in the GCC region, because it started its Islamic banking industry in around 2012. The recommendation for future studies is to incorporate more macroeconomic variables relevant to GCC economies that influence banks' financial stability. Moreover, future research may take into consideration specific bank variables such as all financial risks; liquidity risk, credit risk, interest rate risk and CAR. There is also a need to differentiate between the GCC region and other regions such as southeast Asia in terms of banks' inancial stability. 2. Literature Review 2.1. Financlal Stability Definition There is no consensus in the literature about the definition of bank financial stability. Nevertheless, financial stability is related to financial problems that appear to be volatile in financlal institutions but not in non-financial institutions [23], Based on that, [24] defined financial stability as the ability of financial institutions to resist economic shocks, absorb the impacts of financial crises, and assess and manage risks. According to [13], the best method to define financial stability is to describe the characteristics of financial instablity. Therefore, banks' financial stability is defined as a period of the absence of instability of banks. Similarly, financial stability is the capability of the financial system-which is comprised of banks and other financial intermediaries, markets, and market infrastructure - to withstand shocks and financial crises [25]. 2.2. Macroeconomic Variables Both macroeconomic and financial imbalances are considered the main factors that play a role in triggering banking distress, which occurs due to an interaction between financial and macroeconomic factors, and also banks' structural weaknesses. Macroeconomic key factors affect banks through several adverse conditions, such as high rates of inflation and banking interest, and levels of negative growth and high level of unemployment [26]. Studies have indicated that some finance and banking variables are influenced by macroeconomicvariables. For example, bank profitability liquidity and Capital Adequacy Ratio credit risk [26,30]; bank efficiency and financial crises It is also recorded in the literature that macroeconomic factors affect the financial stability of banks differently [34-38]. This paper also selected important macroeconomic key factors such as; GDP_G, INF_R, EXR, GFC (2008/2009), and P to be regressed with the financial stability of individual banks. 2.2.1. GDP Growth Most financial stability studies have provided evidence that there is a significantly positive relationship between real GDP_G and bank financial stability Some studies have shown that GDP impact is positive but insignificantly related to bank stability or bank performance Other studies have found that GDP_G is negatively related to bank financial stability and also have found no clear linear dependence on bank stability On the contrary, found that the real GDP_G variable is significantly and negatively related to the financial stability of conventional banks, bu insignificantly and negatively related to 15 lamic bank stability. However, [92] and [36] found n impact of GDP_G on bank financial stablity. by the adverse effects of oll prices and negative changes had more effects on bank NPLs than positive changes in oll prices (102). The hypothesis of the OPC variable is stated as follows: Hypothesis 5 (HS). There is a sienificant and negative relationship between OPC and the financial stability of GCC banks. 2.2.6. Pollitical Instability The political stability variable is one of the important variables for a country's economic growth because there is a significant fole of political stability in economic growth, as a stable political environment indeed supports building and sustaining economic grown (8n). Political instability events adversely affected the financial and economic systems through heightened security concerns and increased geopolitical tension Ref., [103] suggested that political stability is a very important variable and is a significant predictor of domestic and foreign investments, as well as other key macroeconomic factors, such as GDP_G and INF_ R. If investor protection vla rules and regulations does not function well due to an unstable political environment, it will not be able to protect investors, institutions and properties. In addition, it was found that bank efficiency is affected positively by political stability as one of the categories of the world governance indices among the six indices presented by Kaufmann In this category, political stability is alongside other indicators, such as government effectiveness, regulatory quality, the rule of law, voice and accountability, and control of corruption As well as this, a significant and positive impact between political stability and banking stability in the MENA region was found In general, political events impact economic activities, which successively have effects on the banking system. Hence, PI is one of the macroeconomic factors that has an impact on bank performance Thus, the hypothesis of the PI variable is stated as follows: Hypothesis 6 (H6). There is a significant and negative relationship between PI and the financial stability of GCC banks. 