Question: Requirement b. Would your answer to Part a change if Natasha's net income from consulting were only $4,200 for the year? (Natasha is electing to

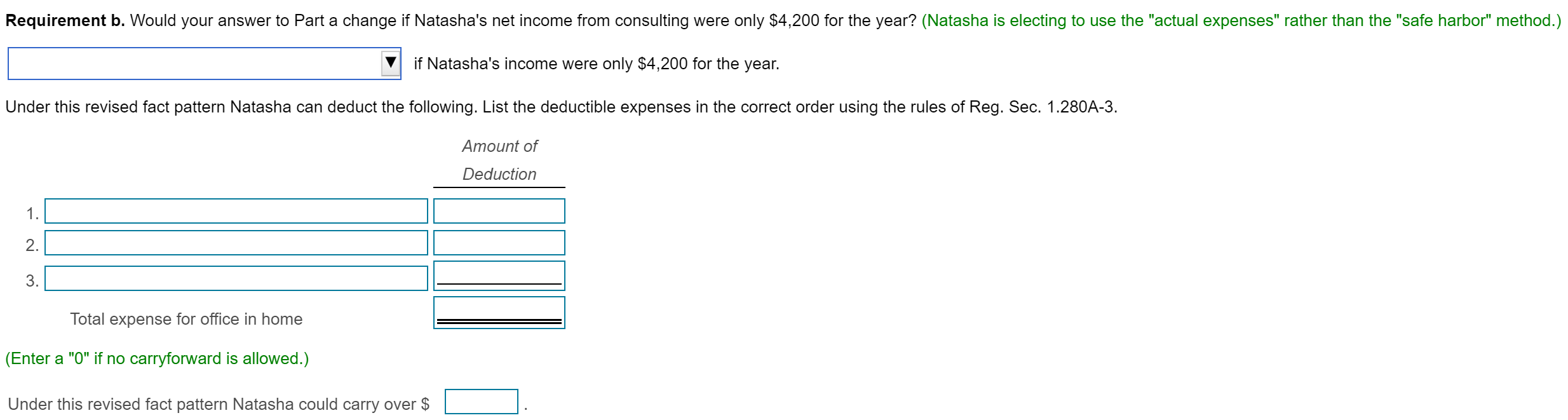

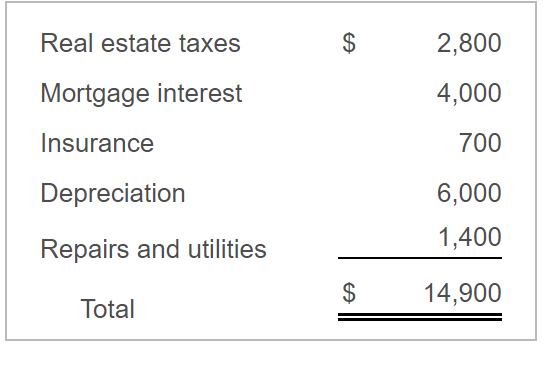

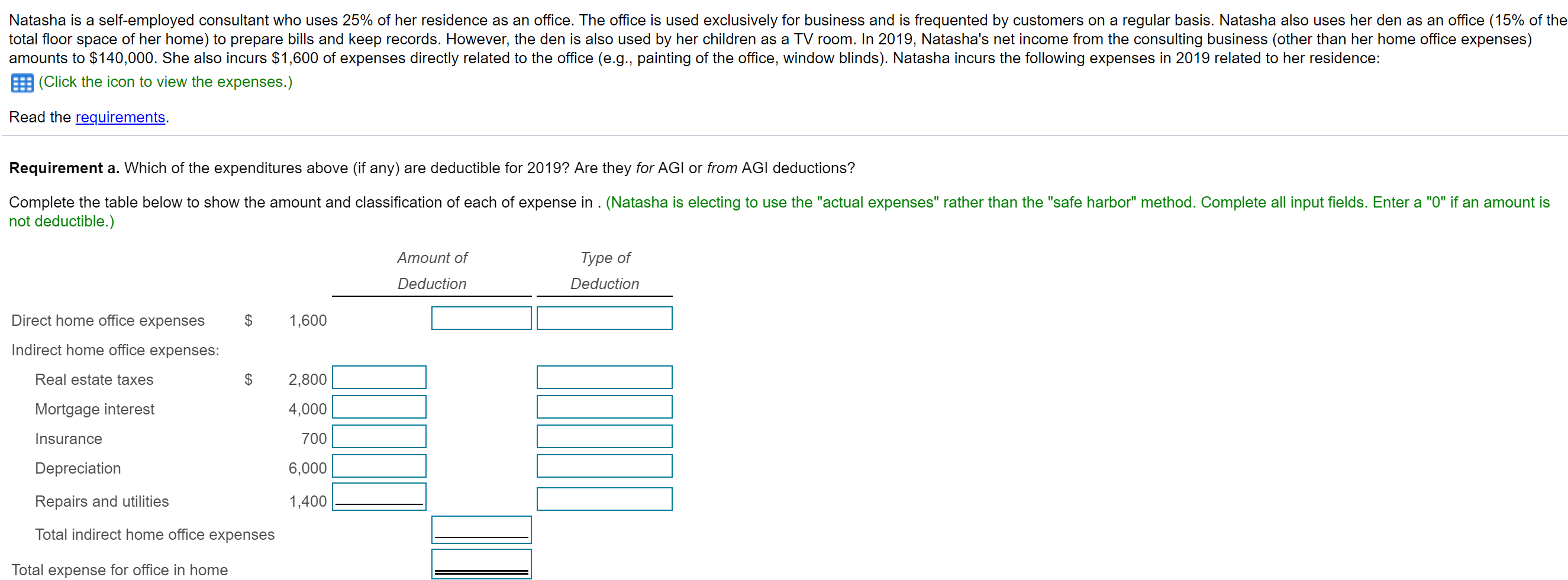

Requirement b. Would your answer to Part a change if Natasha's net income from consulting were only $4,200 for the year? (Natasha is electing to use the "actual expenses" rather than the "safe harbor" method.) if Natasha's income were only $4,200 for the year. Under this revised fact pattern Natasha can deduct the following. List the deductible expenses in the correct order using the rules of Reg. Sec. 1.280A-3. Amount of Deduction 1. 2. 3. Total expense for office in home (Enter a "0" if no carryforward is allowed.) Under this revised fact pattern Natasha could carry over $ Real estate taxes $ 2,800 Mortgage interest 4,000 Insurance 700 Depreciation 6,000 1,400 Repairs and utilities $ 14,900 Total Natasha is a self-employed consultant who uses 25% of her residence as an office. The office is used exclusively for business and is frequented by customers on a regular basis. Natasha also uses her den as an office (15% of the total floor space of her home) to prepare bills and keep records. However, the den is also used by her children as a TV room. In 2019, Natasha's net income from the consulting business (other than her home office expenses) amounts to $140,000. She also incurs $1,600 of expenses directly related to the office (e.g., painting of the office, window blinds). Natasha incurs the following expenses in 2019 related to her residence: (Click the icon to view the expenses.) Read the requirements. Requirement a. Which of the expenditures above (if any) are deductible for 2019? Are they for AGI or from AGI deductions? Complete the table below to show the amount and classification of each of expense in . (Natasha is electing to use the "actual expenses" rather than the "safe harbor" method. Complete all input fields. Enter a "0" if an amount is not deductible.) Amount of Type of Deduction Deduction Direct home office expenses $ 1,600 Indirect home office expenses: Real estate taxes $ 2,800 Mortgage interest 4,000 Insurance 700 Depreciation 6,000 Repairs and utilities 1,400 Total indirect home office expenses Total expense for office in home

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts