Question: scenerio above, please complete question with full working out shown to each question before answering it thanks. Fenton Ltd - continued: Fenton Ltd - Production

scenerio above, please complete question with full working out shown to each question before answering it thanks.

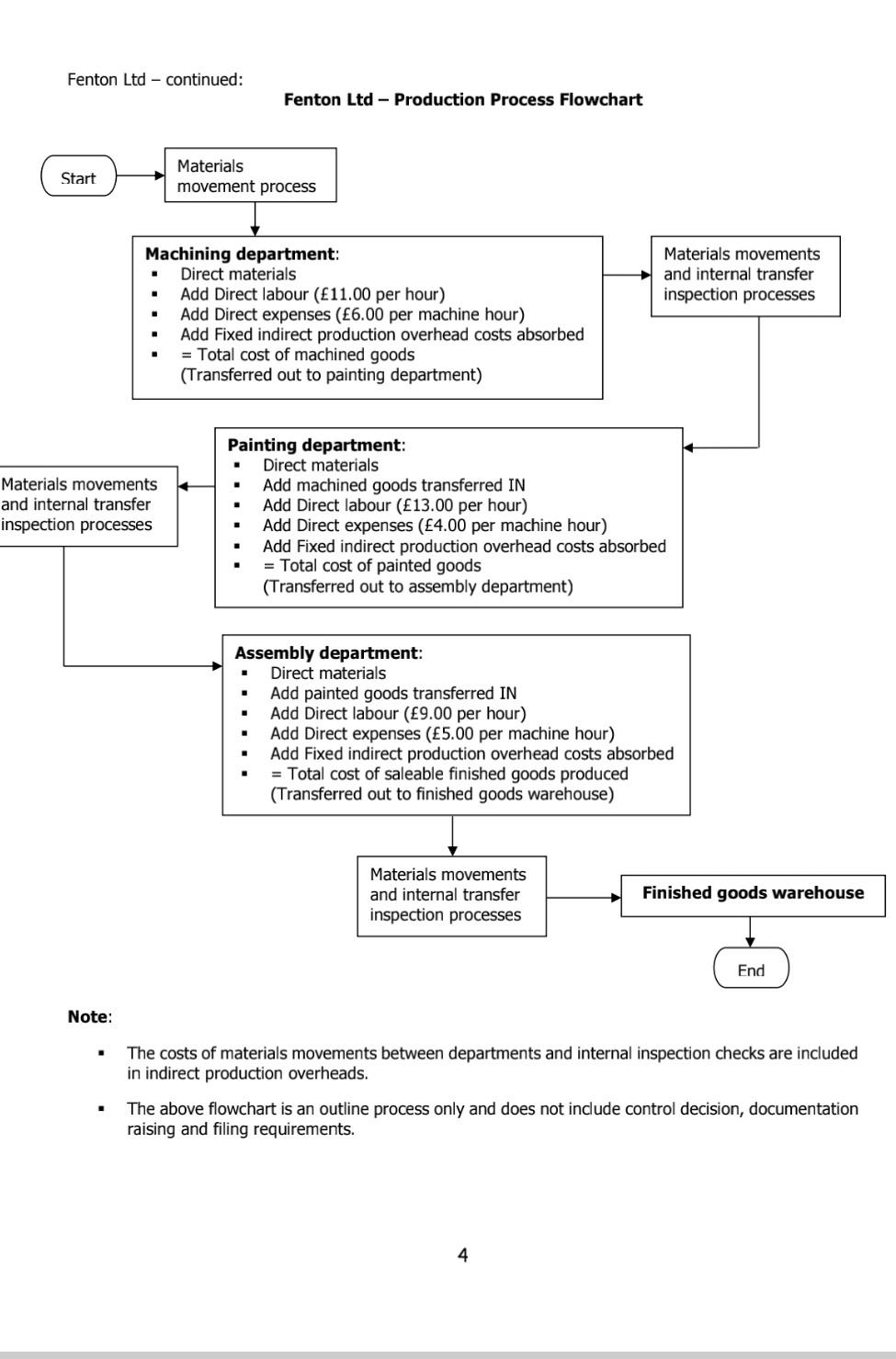

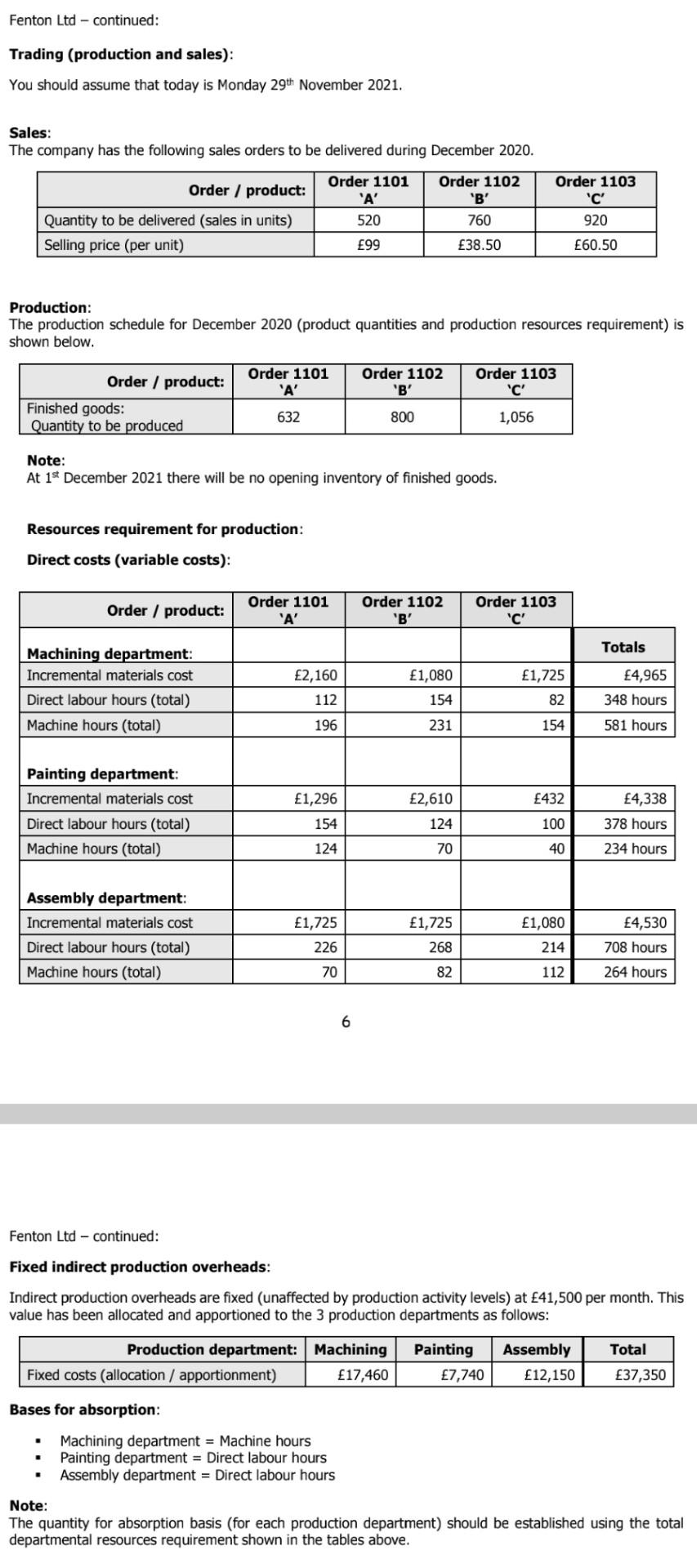

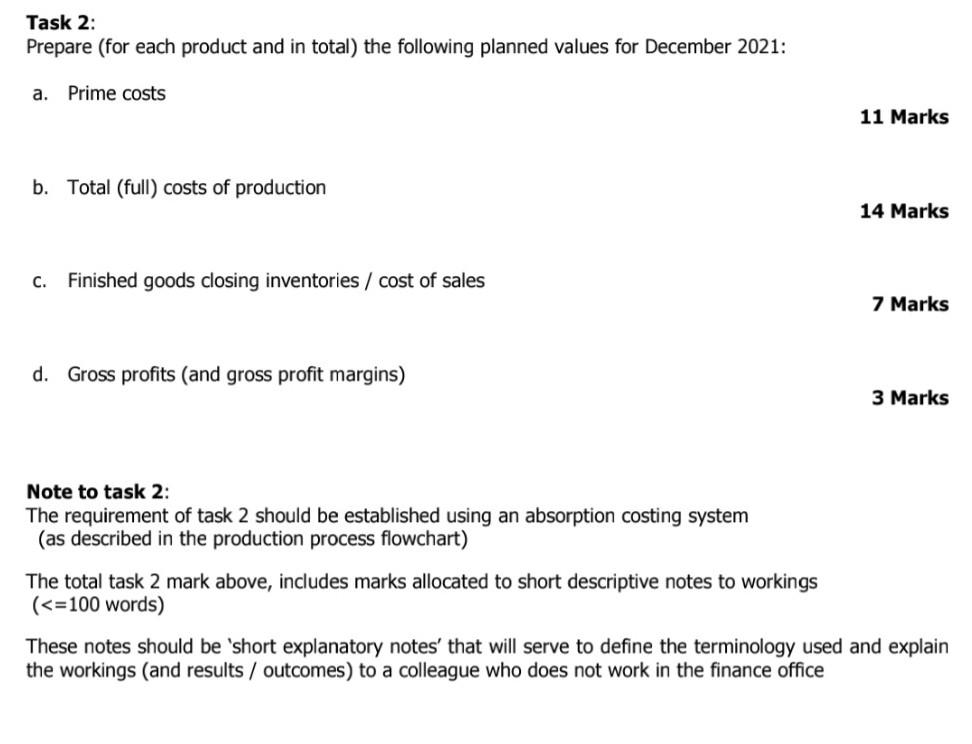

Fenton Ltd - continued: Fenton Ltd - Production Process Flowchart Start Materials movement process . Materials movements and internal transfer inspection processes Machining department: Direct materials Add Direct labour (11.00 per hour) Add Direct expenses (6.00 per machine hour) Add Fixed indirect production overhead costs absorbed = Total cost of machined goods (Transferred out to painting department) Materials movements and internal transfer inspection processes Painting department: Direct materials Add machined goods transferred IN Add Direct labour (13.00 per hour) Add Direct expenses (4.00 per machine hour) Add Fixed indirect production overhead costs absorbed = Total cost of painted goods (Transferred out to assembly department) Assembly department: Direct materials Add painted goods transferred IN Add Direct labour (9.00 per hour) Add Direct expenses (5.00 per machine hour) Add Fixed indirect production overhead costs absorbed = Total cost of saleable finished goods produced (Transferred out to finished goods warehouse) . Materials movements and internal transfer inspection processes Finished goods warehouse End Note: . The costs of materials movements between departments and internal inspection checks are included in indirect production overheads. The above flowchart is an outline process only and does not include control decision, documentation raising and filing requirements. . 4 Fenton Ltd - continued: Trading (production and sales): You should assume that today is Monday 29th November 2021. Sales: The company has the following sales orders to be delivered during December 2020. Order/product: Quantity to be delivered (sales in units) Selling price (per unit) Order 1101 'A' 520 Order 1102 'B' 760 Order 1103 'C' 920 99 38.50 60.50 Production: The production schedule for December 2020 (product quantities and production resources requirement) is shown below. Order 1101 'A' Order 1102 'B' Order 1103 'C' Order / product: Finished goods: Quantity to be produced 632 800 1,056 Note: At 15 December 2021 there will be no opening inventory of finished goods. Resources requirement for production: Direct costs (variable costs): Order / product: Order 1101 'A' Order 1102 'B' Order 1103 'C' Totals 2,160 Machining department: Incremental materials cost Direct labour hours (total) Machine hours (total) 1,080 154 1,725 82 4,965 348 hours 112 196 231 154 581 hours 2,610 432 Painting department: Incremental materials cost Direct labour hours (total) Machine hours (total) 1,296 154 4,338 378 hours 124 100 124 70 40 234 hours Assembly department: Incremental materials cost Direct labour hours (total) Machine hours (total) 1,725 226 1,725 268 1,080 214 4,530 708 hours 70 82 112 264 hours 6 Fenton Ltd - continued: Fixed indirect production overheads: Indirect production overheads are fixed (unaffected by production activity levels) at 41,500 per month. This value has been allocated and apportioned to the 3 production departments as follows: Production department: Machining Painting Assembly Total Fixed costs (allocation / apportionment) 17,460 7,740 12,150 37,350 Bases for absorption: Machining department = Machine hours Painting department = Direct labour hours Assembly department = Direct labour hours Note: The quantity for absorption basis (for each production department) should be established using the total departmental resources requirement shown in the tables above. Task 2: Prepare (for each product and in total) the following planned values for December 2021: a. Prime costs 11 Marks b. Total (full) costs of production 14 Marks C. Finished goods closing inventories / cost of sales 7 Marks d. Gross profits (and gross profit margins) 3 Marks Note to task 2: The requirement of task 2 should be established using an absorption costing system (as described in the production process flowchart) The total task 2 mark above, includes marks allocated to short descriptive notes to workings (

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts