Robert Ltd acquired all the issued shares ( cum div. ) of Matt Ltd on 1 July

Question:

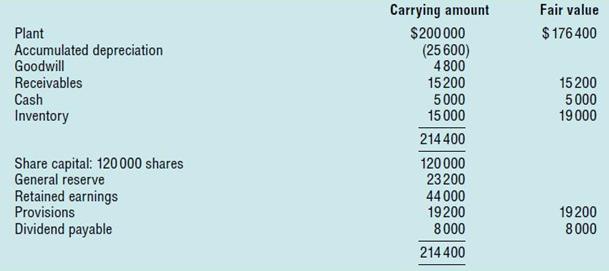

Robert Ltd acquired all the issued shares (cum div.) of Matt Ltd on 1 July 2015. At this date the financial position of Matt Ltd was as follows:

The assets of Matt Ltd did not include a patent that was valued by Robert Ltd at $10 000. Its useful life was considered to be 5 years, with benefits being received equally over that period. The plant was considered to have a further 10-year life and is depreciated on a straight-line basis. All the inventory was sold by 30 June 2016. The goodwill on hand at 1 July 2015 was written off as the result of an impairment test conducted in June 2017. The dividend on hand at 1 July 2015 was paid in August 2015.

In exchange for the shares in Matt Ltd, Robert Ltd gave the following consideration:

- 50 000 shares in Robert Ltd, each share having a fair value of $2.00 per share.

- Cash of $40 000.

- Artworks having a fair value of $60 000.

Robert Ltd incurred legal and accounting costs of $5000 and share issue costs of $4000.

In January 2019, Matt Ltd paid a bonus dividend of $40 000, being one share for every three shares held, the dividend being paid from retained earnings on hand at 1 July 2015. The tax rate is 30%.

Required

Prepare the consolidation worksheet entries for consolidated financial statements prepared by Robert Ltd at 30 June 2020.

Expert Answer:

Financial Accounting and Reporting

ISBN: 978-0273744443

14th Edition

Authors: Barry Elliott, Jamie Elliott