4.5. Results of FGLS Estimator Such a result supports the study of [91]), which argued that higher GDP will lead to reduced risktaking by banks, and then increase banks' stability, as banks from faster-growing countries such as the GCC have a lower portion of impairment loans and are therefore less risky, which encourages banks to participate in financing investments and trusting investors. Similarly, PI has the same effects as the GDP_G impact on GCC banks. Hashed Mabkhot and Hamid Abdulkhaleg Masan AL-Whess. Article htpst//doliori/10.3390/su142315999 Academic Editari Nuno Crespo 1. Introduction Financial instifubins are considered the lifelalood of the econormy and the banking toctor is the most wital institution for growth and economic development. Banks called financiat intermediaries are the key sources of funding businesses, enhance economis growh, and contribute to faanclal stability apainst the shock of finarial crises as the main role of barks as instifutions of financial intermediation is to allocate deposits as a surplas fund from lenders as a surplus unit and to support the deficit in units, borrowers or investors effectiveliy afid efficientir [1]. In this regard, the banking system plays meaningful and useful functions that mostly deal with wealth and capital. These functions are especially related to monetary activities and include economic scarcity eradication, capital mobilization, and allocation of municipal funding, etc. 12 4]. Likewise, the banking systom also plays an essential role in connecting economic units and individuals through stocks and bonds in the financial markots, which are highly sensitwe to fluctuations, in interest rates. Besides the sfignificant role that banks play in friancial intermediation, banks also rum the wheels of overall economic relatons using the wealth that is crested through the process of financial intermediation [S]. Moreover, banks have a crucial role in ensuring financial stability and financing busfinesses in the real economy. Hence, a sound and productive banking sector contributes to growth, economic development and financial stablity. On the contrary, a decline in banking, stability or performance has an adverse impact on economic development and growth [1,6]. In this context, the strength of the banking system in a country is an essential condition to ensure continued economic growth and financial stability [7]. Thus, it could be sald that the profitability of banks enables coconomes to withstand the risks of external financial shocks [8]. The banking industry in the Gulf Cooperation Council (GCC) countries can be divided into two main banking systems: Islamic and conventional banking systems. Many countries, including the GCC, adopt a dual banking system where islamic banks operate alongside conventional banks [3,4]. In fact, this classification into Islamic and conventional banks is based on the operations of the main intermediation functions of the bank, that is collection of deposits and granting loans on the one hand, and on the other hand, paying (charging) of interest or returns [2,9], Islamic finance must fulfill Sharia (Islamic law) requirements by producing-Muamalat or products and services that comply with Sharia principles and implement the Prolit-Loss Sharing (PLS) modes, which essentially prohibit any financial transaction that gives or receives interest or riba [10], In addition, [11] argued that Islamic banks' modes of financing would increase the overal profitability and then increase the resillence capability of Islamic banks to protect the econom y absorbing losses during financial crises. Meanwhile, interest is the major driver of the financi termediation processes of conventional banking and is also considered the prime source come and cost of financing in conventional banks [12]. Bank Financial Stability in GCC Countri anking financial stability became a main concern during and after the global financial crisis (GF Page 2 of 18 banks and is nonsighificant when related to comensional hanks. Therelore, real CDOP C, en average, is expected to be positively related to the financial stabity of banks, anheues is that GDP_G very significantly and poshively affected insolivency fink (as measared by the Hypothesh 1 (H1). There is a significant and positive relationship between GPP_G and the financial stability of GCe banks. 2.2.2. Inflation fate 2.2.2. Inflation Rate Inflation is an important macroeconomic variable and is uned to provide information about banking system to be more vulnerable to risk [81], which is expected to have an impact on bank financial stability, as some studies believe, Most studies on financial stabuity have stated that INF_R is significantly and negatwely related to bank financial stability Although found that the impact of INF_R is different in Islamic and conventional banks, where is is negatively related to the stability of conventional banks but positively related to istamic banks' stability. As well as this; [94] found the same difference in impact between Islamic and conventional banks related to [94] found the same difference in impact between islamic and conwentional banks related to banks' stability. On the other hand, for Southeast Asian banks, it was found that the impact of INF_R is negative and significant on a large bank's stability. At the same time, it was positive and WF_R is negative and significant on a large banks stability. At the same time, it was positive and performance of comventional banks [95]. However, [36] and [92] found no impact of. INF 2R on performance of conventional banks [95]. However, [36] and [92) found no impact of. INF 2R on negatively correlated to all measures of bank profitablity [86]. As well as this, (96]) argued that in the Iong run, INF_R tends to have a positive and significant impact at the Non-Performing Loans (NPLS) ievel. Thus, increases in INF_, Rlead to increases in NPLs or credit riskicvels, which have an is stated as follows: Hypothesis 2(H2). There is a significant and negative relationship between INF_ R and the financial stability of GCC banks. 2.2.3. Exchange Rate Financial crises may be led by an exchange rate crisis, which results from local currency devaluation subsequently causing large losses in the international reserves of a country as banks may be impacted by this crisis and be prone to risk because of changes in foreign exchange rate [53]. Thus, it is expected that the stability of the exchange rate would be positively an significantly related to bank stability. it is supported by the literature on bank stability that th impact of movements in the exchange rate on bank financial stablity is significant and positi [36,89,90]. On the contrary, [38] and [95] found that the exchange rate has a significant a negative association with bank performance in Tanzania and the financial stability of large ba in Southeast Asian countries, respectively. However, it is insignificantly and negatively relate the financial stability of banks in MENA countries. The impact of changes in the exchange rate on the profit of banks has obviously been noted feterminant for bank profits via the common measures of bank profitability (return on ROA) and return on equity (ROE)]. [90] found that the official exchange rate affects profit Page 6 of 18 to macroeconomic indlcator rikik, and the majority of these studies are presented in the inerature the main function of financial autharities led by central banks [13] GCC coundries are iocated in the Arabic peoinsula and they ore conidered the cential blot k of the MCNak regen. Furthermore, GCC countries have achleved better ecanomic pesformarke, have larser infrastucture prolects of banks of the GCC stronger as ther are well capitalited and mere profitalie than other banks in MENA countries. Howevec currenth. GCC countries face mamy challenpes that started with the decline of oil prices since the GFC [14], Followed by political instability (P1) events (known as the Arab Spring) that started in the MENA region at the end of 2010 in Tunisia, permeating quickly to Egypt, Yemen, Libya, and Syria, as well as the outbreak of the Vemeni war and the political crisis betwens Catar on one side and Saudi Arabla, UAF, and Bahrain on the other and finally ending, in the outbreak. of the Coronavirus pandemic at the end of 2019 1(known as COND-19). These challenges, among others, have influenced the economic performance and growth rates in 6CC countries. However, the main economic challenge essentially is the dependency on the revenue of oll as a dominam sector. Hence, this research selects, besldes the common macroeconomic variables such as Gross Domestic Product Growth (GDP_G), inflation rate (INF_R), exchange rate (EXR) and GFC period, other macrooconomic variables related to GCC economies such as oll price changes (OPC) and Pl as considered new variables to be linked with banks' financial stability. GCC countries have similar economies and the same-soclal characteristics, and all of these countries dopend on oil revenue as the single primary commodity [15], That makes them face many challenges due to volatility in oil prices, as there is no economic diversification to adjust the impact of volatility in oil prices. They are far behind other countries that have diversified their economies, especially the Group of Seven (G7) countriesmlthe group of seven includes countries as follows; The United Kingdom, Canada, Italy, France, Germary, Japan, and the United States), which have more enormous oil wealth reserves. Nevertheless, G7 has diversified economies, unlike the GCC economies that depend on oil sector revenue, which in turn increases the exposure to risks due to the decline in oil prices [16, 17]. Financial stabitity reports of banking systems and banks are prepared annually by central banks of GCC countries and focus on the continued soundness and stabilty of financial institutions and banking systems. In fact, the GCC financial sector suffered some deceleration in growth, whereas equity markets reached a low level at the beginning of 2016 , which was during the lowest decline in oil prices (USD 30 per barrel). Then, the recovery in oll prices conhanced equity prices to remain stable. Therefore, dependency on oll revenues as a dominant sector creates the oil-macro financia linkage, and challenges would be faced since oll revenue decreases due to oil price decline whic leads to risk exposure in the financial system through the deterioration of liquidity and ass quality (18). Most notably the financial systems of GCC countries are reliant more on the banki system compared to the United States, which is more reliantion non-bank financial institutio As shown in Table 1 - which was prepared by IMF at the end of 2018 - the GCC financial syste ely on 80 percent of banks' total assets instead of 20 percent for non-bank financial instituti Vhile according to Table 1 figures, the rates are 43 and 57 percent for the same sectors in Inited States, respectively [19,20]), meaning that more dependency on banking system than Page 3 of 18 global financial syitems, (1 mark) 2. Summarize the key findings regarding the resilience of lisamie and conwentional bambi in GCC countries during the GFC. (1 Mark) 3. Apply the study's insights to propose potential strategies or policies for improvine the financial stability of banks in the GCC region. (2 Marki) 4. Analyze the role of specific macroeconomic variables dining finandial crises, such as: - GDP growth - Inflation - Exchange rate in influencing the stability of both Islamic and conventional banks in GCC countries. (2 Marks) very significantly and positively as meavured by hot, while thin impact he nesulive and very significant for profitablity measured by noA. Mt the same time, the inveabdity of the and wery rate increases risk in bank activity and losues may occur in transactions of the forelen exchange levels and such an indicator has an adverse influence on bask performance The thypothesh of the EXR variable is generally stated as follows: Hypothesis 3 ( H3 ). There is a significant and negative relationship between bxt and the finandal stability of GcC banks. 2.2.4. Global Financial Crisis The effects of the GFC were witnessed during 20072009 for conventional banks, while for istamie banks during 20082009, Generally, both types of banks faced many challenges during these periods, which had a severe impact on bank prolitabllity and performance, Net losses were reported due to the rising requirement for impairment and provisions [98]. Howtver, the impact of the crisis was different between islamic and conventional banks. A dummy variable was used by [15,99] ) to express the year(s) of a crisis as a dummy variable that takes onve for the year of the crisis (which was 2008/2009) and zero otherwise. It was found that islamic banks were more profitable than conventional banks during the GFC (2009-2009), while in the post-crisis period, they became less efficient and less profitabie and more prone to credit risk than conventional banks [80]. Ref. [56] suggested that tslamic banks were differently affected from conventional banks through two features related to Islamic banks. First, the PLS modes adopted by Islamic banks helped limit the adverse effects on profitability. Additionally, the PLS modes made islamic banks more resilient against the GFC [100] and second, the weakness of some Islamic banks inmimplementing risk management practices caused a decline in profitability compared to conventional banks. However, they found that the credit and asset growth of Islamic banks were better and contributed more to economic and financial stability than conventional banks during the crisis. Refs. [23,44] indicated that Islamic banks, during the period of GFC (2007-2009), were better capitalized and more cost-effective with higher asset quality ratios. As well as this, ref. [72] argued that Islamic banks are more resilient and stable during financial crises than their conventional counterparts. Nonetheless, an important variation was observed between large and small Islamic banks in terms of financial performance during the crisis [44]. Therefore, the hypothesis of the GFC variable is stated as follows: Hypothesis 4(H4). There is a significant and negative relationship between the GFC and the financial stability of GCC banks. 2.2.5. Oil Price Changes OPC have an effect on oil dependency economies, such as GCC economies. As observed, oil prices witnessed a substantial decline during the GFC of 2007/2009. Such a decline al impacted bank profitability in GCC countries In light of the impact of OPC on bank profitabili two ways that bank performance was affected in olf-exporting MENA countries are present direct impact through OPC and indirect impact through key macroeconomic factors [58]. Moreover, OPC negatively affected the majority of financial ubsectors, while non-financial subsectors were positively affected by OPC Furthermore, vas a significant and negative relationship between OPC and conventional anks' credit risk as proxied by NPLs. Moreover, large banks were more influenced Page 7 of 18

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts