Question: See image Consider an asset with value Sm at time-step mot and expected value Sm+1 under a continuous random walk model, E[sm+1 sm] = S'p(sm,

See image

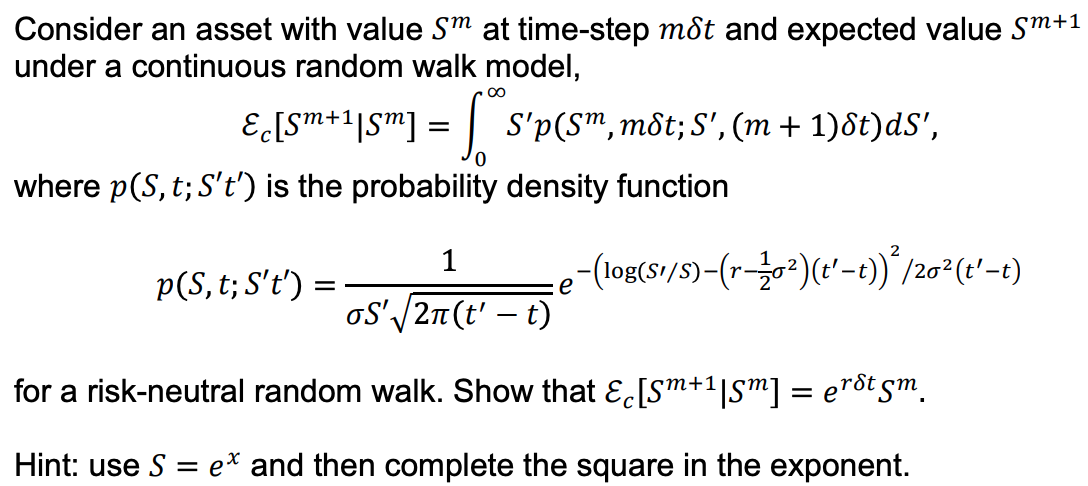

Consider an asset with value Sm at time-step mot and expected value Sm+1 under a continuous random walk model, E[sm+1 sm] = S'p(sm, mot; S', (m + 1)St)ds', 0 where p(S, t; S't') is the probability density function p(S, t; S't') = e -(log(S,/s)-(7-202)(t'-t)) /202(t' -t) oS' \\2n(t' - t) for a risk-neutral random walk. Show that E [Sm+1|sm] = erstym. Hint: use S = ex and then complete the square in the exponent

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock