Question: Section 85 permits the transferor to elect jointly with the transferee (the new subsidiary receiving the appreciated property) to fix an agreed amount, such as

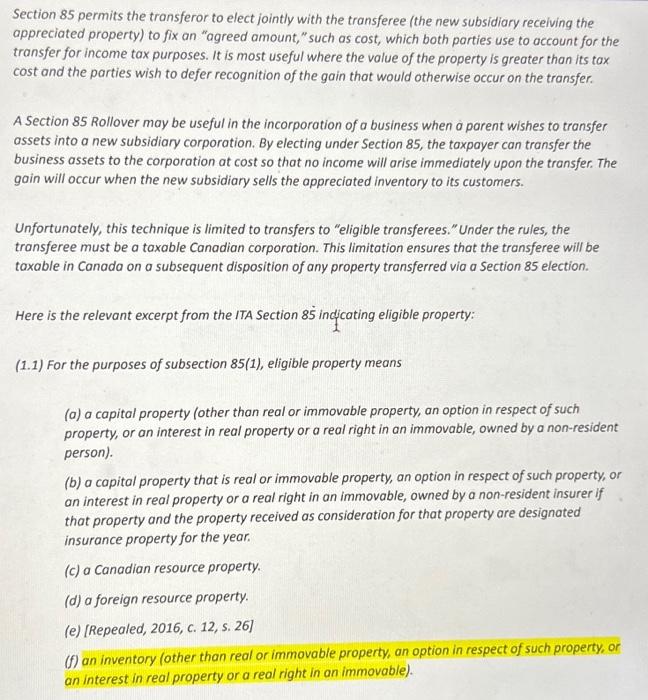

Section 85 permits the transferor to elect jointly with the transferee (the new subsidiary receiving the appreciated property) to fix an "agreed amount, "such as cost, which both parties use to account for the transfer for income tax purposes. It is most useful where the value of the property is greater than its tax cost and the parties wish to defer recognition of the gain that would otherwise occur on the transfer. A Section 85 Rollover may be useful in the incorporation of a business when a parent wishes to transfer assets into a new subsidiary corporation. By electing under Section 85, the taxpayer can transfer the business assets to the corporation at cost so that no income will arise immediately upon the transfer. The gain will occur when the new subsidiary sells the oppreciated inventory to its customers. Unfortunately, this technique is limited to transfers to "eligible transferees." Under the rules, the transferee must be a taxable Canadian corporation. This limitation ensures that the transferee will be taxable in Canada on a subsequent disposition of any property transferred via a section 85 election. Here is the relevant excerpt from the ITA Section 85 indicating eligible property: (1.1) For the purposes of subsection 85(1), eligible property means (a) a capital property (other than real or immovable property, an option in respect of such property, or an interest in real property or a real right in an immovable, owned by a non-resident person). (b) a capital property that is real or immovable property, an option in respect of such property, or an interest in real property or a real right in an immovable, owned by a non-resident insurer if that property and the property received as consideration for that property are designated insurance property for the year. (c) a Canadian resource property. (d) a foreign resource property. (e) [Repealed, 2016, c. 12, s. 26] (f) an inventory (other than real or immovable property, an option in respect of such property, or an interest in real property or a real right in an immovable). Section 85 permits the transferor to elect jointly with the transferee (the new subsidiary receiving the appreciated property) to fix an "agreed amount, "such as cost, which both parties use to account for the transfer for income tax purposes. It is most useful where the value of the property is greater than its tax cost and the parties wish to defer recognition of the gain that would otherwise occur on the transfer. A Section 85 Rollover may be useful in the incorporation of a business when a parent wishes to transfer assets into a new subsidiary corporation. By electing under Section 85, the taxpayer can transfer the business assets to the corporation at cost so that no income will arise immediately upon the transfer. The gain will occur when the new subsidiary sells the oppreciated inventory to its customers. Unfortunately, this technique is limited to transfers to "eligible transferees." Under the rules, the transferee must be a taxable Canadian corporation. This limitation ensures that the transferee will be taxable in Canada on a subsequent disposition of any property transferred via a section 85 election. Here is the relevant excerpt from the ITA Section 85 indicating eligible property: (1.1) For the purposes of subsection 85(1), eligible property means (a) a capital property (other than real or immovable property, an option in respect of such property, or an interest in real property or a real right in an immovable, owned by a non-resident person). (b) a capital property that is real or immovable property, an option in respect of such property, or an interest in real property or a real right in an immovable, owned by a non-resident insurer if that property and the property received as consideration for that property are designated insurance property for the year. (c) a Canadian resource property. (d) a foreign resource property. (e) [Repealed, 2016, c. 12, s. 26] (f) an inventory (other than real or immovable property, an option in respect of such property, or an interest in real property or a real right in an immovable)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts