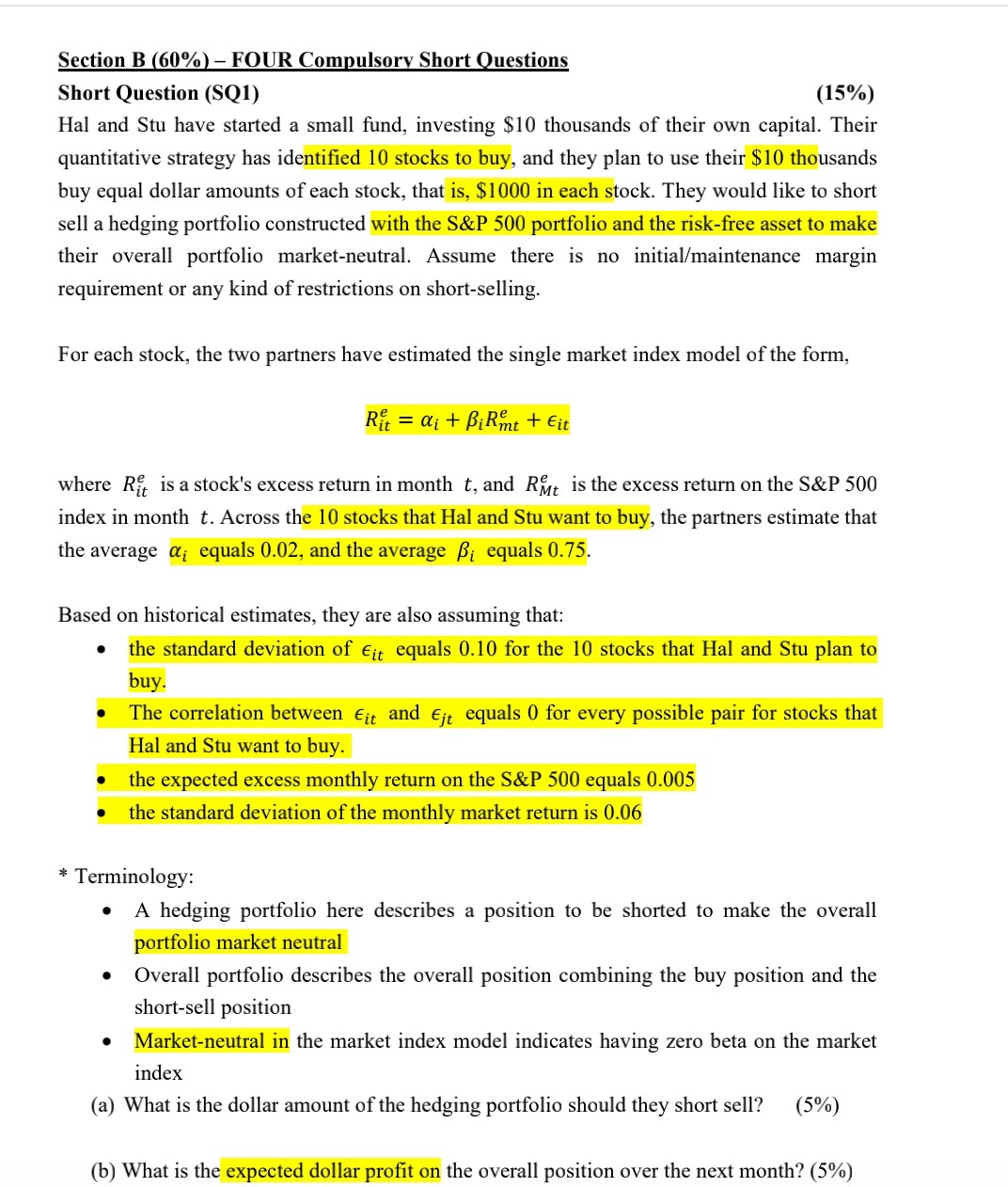

Question: Section B 60% FOUR Com ulsor Short uestions Short Question {SQI} (15%) Hal and Stu have started a small fund, investing $10 thousands of their

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock