Requirements Assume you are one of the audit team members who will conduct the financial report audit

Question:

Requirements

Assume you are one of the audit team members who will conduct the financial report audit – year ending 30 June 2021 - for OneWorld. Using the company’s information given above, prepare a report dated June 12, 2021 for the audit manager outlining the audit plan. As it is the beginning of the audit do not prepare a final audit report/opinion. The report should cover the following areas under the suggested headings:

- Risk Assessment

From the background and financial information given above:

- identify and explain four (4) potential HIGH inherent risks and two (2) potential HIGH control risks. Please note, the risk given must be key and related to the client’s characteristics/situation.

- for each risk listed, identify the type of risk (inherent risk or control risk), and the associated financial accounts and key assertions that would be affected.

Please use the following table to present your answers:

Potential risk – type of risk, description | Accounts | Assertions |

|

|

|

|

|

|

- Planning Materiality

The audit firm dictates that one planning materiality amount (and percentage if necessary) is to be used for the financial statement as a whole. The planning materiality bases are as follows:

Base | Threshold (%) |

Profit before tax | 5-10 |

Turnover | 0.5-1 |

Gross profit | 2.0-5 |

Total assets | 0.5-1 |

Based on the information given and your risk assessment,

- select the base for planning materiality that you believe is most appropriate, and provide three reasons justifying the base you have chosen.

- calculate and suggest the planning materiality that you would use for the client.

(You can refer to GT program and textbook pages 106-107 and other resources for further understanding.)

- Analytical Procedures

As part of the risk assessment phase, you have to conduct analytical procedures:

- Based on the financial information given above, conduct analytical procedures using common-size analysis.

- Using the planning material set out above, discuss the results of the analytical procedures by outlining six (6) potential problem areas (that is, where possible material misstatements in the financial reports exist), and any other special concerns (for example, going concern). Specify the account balances and related assertions that would require attention in the audit. For each problem identified, you must use your quantitative analysis (with detailed calculations) to support your argument.

- Conclusion

Based on the risk assessment processes and analytical procedures undertaken in the previous sections, conclude the overall level of risk, materiality of the firm and recommend the areas of audit focus.

APPENDIX D – INCOME STATEMENT (PART B)

All figures in Australian Dollar | JUN '21 | JUN '20 | JUN '19 | JUN '18 |

Estimated | Actual | Actual | Actual | |

Revenue | 16,256,779 | 3,002,339 | 2,626,009 | 6,236,046 |

Share of profits of associates accounted for using the equity method | 53,400 | |||

Other income | 1,369 | 12,733 | ||

Interest revenue | 4,970 | 8,338 | 42,376 | |

Gain from deemed disposal of associate shareholding | 145,968 | |||

Expenses | ||||

Cost of sales | -5,705,534 | -1,380,724 | -1,775,523 | -3,537,527 |

Marketing | -1,089,951 | -91,685 | -50,599 | -71,451 |

Occupancy (Leasing) | -266,382 | 0 | -11,926 | -55,764 |

Administration | -7,453,540 | -1,560,008 | -2,385,159 | -2,199,018 |

Impairment of goodwill | -16,016,577 | |||

Acquisition costs | -180,417 | |||

Other expenses | -718,638 | -1,085,902 | -1,226,499 | -1,376,068 |

Finance costs | -48,785 | -24,450 | -51,769 | -106,050 |

Profit/Loss before income tax (expense)/benefit | 999,239 | -1,132,092 | -18,849,667 | -1,097,099 |

Income tax benefit | 1,626,926 | 0 | -418,942 | 59,922 |

Profit after income tax (expense)/benefit for the year attributable to the owners | 2,626,165 | -1,132,092 | -19,268,609 | -1,037,177 |

Other comprehensive income for the year, net of tax | ||||

Total comprehensive income for the year attributable to the owners | 2,626,165 | -1,132,092 | -19,268,609 | -1,037,177 |

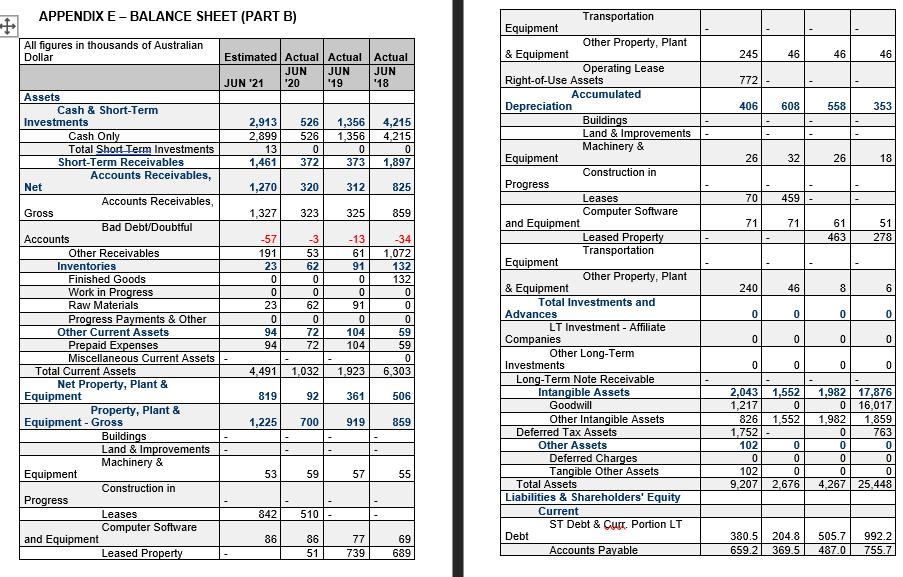

APPENDIX E – BALANCE SHEET (PART B) pages 1 - 2

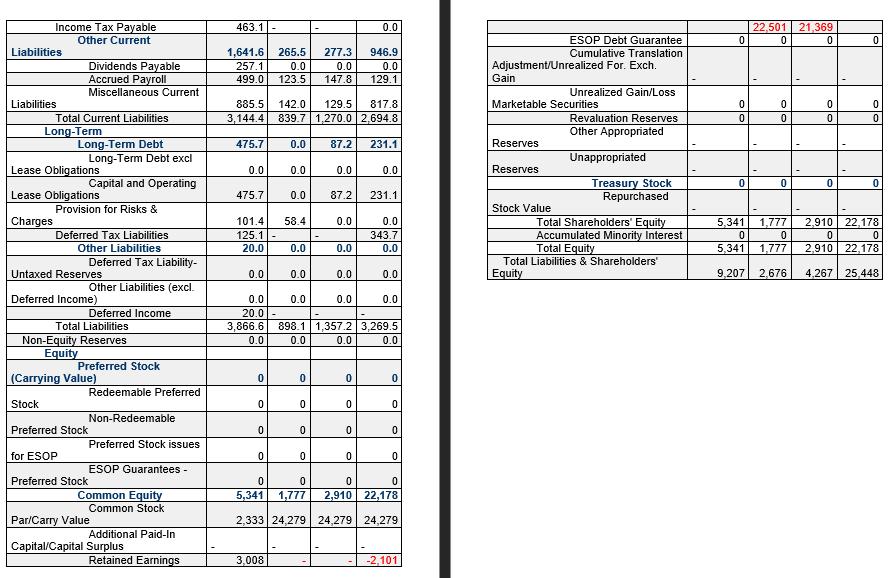

APPENDIX E continued – BALANCE SHEET (PART B) pages 3 - 4

Expert Answer:

Question Risk assessment is a term used to describe the overall process or method where you 1 Identify hazards and risk factors that have the potential to cause harm hazard identification 2 Analyze an... View the full answer