Question: Section - II Answer both the questions Make necessary assumptions wherever required Word limit: 400-600 words for 10 marks Read the case*and answer the following

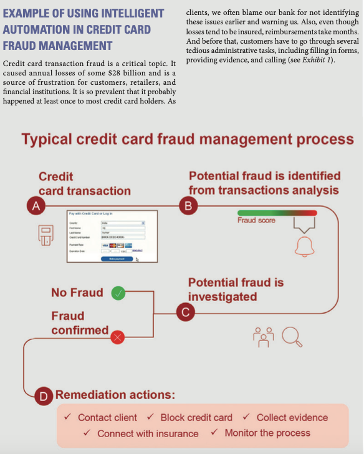

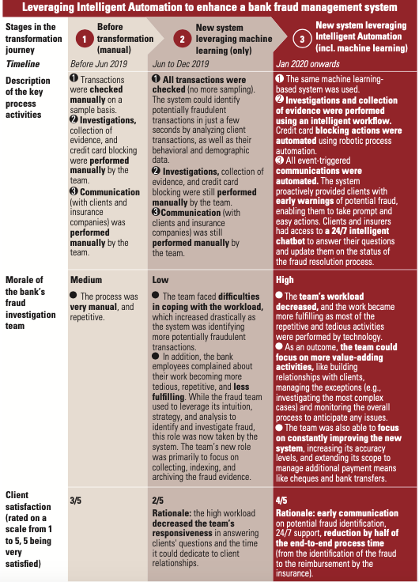

Section - II Answer both the questions Make necessary assumptions wherever required Word limit: 400-600 words for 10 marks Read the case*and answer the following questions: Im concerned about the speed and scope top management pushes our digital transformation, said Nikita Jones to Antony Lee, her deputy head of customer service. She and Lee were having a follow-up discussion after the board meeting, where the chief executive officer (CEO) outlined the banks aggressive push toward rapid digitization of its retail banking division. The board and top management expected significant cost savings, better service quality, higher compliance, and easy scalability of its operations. However, Jones worried how the banks customers, many of them being wealthy baby boomers and Gen X, would respond. After the meeting, the CEO had sent an email to share his vision; it clearly shows his enthusiasm for this accelerated push. It included the following: Central for almost all businesses to survive is the digital and technological revolution we are all currently living through. I am convinced that the service sector is at an inflection point with regard to productivity gains and service industrialization, similar to the Industrial Revolution in manufacturing that started in the 18th century. Virtually all service sectors will be transformed by rapidly developing technologies that become better, smarter, smaller, and cheaper. This applies especially to technologies that are relevant in retail banking, such as AI, chatbots, analytics, machine learning, mobile technologies, apps, geo-tagging, biometrics, and text processing, speech processing, image processing, and so much more. In combination, these technologies and service innovations have the potential to dramatically improve the customer experience and productivity all at the same time. Furthermore, many of these technologies have almost zero incremental cost. For example, AI and virtual service robots (e.g., voice-based chatbots) require significant investments for their development, but then can be scaled. Serving more customers has almost zero incremental costs. Have a look at the case study of a leading bank that is already in the advanced stages of digitization and intelligent automation (Exhibit 1). This is where I envisage we will go, too. Thankfully, this bank is in a different geography and we are not competing with it! By going faster than our local competitors, we may have the opportunity to gain significant market share! Lets be proactive and make this our number one strategic direction. We want to become one of the worlds best digital banks taking full advantage of intelligent automation ... but of course, with a personal touch, where needed and where it adds real value! Jones shook her head and wondered, How can we develop an implementation strategy that will be embraced by our customers? Do we need to structure our implementation by types of services, customers, and profitability? What else do we need to worry about? Then Jones recalls the customer survey that a marketing agency had recently conducted. Jones and Lee looked through the findings of the focus groups and the representative quotes the research agency had pulled out that showed how customers might respond to chatbots and service robots: For certain questions, it is completely sufficient to talk to a robot. And I like the fact that a chatbot is available around the clock and can help directly. (Ava, 36 years, nurse) Its very evident when it comes to finances, were talking about confidential, private, and sensitive information. I want to speak to my personal bank advisor, who has known me for years. (William, 51 years, tax accountant) It doesnt matter whether Im talking to a robot or an employee. What matters to me is that someone takes care of my request quickly. For me, the only thing that counts is whether I get the credit or not. (Liam, 30 years, entrepreneur) As a loyal and good customer, I naturally expect a bit more service, starting with accessibility and that my requests are treated with priority. I dont want to have to talk to a robot every time. (Toni, 60 years, manager) Especially for complex investment decisions, robots can retrieve and analyze all relevant data much faster and better, and humans make mistakes. Therefore, I trust robots more than humans when things get complex. However, people can explain complicated financial products better and make me understand their relevance for my personal situation. Is there a way to have both? (Sophia, 43 years, doctor) When it comes to analyzing the behavior of global stock markets, I believe that only AI can do that well. Ok, I have to trust an unknown system, but a human wouldnt be able to do it better. We dont have the capacity for that. (Thomas, 48 years, IT specialist) The diversity of opinions these quotes reflect left an impression on Jones. She planned to set up a meeting soon with her customer service team to discuss how they might approach intelligent automation (IA), and importantly, mitigate potential negative customer responses. To improve customer experience and limit its losses due to card fraud, a leading bank decided to create a state-of-the-art machine learning-based program to identify fraudulent transactions automatically. This implementation increased the volume of fraud resolved by 30% in less than 4 months. However, its employee and customer experience deteriorated (see Stage 2 in Exhibit 2). To address this issue, the bank decided to take a more holistic approach. It requested support from a team in charge of IA at one of its subsidiaries. The first action from this team was to review and redesign not only the activity of fraud identification but also, more broadly, the end-to-end process with an emphasis on the customer and employee experience (see Stage 3 in Exhibit 2). While machine learning in Stage 2 automated only 20% of the process, the IA team succeeded in automating more than 80% in Stage 3. As a result, the customer and employee experience drastically improved. Most of the tedious tasks were now performed by technology. Overall, the bank increased the number of fraudulent transactions solved by 70% and generated more than $100 million in additional savings per year. Exhibit 1 Typical credit card fraud management process Exhibit 2 Using intelligent automation in credit card fraud processes

Q6. How can customers be enticed to try and ultimately routinely use these new delivery channels? Does the bank need to segment customers based on their ability and willingness to adopt these smart delivery channels? Does the profitability of customers play a role? (2+2+1 marks)

EXAMPLE OF USING INTELLIGENT AUTOMATION IN CREDIT CARD clients, we often blame our bank for not identifying these issues earlier and warning us. Also, even though losses tend to be insured, reimbursements take months. And before that, customers have to go through several tedious administrative tasks, including filling in forms, FRAUD MANAGEMENT providing evidence, and calling (see Exhibit 1), Credit card transaction fraud is a critical topic. It caused annual losses of some $28 billion and is a source of frustration for customers, retailers, and financial institutions. It is so prevalent that it probably happened at least once to most credit card holders. As Typical credit card fraud management process Credit card transaction Potential fraud is identified from transactions analysis A B Fraud score No Fraud Potential fraud is investigated Fraud confirmed D Remediation actions: (C) Q Contact client Block credit card Collect evidence Connect with insurance Monitor the process Leveraging Intelligent Automation to enhance a bank fraud management system Stages in the Before New system 1 transformation 2 leveraging machine transformation New system leveraging Intelligent Automation (incl. machine learning) journey (manual) learning (only) Timeline Before Jun 2019 Jun to Dec 2019 Description Transactions were checked of the key process activities manually on a sample basis. Investigations, All transactions were checked (no more sampling). The system could identify potentially fraudulent transactions in just a few seconds by analyzing client transactions, as well as their behavioral and demographic data. collection of evidence, and credit card blocking were performed manually by the team. Communication (with clients and insurance companies) was performed manually by the team. 2 Investigations, collection of evidence, and credit card blocking were still performed manually by the team. 3Communication (with clients and insurance companies) was still performed manually by the team. Medium Low The process was very manual, and repetitive. The team faced difficulties in coping with the workload, which increased drastically as the system was identifying more potentially fraudulent transactions. In addition, the bank employees complained about their work becoming more tedious, repetitive, and less fulfilling. While the fraud team used to leverage its intuition, strategy, and analysis to identify and investigate fraud, this role now taken by the system. The team's new role was primarily to focus on collecting, indexing, and archiving the fraud evidence. 2/5 Rationale: the high workload decreased the team's responsiveness in answering clients' questions and the time it could dedicate to client relationships. Morale of the bank's fraud investigation team Client satisfaction (rated on a scale from 1 to 5, 5 being very satisfied) 3/5 Jan 2020 onwards The same machine learning- based system was used. Investigations and collection of evidence were performed using an intelligent workflow. Credit card blocking actions were automated using robotic process automation All event-triggered communications were automated. The system proactively provided clients with early warnings of potential fraud, enabling them to take prompt and easy actions. Clients and insurers had access to a 24/7 intelligent chatbot to answer their questions and update them on the status of the fraud resolution process. High The team's workload decreased, and the work became more fulfilling as most of the repetitive and tedious activities were performed by technology. As an outcome, the team could focus on more value-adding activities, like building relationships with clients, managing the exceptions (e.g.. investigating the most complex cases) and monitoring the overall process to anticipate any issues. The team was also able to focus on constantly improving the new system, increasing its accuracy levels, and extending its scope to manage additional payment means like cheques and bank transfers. 4/5 Rationale: early communication on potential fraud identification, 24/7 support, reduction by half of the end-to-end process time (from the identification of the fraud to the reimbursement by the insurance)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts