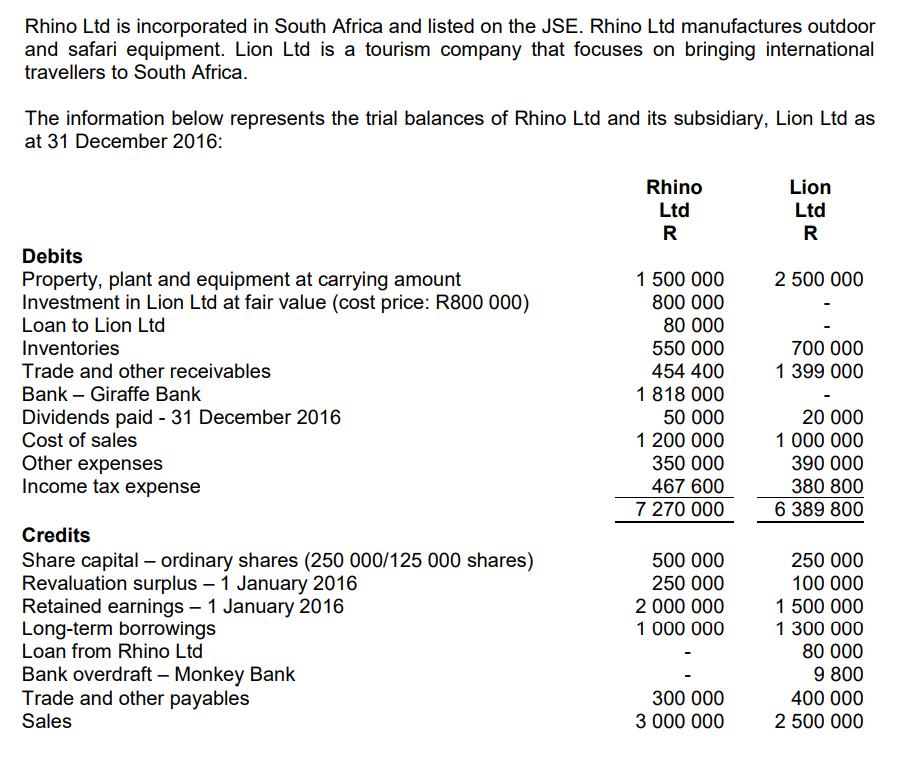

Rhino Ltd is incorporated in South Africa and listed on the JSE. Rhino Ltd manufactures outdoor...

Fantastic news! We've Found the answer you've been seeking!

Question:

![FAC2602/101 Marks 22 [22] ASSIGNMENT 02 (First semester) (continue) Part B Prepare only the following columns of the consolid](https://dsd5zvtm8ll6.cloudfront.net/si.experts.images/questions/2022/05/628b5f0c24824_1653301004275.jpg)

Transcribed Image Text:

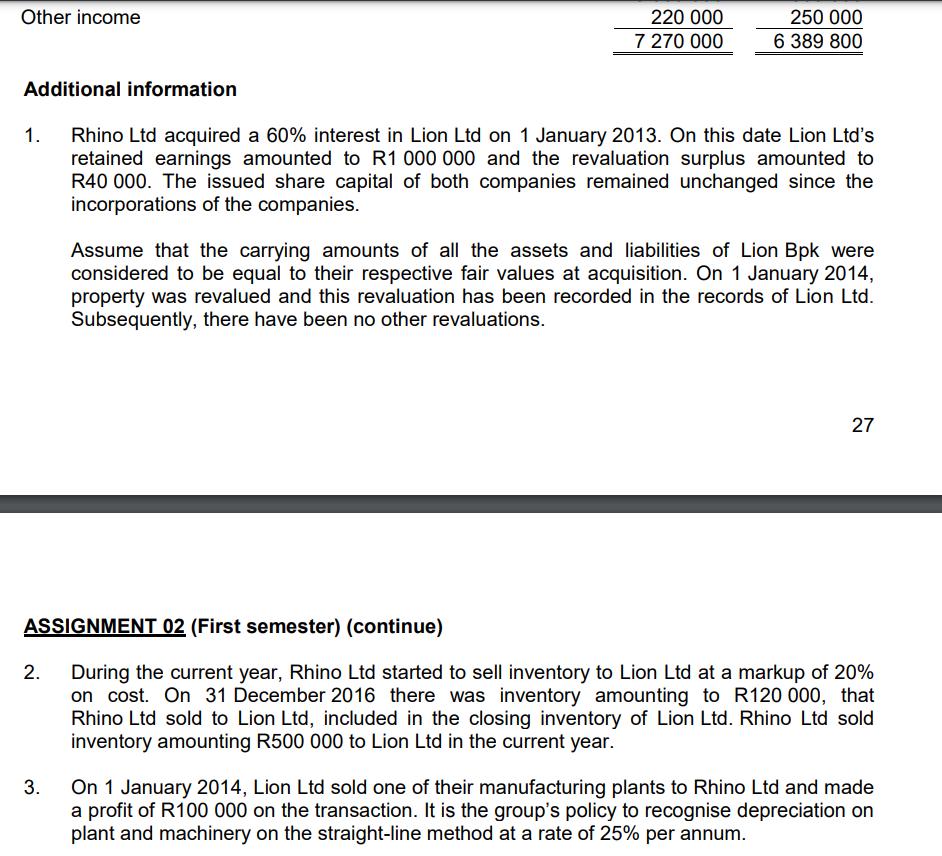

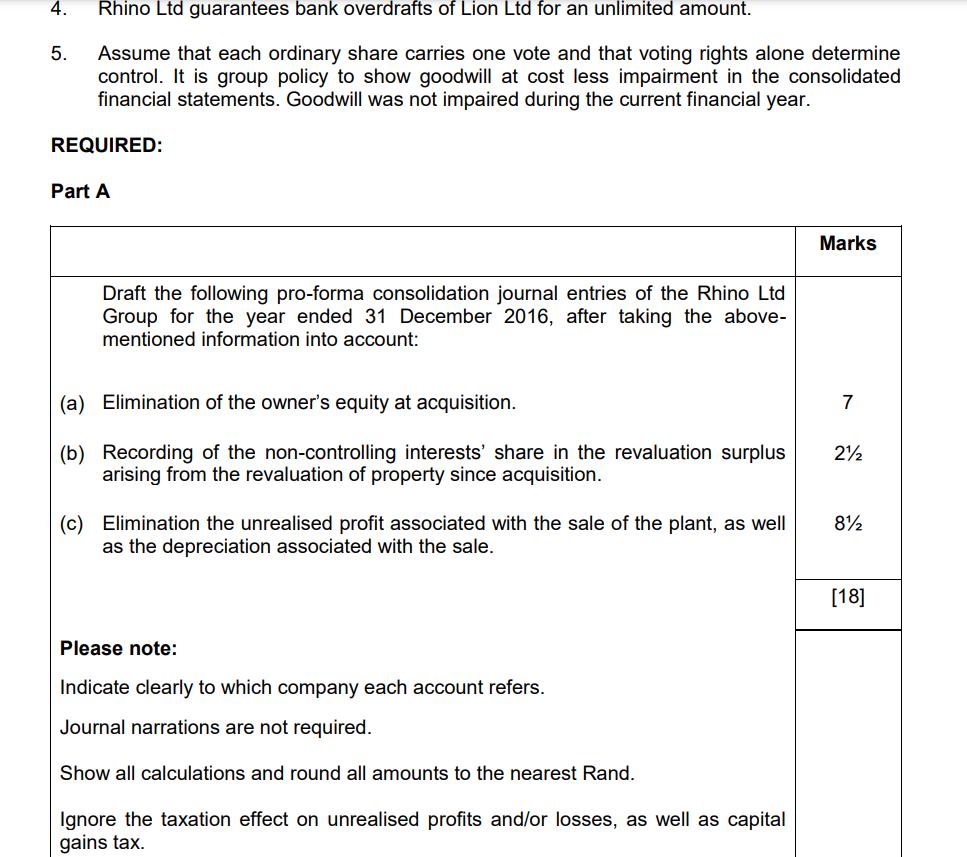

Rhino Ltd is incorporated in South Africa and listed on the JSE. Rhino Ltd manufactures outdoor and safari equipment. Lion Ltd is a tourism company that focuses on bringing international travellers to South Africa. The information below represents the trial balances of Rhino Ltd and its subsidiary, Lion Ltd as at 31 December 2016: Debits Property, plant and equipment at carrying amount Investment in Lion Ltd at fair value (cost price: R800 000) Loan to Lion Ltd Inventories Trade and other receivables Bank - Giraffe Bank Dividends paid - 31 December 2016 Cost of sales Other expenses Income tax expense Credits Share capital - ordinary shares (250 000/125 000 shares) Revaluation surplus - 1 January 2016 Retained earnings - 1 January 2016 Long-term borrowings Loan from Rhino Ltd Bank overdraft - Monkey Bank Trade and other payables Sales Rhino Ltd R 1 500 000 800 000 80 000 550 000 454 400 1 818 000 50 000 1 200 000 350 000 467 600 7 270 000 500 000 250 000 2 000 000 1 000 000 300 000 3 000 000 Lion Ltd R 2 500 000 700 000 1 399 000 20 000 1 000 000 390 000 380 800 6 389 800 250 000 100 000 1 500 000 1 300 000 80 000 9 800 400 000 2 500 000 Other income Additional information 220 000 7 270 000 1. Rhino Ltd acquired a 60% interest in Lion Ltd on 1 January 2013. On this date Lion Ltd's retained earnings amounted to R1 000 000 and the revaluation surplus amounted to R40 000. The issued share capital of both companies remained unchanged since the incorporations of the companies. 2. 250 000 6 389 800 3. Assume that the carrying amounts of all the assets and liabilities of Lion Bpk were considered to be equal to their respective fair values at acquisition. On 1 January 2014, property was revalued and this revaluation has been recorded in the records of Lion Ltd. Subsequently, there have been no other revaluations. ASSIGNMENT 02 (First semester) (continue) During the current year, Rhino Ltd started to sell inventory to Lion Ltd at a markup of 20% on cost. On 31 December 2016 there was inventory amounting to R120 000, that Rhino Ltd sold to Lion Ltd, included in the closing inventory of Lion Ltd. Rhino Ltd sold inventory amounting R500 000 to Lion Ltd in the current year. 27 On 1 January 2014, Lion Ltd sold one of their manufacturing plants to Rhino Ltd and made a profit of R100 000 on the transaction. It is the group's policy to recognise depreciation on plant and machinery on the straight-line method at a rate of 25% per annum. 4. 5. Rhino Ltd guarantees bank overdrafts of Lion Ltd for an unlimited amount. Assume that each ordinary share carries one vote and that voting rights alone determine control. It is group policy to show goodwill at cost less impairment in the consolidated financial statements. Goodwill was not impaired during the current financial year. REQUIRED: Part A Draft the following pro-forma consolidation journal entries of the Rhino Ltd Group for the year ended 31 December 2016, after taking the above- mentioned information into account: (a) Elimination of the owner's equity at acquisition. (b) Recording of the non-controlling interests' share in the revaluation surplus arising from the revaluation of property since acquisition. (c) Elimination the unrealised profit associated with the sale of the plant, as well as the depreciation associated with the sale. Please note: Indicate clearly to which company each account refers. Journal narrations are not required. Show all calculations and round all amounts to the nearest Rand. Ignore the taxation effect on unrealised profits and/or losses, as well as capital gains tax. Marks 7 2½ 8½ [18] ASSIGNMENT 02 (First semester) (continue) Part B FAC2602/101 Prepare only the following columns of the consolidated statement of changes in equity of the Rhino Ltd Group for the year ended 31 December 2016: Revaluation surplus Retained earnings Non-controlling interests Please note: Your answer should comply with the requirements of the International Financial Reporting Standards (IFRS). Show all calculations and round all amounts to the nearest Rand. Ignore the taxation effect on unrealised profits and/or losses, as well as capital gains tax. Notes to the consolidated statements are not required. Marks 22 [22] Rhino Ltd is incorporated in South Africa and listed on the JSE. Rhino Ltd manufactures outdoor and safari equipment. Lion Ltd is a tourism company that focuses on bringing international travellers to South Africa. The information below represents the trial balances of Rhino Ltd and its subsidiary, Lion Ltd as at 31 December 2016: Debits Property, plant and equipment at carrying amount Investment in Lion Ltd at fair value (cost price: R800 000) Loan to Lion Ltd Inventories Trade and other receivables Bank - Giraffe Bank Dividends paid - 31 December 2016 Cost of sales Other expenses Income tax expense Credits Share capital - ordinary shares (250 000/125 000 shares) Revaluation surplus - 1 January 2016 Retained earnings - 1 January 2016 Long-term borrowings Loan from Rhino Ltd Bank overdraft - Monkey Bank Trade and other payables Sales Rhino Ltd R 1 500 000 800 000 80 000 550 000 454 400 1 818 000 50 000 1 200 000 350 000 467 600 7 270 000 500 000 250 000 2 000 000 1 000 000 300 000 3 000 000 Lion Ltd R 2 500 000 700 000 1 399 000 20 000 1 000 000 390 000 380 800 6 389 800 250 000 100 000 1 500 000 1 300 000 80 000 9 800 400 000 2 500 000 Other income Additional information 220 000 7 270 000 1. Rhino Ltd acquired a 60% interest in Lion Ltd on 1 January 2013. On this date Lion Ltd's retained earnings amounted to R1 000 000 and the revaluation surplus amounted to R40 000. The issued share capital of both companies remained unchanged since the incorporations of the companies. 2. 250 000 6 389 800 3. Assume that the carrying amounts of all the assets and liabilities of Lion Bpk were considered to be equal to their respective fair values at acquisition. On 1 January 2014, property was revalued and this revaluation has been recorded in the records of Lion Ltd. Subsequently, there have been no other revaluations. ASSIGNMENT 02 (First semester) (continue) During the current year, Rhino Ltd started to sell inventory to Lion Ltd at a markup of 20% on cost. On 31 December 2016 there was inventory amounting to R120 000, that Rhino Ltd sold to Lion Ltd, included in the closing inventory of Lion Ltd. Rhino Ltd sold inventory amounting R500 000 to Lion Ltd in the current year. 27 On 1 January 2014, Lion Ltd sold one of their manufacturing plants to Rhino Ltd and made a profit of R100 000 on the transaction. It is the group's policy to recognise depreciation on plant and machinery on the straight-line method at a rate of 25% per annum. 4. 5. Rhino Ltd guarantees bank overdrafts of Lion Ltd for an unlimited amount. Assume that each ordinary share carries one vote and that voting rights alone determine control. It is group policy to show goodwill at cost less impairment in the consolidated financial statements. Goodwill was not impaired during the current financial year. REQUIRED: Part A Draft the following pro-forma consolidation journal entries of the Rhino Ltd Group for the year ended 31 December 2016, after taking the above- mentioned information into account: (a) Elimination of the owner's equity at acquisition. (b) Recording of the non-controlling interests' share in the revaluation surplus arising from the revaluation of property since acquisition. (c) Elimination the unrealised profit associated with the sale of the plant, as well as the depreciation associated with the sale. Please note: Indicate clearly to which company each account refers. Journal narrations are not required. Show all calculations and round all amounts to the nearest Rand. Ignore the taxation effect on unrealised profits and/or losses, as well as capital gains tax. Marks 7 2½ 8½ [18] ASSIGNMENT 02 (First semester) (continue) Part B FAC2602/101 Prepare only the following columns of the consolidated statement of changes in equity of the Rhino Ltd Group for the year ended 31 December 2016: Revaluation surplus Retained earnings Non-controlling interests Please note: Your answer should comply with the requirements of the International Financial Reporting Standards (IFRS). Show all calculations and round all amounts to the nearest Rand. Ignore the taxation effect on unrealised profits and/or losses, as well as capital gains tax. Notes to the consolidated statements are not required. Marks 22 [22] Rhino Ltd is incorporated in South Africa and listed on the JSE. Rhino Ltd manufactures outdoor and safari equipment. Lion Ltd is a tourism company that focuses on bringing international travellers to South Africa. The information below represents the trial balances of Rhino Ltd and its subsidiary, Lion Ltd as at 31 December 2016: Debits Property, plant and equipment at carrying amount Investment in Lion Ltd at fair value (cost price: R800 000) Loan to Lion Ltd Inventories Trade and other receivables Bank - Giraffe Bank Dividends paid - 31 December 2016 Cost of sales Other expenses Income tax expense Credits Share capital - ordinary shares (250 000/125 000 shares) Revaluation surplus - 1 January 2016 Retained earnings - 1 January 2016 Long-term borrowings Loan from Rhino Ltd Bank overdraft - Monkey Bank Trade and other payables Sales Rhino Ltd R 1 500 000 800 000 80 000 550 000 454 400 1 818 000 50 000 1 200 000 350 000 467 600 7 270 000 500 000 250 000 2 000 000 1 000 000 300 000 3 000 000 Lion Ltd R 2 500 000 700 000 1 399 000 20 000 1 000 000 390 000 380 800 6 389 800 250 000 100 000 1 500 000 1 300 000 80 000 9 800 400 000 2 500 000 Other income Additional information 220 000 7 270 000 1. Rhino Ltd acquired a 60% interest in Lion Ltd on 1 January 2013. On this date Lion Ltd's retained earnings amounted to R1 000 000 and the revaluation surplus amounted to R40 000. The issued share capital of both companies remained unchanged since the incorporations of the companies. 2. 250 000 6 389 800 3. Assume that the carrying amounts of all the assets and liabilities of Lion Bpk were considered to be equal to their respective fair values at acquisition. On 1 January 2014, property was revalued and this revaluation has been recorded in the records of Lion Ltd. Subsequently, there have been no other revaluations. ASSIGNMENT 02 (First semester) (continue) During the current year, Rhino Ltd started to sell inventory to Lion Ltd at a markup of 20% on cost. On 31 December 2016 there was inventory amounting to R120 000, that Rhino Ltd sold to Lion Ltd, included in the closing inventory of Lion Ltd. Rhino Ltd sold inventory amounting R500 000 to Lion Ltd in the current year. 27 On 1 January 2014, Lion Ltd sold one of their manufacturing plants to Rhino Ltd and made a profit of R100 000 on the transaction. It is the group's policy to recognise depreciation on plant and machinery on the straight-line method at a rate of 25% per annum. 4. 5. Rhino Ltd guarantees bank overdrafts of Lion Ltd for an unlimited amount. Assume that each ordinary share carries one vote and that voting rights alone determine control. It is group policy to show goodwill at cost less impairment in the consolidated financial statements. Goodwill was not impaired during the current financial year. REQUIRED: Part A Draft the following pro-forma consolidation journal entries of the Rhino Ltd Group for the year ended 31 December 2016, after taking the above- mentioned information into account: (a) Elimination of the owner's equity at acquisition. (b) Recording of the non-controlling interests' share in the revaluation surplus arising from the revaluation of property since acquisition. (c) Elimination the unrealised profit associated with the sale of the plant, as well as the depreciation associated with the sale. Please note: Indicate clearly to which company each account refers. Journal narrations are not required. Show all calculations and round all amounts to the nearest Rand. Ignore the taxation effect on unrealised profits and/or losses, as well as capital gains tax. Marks 7 2½ 8½ [18] ASSIGNMENT 02 (First semester) (continue) Part B FAC2602/101 Prepare only the following columns of the consolidated statement of changes in equity of the Rhino Ltd Group for the year ended 31 December 2016: Revaluation surplus Retained earnings Non-controlling interests Please note: Your answer should comply with the requirements of the International Financial Reporting Standards (IFRS). Show all calculations and round all amounts to the nearest Rand. Ignore the taxation effect on unrealised profits and/or losses, as well as capital gains tax. Notes to the consolidated statements are not required. Marks 22 [22] Rhino Ltd is incorporated in South Africa and listed on the JSE. Rhino Ltd manufactures outdoor and safari equipment. Lion Ltd is a tourism company that focuses on bringing international travellers to South Africa. The information below represents the trial balances of Rhino Ltd and its subsidiary, Lion Ltd as at 31 December 2016: Debits Property, plant and equipment at carrying amount Investment in Lion Ltd at fair value (cost price: R800 000) Loan to Lion Ltd Inventories Trade and other receivables Bank - Giraffe Bank Dividends paid - 31 December 2016 Cost of sales Other expenses Income tax expense Credits Share capital - ordinary shares (250 000/125 000 shares) Revaluation surplus - 1 January 2016 Retained earnings - 1 January 2016 Long-term borrowings Loan from Rhino Ltd Bank overdraft - Monkey Bank Trade and other payables Sales Rhino Ltd R 1 500 000 800 000 80 000 550 000 454 400 1 818 000 50 000 1 200 000 350 000 467 600 7 270 000 500 000 250 000 2 000 000 1 000 000 300 000 3 000 000 Lion Ltd R 2 500 000 700 000 1 399 000 20 000 1 000 000 390 000 380 800 6 389 800 250 000 100 000 1 500 000 1 300 000 80 000 9 800 400 000 2 500 000 Other income Additional information 220 000 7 270 000 1. Rhino Ltd acquired a 60% interest in Lion Ltd on 1 January 2013. On this date Lion Ltd's retained earnings amounted to R1 000 000 and the revaluation surplus amounted to R40 000. The issued share capital of both companies remained unchanged since the incorporations of the companies. 2. 250 000 6 389 800 3. Assume that the carrying amounts of all the assets and liabilities of Lion Bpk were considered to be equal to their respective fair values at acquisition. On 1 January 2014, property was revalued and this revaluation has been recorded in the records of Lion Ltd. Subsequently, there have been no other revaluations. ASSIGNMENT 02 (First semester) (continue) During the current year, Rhino Ltd started to sell inventory to Lion Ltd at a markup of 20% on cost. On 31 December 2016 there was inventory amounting to R120 000, that Rhino Ltd sold to Lion Ltd, included in the closing inventory of Lion Ltd. Rhino Ltd sold inventory amounting R500 000 to Lion Ltd in the current year. 27 On 1 January 2014, Lion Ltd sold one of their manufacturing plants to Rhino Ltd and made a profit of R100 000 on the transaction. It is the group's policy to recognise depreciation on plant and machinery on the straight-line method at a rate of 25% per annum. 4. 5. Rhino Ltd guarantees bank overdrafts of Lion Ltd for an unlimited amount. Assume that each ordinary share carries one vote and that voting rights alone determine control. It is group policy to show goodwill at cost less impairment in the consolidated financial statements. Goodwill was not impaired during the current financial year. REQUIRED: Part A Draft the following pro-forma consolidation journal entries of the Rhino Ltd Group for the year ended 31 December 2016, after taking the above- mentioned information into account: (a) Elimination of the owner's equity at acquisition. (b) Recording of the non-controlling interests' share in the revaluation surplus arising from the revaluation of property since acquisition. (c) Elimination the unrealised profit associated with the sale of the plant, as well as the depreciation associated with the sale. Please note: Indicate clearly to which company each account refers. Journal narrations are not required. Show all calculations and round all amounts to the nearest Rand. Ignore the taxation effect on unrealised profits and/or losses, as well as capital gains tax. Marks 7 2½ 8½ [18] ASSIGNMENT 02 (First semester) (continue) Part B FAC2602/101 Prepare only the following columns of the consolidated statement of changes in equity of the Rhino Ltd Group for the year ended 31 December 2016: Revaluation surplus Retained earnings Non-controlling interests Please note: Your answer should comply with the requirements of the International Financial Reporting Standards (IFRS). Show all calculations and round all amounts to the nearest Rand. Ignore the taxation effect on unrealised profits and/or losses, as well as capital gains tax. Notes to the consolidated statements are not required. Marks 22 [22] Rhino Ltd is incorporated in South Africa and listed on the JSE. Rhino Ltd manufactures outdoor and safari equipment. Lion Ltd is a tourism company that focuses on bringing international travellers to South Africa. The information below represents the trial balances of Rhino Ltd and its subsidiary, Lion Ltd as at 31 December 2016: Debits Property, plant and equipment at carrying amount Investment in Lion Ltd at fair value (cost price: R800 000) Loan to Lion Ltd Inventories Trade and other receivables Bank - Giraffe Bank Dividends paid - 31 December 2016 Cost of sales Other expenses Income tax expense Credits Share capital - ordinary shares (250 000/125 000 shares) Revaluation surplus - 1 January 2016 Retained earnings - 1 January 2016 Long-term borrowings Loan from Rhino Ltd Bank overdraft - Monkey Bank Trade and other payables Sales Rhino Ltd R 1 500 000 800 000 80 000 550 000 454 400 1 818 000 50 000 1 200 000 350 000 467 600 7 270 000 500 000 250 000 2 000 000 1 000 000 300 000 3 000 000 Lion Ltd R 2 500 000 700 000 1 399 000 20 000 1 000 000 390 000 380 800 6 389 800 250 000 100 000 1 500 000 1 300 000 80 000 9 800 400 000 2 500 000 Other income Additional information 220 000 7 270 000 1. Rhino Ltd acquired a 60% interest in Lion Ltd on 1 January 2013. On this date Lion Ltd's retained earnings amounted to R1 000 000 and the revaluation surplus amounted to R40 000. The issued share capital of both companies remained unchanged since the incorporations of the companies. 2. 250 000 6 389 800 3. Assume that the carrying amounts of all the assets and liabilities of Lion Bpk were considered to be equal to their respective fair values at acquisition. On 1 January 2014, property was revalued and this revaluation has been recorded in the records of Lion Ltd. Subsequently, there have been no other revaluations. ASSIGNMENT 02 (First semester) (continue) During the current year, Rhino Ltd started to sell inventory to Lion Ltd at a markup of 20% on cost. On 31 December 2016 there was inventory amounting to R120 000, that Rhino Ltd sold to Lion Ltd, included in the closing inventory of Lion Ltd. Rhino Ltd sold inventory amounting R500 000 to Lion Ltd in the current year. 27 On 1 January 2014, Lion Ltd sold one of their manufacturing plants to Rhino Ltd and made a profit of R100 000 on the transaction. It is the group's policy to recognise depreciation on plant and machinery on the straight-line method at a rate of 25% per annum. 4. 5. Rhino Ltd guarantees bank overdrafts of Lion Ltd for an unlimited amount. Assume that each ordinary share carries one vote and that voting rights alone determine control. It is group policy to show goodwill at cost less impairment in the consolidated financial statements. Goodwill was not impaired during the current financial year. REQUIRED: Part A Draft the following pro-forma consolidation journal entries of the Rhino Ltd Group for the year ended 31 December 2016, after taking the above- mentioned information into account: (a) Elimination of the owner's equity at acquisition. (b) Recording of the non-controlling interests' share in the revaluation surplus arising from the revaluation of property since acquisition. (c) Elimination the unrealised profit associated with the sale of the plant, as well as the depreciation associated with the sale. Please note: Indicate clearly to which company each account refers. Journal narrations are not required. Show all calculations and round all amounts to the nearest Rand. Ignore the taxation effect on unrealised profits and/or losses, as well as capital gains tax. Marks 7 2½ 8½ [18] ASSIGNMENT 02 (First semester) (continue) Part B FAC2602/101 Prepare only the following columns of the consolidated statement of changes in equity of the Rhino Ltd Group for the year ended 31 December 2016: Revaluation surplus Retained earnings Non-controlling interests Please note: Your answer should comply with the requirements of the International Financial Reporting Standards (IFRS). Show all calculations and round all amounts to the nearest Rand. Ignore the taxation effect on unrealised profits and/or losses, as well as capital gains tax. Notes to the consolidated statements are not required. Marks 22 [22] Rhino Ltd is incorporated in South Africa and listed on the JSE. Rhino Ltd manufactures outdoor and safari equipment. Lion Ltd is a tourism company that focuses on bringing international travellers to South Africa. The information below represents the trial balances of Rhino Ltd and its subsidiary, Lion Ltd as at 31 December 2016: Debits Property, plant and equipment at carrying amount Investment in Lion Ltd at fair value (cost price: R800 000) Loan to Lion Ltd Inventories Trade and other receivables Bank - Giraffe Bank Dividends paid - 31 December 2016 Cost of sales Other expenses Income tax expense Credits Share capital - ordinary shares (250 000/125 000 shares) Revaluation surplus - 1 January 2016 Retained earnings - 1 January 2016 Long-term borrowings Loan from Rhino Ltd Bank overdraft - Monkey Bank Trade and other payables Sales Rhino Ltd R 1 500 000 800 000 80 000 550 000 454 400 1 818 000 50 000 1 200 000 350 000 467 600 7 270 000 500 000 250 000 2 000 000 1 000 000 300 000 3 000 000 Lion Ltd R 2 500 000 700 000 1 399 000 20 000 1 000 000 390 000 380 800 6 389 800 250 000 100 000 1 500 000 1 300 000 80 000 9 800 400 000 2 500 000 Other income Additional information 220 000 7 270 000 1. Rhino Ltd acquired a 60% interest in Lion Ltd on 1 January 2013. On this date Lion Ltd's retained earnings amounted to R1 000 000 and the revaluation surplus amounted to R40 000. The issued share capital of both companies remained unchanged since the incorporations of the companies. 2. 250 000 6 389 800 3. Assume that the carrying amounts of all the assets and liabilities of Lion Bpk were considered to be equal to their respective fair values at acquisition. On 1 January 2014, property was revalued and this revaluation has been recorded in the records of Lion Ltd. Subsequently, there have been no other revaluations. ASSIGNMENT 02 (First semester) (continue) During the current year, Rhino Ltd started to sell inventory to Lion Ltd at a markup of 20% on cost. On 31 December 2016 there was inventory amounting to R120 000, that Rhino Ltd sold to Lion Ltd, included in the closing inventory of Lion Ltd. Rhino Ltd sold inventory amounting R500 000 to Lion Ltd in the current year. 27 On 1 January 2014, Lion Ltd sold one of their manufacturing plants to Rhino Ltd and made a profit of R100 000 on the transaction. It is the group's policy to recognise depreciation on plant and machinery on the straight-line method at a rate of 25% per annum. 4. 5. Rhino Ltd guarantees bank overdrafts of Lion Ltd for an unlimited amount. Assume that each ordinary share carries one vote and that voting rights alone determine control. It is group policy to show goodwill at cost less impairment in the consolidated financial statements. Goodwill was not impaired during the current financial year. REQUIRED: Part A Draft the following pro-forma consolidation journal entries of the Rhino Ltd Group for the year ended 31 December 2016, after taking the above- mentioned information into account: (a) Elimination of the owner's equity at acquisition. (b) Recording of the non-controlling interests' share in the revaluation surplus arising from the revaluation of property since acquisition. (c) Elimination the unrealised profit associated with the sale of the plant, as well as the depreciation associated with the sale. Please note: Indicate clearly to which company each account refers. Journal narrations are not required. Show all calculations and round all amounts to the nearest Rand. Ignore the taxation effect on unrealised profits and/or losses, as well as capital gains tax. Marks 7 2½ 8½ [18] ASSIGNMENT 02 (First semester) (continue) Part B FAC2602/101 Prepare only the following columns of the consolidated statement of changes in equity of the Rhino Ltd Group for the year ended 31 December 2016: Revaluation surplus Retained earnings Non-controlling interests Please note: Your answer should comply with the requirements of the International Financial Reporting Standards (IFRS). Show all calculations and round all amounts to the nearest Rand. Ignore the taxation effect on unrealised profits and/or losses, as well as capital gains tax. Notes to the consolidated statements are not required. Marks 22 [22]

Expert Answer:

Answer rating: 100% (QA)

frefore the fillong Calumne a Consell dded stark met of equity of th... View the full answer

Related Book For

Financial and Managerial Accounting the basis for business decisions

ISBN: 978-0078111044

16th edition

Authors: Jan Williams, Susan Haka, Mark Bettner, Joseph Carcello

Posted Date:

Students also viewed these accounting questions

-

As at 31 December 2019, Portal Development Limited (PD) has trade receivables of HK$20,000,000 overdue for more than one year. After some rounds of tough negotiation with the auditor, PD finally...

-

The adjusted trial balances of Pin Corporation and its 80 percent-owned subsidiary, Son Corporation, at December 31, 2012, are as follows (in thousands): Pin acquired its interest in Son for $640,000...

-

The adjusted trial balances of Pop Corporation and its 80 percent-owned subsidiary, Son Corporation, at December 31, 2017, are as follows (in thousands): Pop acquired its interest in Son for...

-

Q4 11 Points 4. Consider the following Current Data for ABC Corp.: Debt Equity Market Value (in millions of $) 16,000 26,000 Cost 7% 14% If ABC moves to and maintains a debt-to-value (D/V) ratio of...

-

Mr. Larry Leininger donated $3,000,000 to a nongovernment VHWO on June 17, 20X8. 1. Assume that no restrictions are placed on the use of the donated resources. a. Prepare the required June 17, 20X8,...

-

Find the nth term of the geometric sequence with the given values. 125,25, 5, . . . ; n = 7

-

Which of the following is most likely to provide management with incentives to overstate earnings? a. Projected quarterly dividends. b. Issuance of preferred stock. c. Unbudgeted increases in...

-

Victor sells to Bonnie a refrigerator for $600 payable in monthly installments of $30 for twenty months. Bonnie signs a security agreement granting Victor a security interest in the refrigerator. The...

-

In the figure below, q = 92 = -27.0 C, and the charges are separated by d = 10.0 cm. If q is located at x = 0.00 cm, find the electric potential at the midpoint between the two charges (x = 5.00 cm)....

-

1. Describe the leadership style of David Norris? Include in your explanation the nature of the relationship he had with Lindsay Farrow. 2. Do you consider the decisions made by Norris dysfunctional...

-

A researcher has designed the relationship between the salaries of 100 selected employees of an organization (shown as "EARN" in $/hour) and their years of education (shown as "YRSEDUC", in years)...

-

7) A rigid bar is supported by three rods in same vertical plane and equi distant. The outer rods are of brass and of length 600mm and diameter 30mm. The central rod is of steel of 900 mm length and...

-

3 A block of mass M-25 kg is attached to the cord wound on the drum of diameter 100 mm and it is allowed to fall under the action of gravity (see Figure B3). The drum is firmly attached to gear A,...

-

(b) The following C++ function multiplies natural numbers x and y by repeated addition. Derive, and prove correct, the number of "+" operations this method executes. int multiply (int x, int y) ( }...

-

4. 5. A drug is to be sold in gelatin capsules, which have an approximately cylindrical shape. To hold the required dosage, the capsules must have a volume of 120 cubic millimeters. What are the...

-

The belt in the given image moves at a steady velocity Vand skims the top of a tank of oil of viscosity J. + Of Oil, depth h Moving belt, width b What power P in watts is required if the belt moves...

-

Design 4-bar a mechanism which will do the following crank angle woordination: assuming that ground link is 10 cm. Pos 1: Pos 2: Pas 3: 60 (K 120 Find the link. . mechanism corresponding 04 90 1000...

-

Prove the following D,(cos x) = - sin x (Hint: Apply the identity cos(A + B) = cos A cos B sin A sin B)

-

The realization principle determines when a business should recognize revenue. Listed next are three common business situations involving revenue. After each situation, we give two alternatives as to...

-

An activity analysis at Loafs End Bread Company found the following activities for its bread makers: 10 percent of time, adding ingredients; 60 percent of time, mixing and kneading dough; 10 percent...

-

Fire Code manufactures smoke detectors that are sold to homeowners throughout the United States at $20 apiece. Each detector is equipped with a sensory cell that is guaranteed to last two full years...

-

Use a stem-and-leaf plot to display the data, which represent the numbers of hours 24 students study per week. Organize the data using the indicated type of graph. Describe any patterns. 20 24 25 18...

-

Use a stem-and-leaf plot to display the data, which represent the runs scored by a batsman in a World Cup series. Organize the data using the indicated type of graph. Describe any patterns. 70 75 71...

-

Use a stem-and-leaf plot to display the data shown in the table at the left, which represent the drunk driving cases registered at 30 strategic road intersections. Organize the data using the...

Study smarter with the SolutionInn App