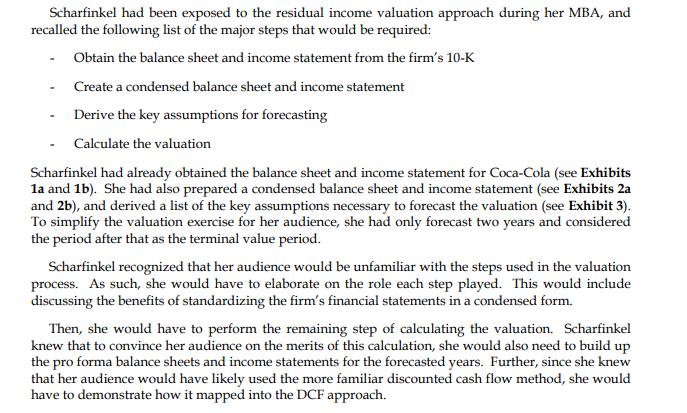

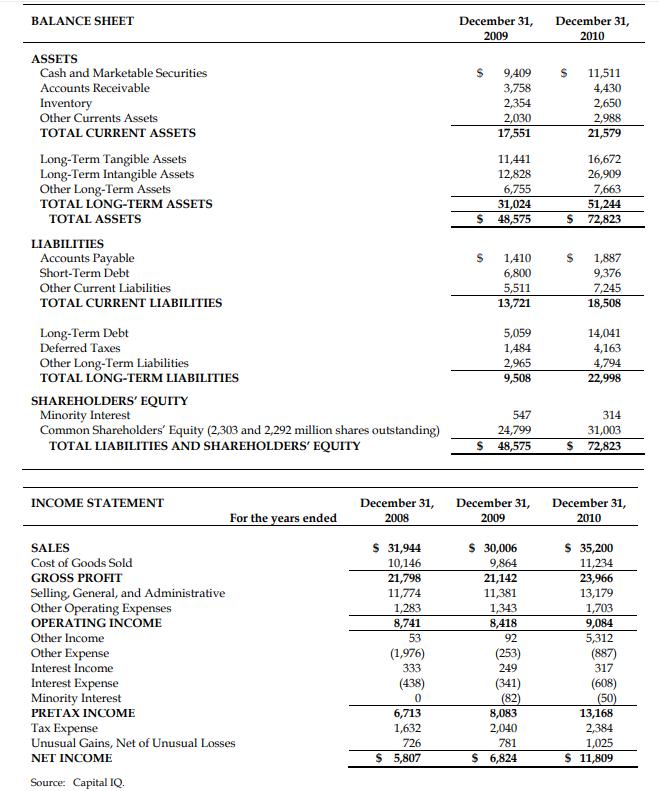

Scharfinkel had been exposed to the residual income valuation approach during her MBA, and recalled the...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

Scharfinkel had been exposed to the residual income valuation approach during her MBA, and recalled the following list of the major steps that would be required: Obtain the balance sheet and income statement from the firm's 10-K Create a condensed balance sheet and income statement Derive the key assumptions for forecasting Calculate the valuation Scharfinkel had already obtained the balance sheet and income statement for Coca-Cola (see Exhibits 1a and 1b). She had also prepared a condensed balance sheet and income statement (see Exhibits 2a and 2b), and derived a list of the key assumptions necessary to forecast the valuation (see Exhibit 3). To simplify the valuation exercise for her audience, she had only forecast two years and considered the period after that as the terminal value period. Scharfinkel recognized that her audience would be unfamiliar with the steps used in the valuation process. As such, she would have to elaborate on the role each step played. This would include discussing the benefits of standardizing the firm's financial statements in a condensed form. Then, she would have to perform the remaining step of calculating the valuation. Scharfinkel knew that to convince her audience on the merits of this calculation, she would also need to build up the pro forma balance sheets and income statements for the forecasted years. Further, since she knew that her audience would have likely used the more familiar discounted cash flow method, she would have to demonstrate how it mapped into the DCF approach. BALANCE SHEET ASSETS Cash and Marketable Securities Accounts Receivable Inventory Other Currents Assets TOTAL CURRENT ASSETS Long-Term Tangible Assets Long-Term Intangible Assets Other Long-Term Assets TOTAL LONG-TERM ASSETS TOTAL ASSETS LIABILITIES Accounts Payable Short-Term Debt Other Current Liabilities TOTAL CURRENT LIABILITIES Long-Term Debt Deferred Taxes Other Long-Term Liabilities TOTAL LONG-TERM LIABILITIES SHAREHOLDERS' EQUITY Minority Interest Common Shareholders' Equity (2,303 and 2,292 million shares outstanding) TOTAL LIABILITIES AND SHAREHOLDERS' EQUITY INCOME STATEMENT SALES Cost of Goods Sold GROSS PROFIT Selling, General, and Administrative Other Operating Expenses OPERATING INCOME Other Income Other Expense Interest Income Interest Expense Minority Interest PRETAX INCOME For the years ended Tax Expense Unusual Gains, Net of Unusual Losses NET INCOME Source: Capital IQ. December 31, 2008 $ 31,944 10,146 21,798 11,774 1,283 8,741 53 (1,976) 333 (438) 0 6,713 1,632 726 $ 5,807 December 31, 2009 S 9,409 3,758 2,354 2,030 17,551 11,441 12,828 6,755 31,024 $ 48,575 $ 1,410 6,800 5,511 13,721 5,059 1,484 2,965 9,508 547 24,799 $ 48,575 December 31, 2009 $ 30,006 9,864 21,142 11,381 1,343 8,418 92 (253) 249 (341) (82) 8,083 2,040 781 $ 6,824 December 31, 2010 $ 11,511 4,430 2,650 2,988 21,579 $ 16,672 26,909 7,663 51,244 $ 72,823 1,887 9,376 7,245 18,508 14,041 4,163 4,794 22,998 314 31,003 $ 72,823 December 31, 2010 $ 35,200 11,234 23,966 13,179 1,703 9,084 5,312 (887) 317 (608) (50) 13,168 2,384 1,025 $ 11,809. Beginning Net Working Capital Beginning Net Long-Term Assets NET OPERATING ASSETS For the year ending Sales NOPAT Net Interest Expense After Tax NET INCOME Less: Preferred Dividends NET INCOME TO COMMON SHAREHOLDERS Source: Casewriter. Net Debt Preferred Stock Shareholders' Equity NET CAPITAL Exhibit 2b Coca-Cola, Condensed Income Statement (in $ millions) Exhibit 3 Coca-Cola, Forecasting Assumptions Panel A. Cost of Capital Parameters Market Risk Premium Risk-Free Rate Tax Rate Cost of Debt Common Equity Beta Panel B. Future Performance Forecasts Sales Growth Rate NOPAT/ Sales Beginning Net Operating Working Capital / Sales Beginning Net Operating Long-Term Assets / Sales As of Net Debt / Book Value of Net Capital Preferred Equity / Book Value of Net Capital Shareholders' Equity / Book Value of Net Capital Source: Casewriter. January 1, 2009 $ $ 740 24,065 24,805 $ December 31, 2008 $ 4,333 0 20,472 24,805 31,944 5,886 79 5,807 0 5,807 2011 10.0% 20.0% 27.75% 0.0% 72.25% January 1, 2010 $ 1,221 26,028 27,249 2,450 0 24,799 $ 27,249 December 31, 2009 $ $ 31,006 6,892 69 6,824 0 6,824 5.0% 3.0% 35.0% 4.5% 0.6 2012 8.0% 20.0% 3.0% 105.0% 27.75% 0.0% 72.25% January 1, 2011 $ 936 41,973 42,909 11,906 0 31,003 $ 42,909 December 31, 2010 $ 35,200 12,047 238 11,809 0 $ 11,809 Terminal 3.0% 15.0% 3.0% 100.0% 27.75% 0.0% 72.25% Scharfinkel had been exposed to the residual income valuation approach during her MBA, and recalled the following list of the major steps that would be required: Obtain the balance sheet and income statement from the firm's 10-K Create a condensed balance sheet and income statement Derive the key assumptions for forecasting Calculate the valuation Scharfinkel had already obtained the balance sheet and income statement for Coca-Cola (see Exhibits 1a and 1b). She had also prepared a condensed balance sheet and income statement (see Exhibits 2a and 2b), and derived a list of the key assumptions necessary to forecast the valuation (see Exhibit 3). To simplify the valuation exercise for her audience, she had only forecast two years and considered the period after that as the terminal value period. Scharfinkel recognized that her audience would be unfamiliar with the steps used in the valuation process. As such, she would have to elaborate on the role each step played. This would include discussing the benefits of standardizing the firm's financial statements in a condensed form. Then, she would have to perform the remaining step of calculating the valuation. Scharfinkel knew that to convince her audience on the merits of this calculation, she would also need to build up the pro forma balance sheets and income statements for the forecasted years. Further, since she knew that her audience would have likely used the more familiar discounted cash flow method, she would have to demonstrate how it mapped into the DCF approach. BALANCE SHEET ASSETS Cash and Marketable Securities Accounts Receivable Inventory Other Currents Assets TOTAL CURRENT ASSETS Long-Term Tangible Assets Long-Term Intangible Assets Other Long-Term Assets TOTAL LONG-TERM ASSETS TOTAL ASSETS LIABILITIES Accounts Payable Short-Term Debt Other Current Liabilities TOTAL CURRENT LIABILITIES Long-Term Debt Deferred Taxes Other Long-Term Liabilities TOTAL LONG-TERM LIABILITIES SHAREHOLDERS' EQUITY Minority Interest Common Shareholders' Equity (2,303 and 2,292 million shares outstanding) TOTAL LIABILITIES AND SHAREHOLDERS' EQUITY INCOME STATEMENT SALES Cost of Goods Sold GROSS PROFIT Selling, General, and Administrative Other Operating Expenses OPERATING INCOME Other Income Other Expense Interest Income Interest Expense Minority Interest PRETAX INCOME For the years ended Tax Expense Unusual Gains, Net of Unusual Losses NET INCOME Source: Capital IQ. December 31, 2008 $ 31,944 10,146 21,798 11,774 1,283 8,741 53 (1,976) 333 (438) 0 6,713 1,632 726 $ 5,807 December 31, 2009 S 9,409 3,758 2,354 2,030 17,551 11,441 12,828 6,755 31,024 $ 48,575 $ 1,410 6,800 5,511 13,721 5,059 1,484 2,965 9,508 547 24,799 $ 48,575 December 31, 2009 $ 30,006 9,864 21,142 11,381 1,343 8,418 92 (253) 249 (341) (82) 8,083 2,040 781 $ 6,824 December 31, 2010 $ 11,511 4,430 2,650 2,988 21,579 $ 16,672 26,909 7,663 51,244 $ 72,823 1,887 9,376 7,245 18,508 14,041 4,163 4,794 22,998 314 31,003 $ 72,823 December 31, 2010 $ 35,200 11,234 23,966 13,179 1,703 9,084 5,312 (887) 317 (608) (50) 13,168 2,384 1,025 $ 11,809. Beginning Net Working Capital Beginning Net Long-Term Assets NET OPERATING ASSETS For the year ending Sales NOPAT Net Interest Expense After Tax NET INCOME Less: Preferred Dividends NET INCOME TO COMMON SHAREHOLDERS Source: Casewriter. Net Debt Preferred Stock Shareholders' Equity NET CAPITAL Exhibit 2b Coca-Cola, Condensed Income Statement (in $ millions) Exhibit 3 Coca-Cola, Forecasting Assumptions Panel A. Cost of Capital Parameters Market Risk Premium Risk-Free Rate Tax Rate Cost of Debt Common Equity Beta Panel B. Future Performance Forecasts Sales Growth Rate NOPAT/ Sales Beginning Net Operating Working Capital / Sales Beginning Net Operating Long-Term Assets / Sales As of Net Debt / Book Value of Net Capital Preferred Equity / Book Value of Net Capital Shareholders' Equity / Book Value of Net Capital Source: Casewriter. January 1, 2009 $ $ 740 24,065 24,805 $ December 31, 2008 $ 4,333 0 20,472 24,805 31,944 5,886 79 5,807 0 5,807 2011 10.0% 20.0% 27.75% 0.0% 72.25% January 1, 2010 $ 1,221 26,028 27,249 2,450 0 24,799 $ 27,249 December 31, 2009 $ $ 31,006 6,892 69 6,824 0 6,824 5.0% 3.0% 35.0% 4.5% 0.6 2012 8.0% 20.0% 3.0% 105.0% 27.75% 0.0% 72.25% January 1, 2011 $ 936 41,973 42,909 11,906 0 31,003 $ 42,909 December 31, 2010 $ 35,200 12,047 238 11,809 0 $ 11,809 Terminal 3.0% 15.0% 3.0% 100.0% 27.75% 0.0% 72.25%

Expert Answer:

Answer rating: 100% (QA)

Steps to calculate the residual income valuation for CocaCola using the information provided 1 Build ... View the full answer

Related Book For

Systems analysis and design

ISBN: 978-0136089162

8th Edition

Authors: kenneth e. kendall, julie e. kendall

Posted Date:

Students also viewed these corporate finance questions

-

List the data stores that would be required to implement the person registering in Problem 14

-

Explain the theory behind the residual income valuation approach. Why is residual income value-relevant to common equity shareholders?

-

Describe managerial skills and behaviors that would be required to manage effectively in a functional department. Are these skills and behaviors different from those required in a product department?...

-

Calculate the managerial remuneration from the following particulars of Zen Ltd. the company has only one Managing Director. Net Profit Net Profit is calculated after considering the following:...

-

According to the Associated Press report, 47 percent of parents who have purchased TV sets after V- chips became standard equipment in January 2000 are aware that their sets have V- chips, and of...

-

1. What is international market segmentation? What challenges does it pose to Bentley? 2. Using the full spectrum of segmentation variables, describe how Bentley segments and targets the...

-

The design for a Website is to consist of four colors, three fonts, and three positions for an image. From the multiplication rule, \(4 \times 3 \times 3=36\) different designs are possible.

-

Five years ago, Kennedy Trucking Company was considering the purchase of 60 new diesel trucks that were 15 percent more fuel-efficient than the ones the firm is now using. Mr. Hoffman, the president,...

-

Use Bayes' theorem or a tree diagram to calculate the indicated probability. Round your answer to four decimal places. P(Y1 | X) = 2' form a partition of S. P(X | Y) = 0.8, P(X | Y2) = 0.1, P(X | Y)...

-

Problem 9 (50 Points) An air-cooled aluminum heat sink is used to keep electronics cool (see image and diagram). The cooling requirements are being significantly increased. To increase the rate of...

-

Your assignment should have an introduction [2] Your assignment should have a conclusion [2] Cite your sources [2] Use the APA referencing system (Not less than three sources [2] Content [2] Submit...

-

Ben Rishi is operations manager for a factory making saucepans. The weekly maximum capacity of the factory is 3000 units. The main limit on capacity is the old-fashioned machine for stamping out the...

-

Evaluate If n is an even integer, then n - 1 is odd.

-

1) Rim. Inc. , which had earnigns and profits of 100,000, distributed and to Alex Rowe, a stockholder Pym's adjusted basis for this land was $3,000. The land had a fair market value of 12,000 and was...

-

Meadowland Clothing uses 3 yards of material for each garment produced. On May 1, Meadowland had 24 yards of material on hand. If Meadowland desires an ending inventory of 15 yards of material and...

-

Sunrise Pools, Inc., is being sued by the crescent club for negligence when installing a new pool on crescent club's property. Crescent club alleges that the employees of Sunrise Pools damaged the...

-

For the following program, (1) sketch the corresponding process tree being sure to indicate any outputs and synchronization points, if they exist and (2) write down the output it will produce when...

-

Open Text Corporation provides a suite of business information software products. Exhibit 10-9 contains Note 10 from the companys 2013 annual report detailing long-term debt. Required: a. Open Text...

-

Ive got the idea of the century! proclaims Bea Kwicke, a new systems analyst with your systems group. Lets skip all this SDLC garbage and just prototype everything. Our projects will go a lot more...

-

I dont need to see it very often, but when I do, I have to be able to get at it quickly. I think we lost the last contract because the information I needed was buried in a stack of paper on someones...

-

Clyde Clerk is reviewing his firms expense reimbursement policies with the new salesperson, Trav Farr. Our reimbursement policies depend on the situation. You see, first we determine if it is a...

-

An inborn error of metabolism is caused by a. a mutation in a gene that causes an enzyme to be inactive. b. a mutation in a gene that occurs in somatic cells. c. the consumption of foods that disrupt...

-

During the initiation stage of translation in bacteria, which of the following events occur(s)? a. IF1 and IF3 bind to the 30S subunit. b. The mRNA binds to the 30S subunit, and tRNAfMet binds to the...

-

Each ribosomal subunit is composed of a. multiple proteins. c. tRNA. b. rRNA. d. both a and b.

Study smarter with the SolutionInn App