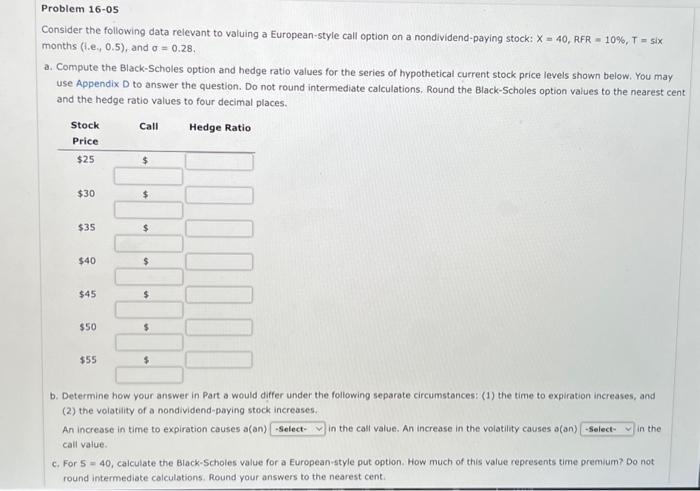

Question: selects are increase or decrease Consider the following data relevant to valuing a European-style call option on a nondividend-paying stock: X=40,RFR=10%,T=six months ( 1.e,,0.5 ),

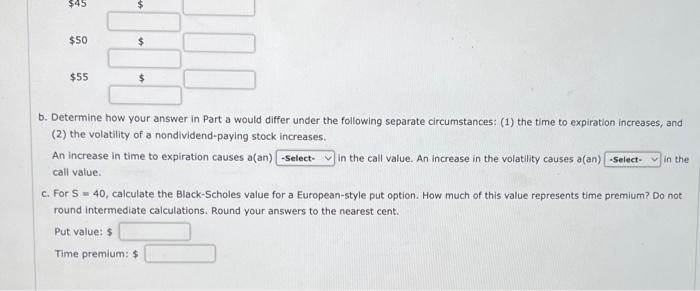

Consider the following data relevant to valuing a European-style call option on a nondividend-paying stock: X=40,RFR=10%,T=six months ( 1.e,,0.5 ), and =0.28. use Appendix D to answer the question. Do not round intermediate calculations, Round the Black-Scholes option values to the nearest cen and the hedge ratio values to four decimal places. b. Determine how your answer in Part a would differ under the following separate circumstances: (1) the time to expiration increases, and (2) the volatility of a nondividend-paying stock increases. An increase in time to expiration causes a(an) in the call value. An increase in the volatility causes a(an) in the call value. c. For 5=40, calculate the Black-Scholes value for a European-style put option. How much of this value represents time premium? Do not round intermediate calculations. Round your answers to the nearest cent. b. Determine how your answer in Part a would differ under the following separate circumstances: (1) the time to expiration increases, and (2) the volatility of a nondividend-paying stock increases. An increase in time to expiration causes a(an) in the call value. An increase in the volatility causes a(an) call value. c. For S=40, calculate the Black-Scholes value for a European-style put option. How much of this value represents time premium? Do not round intermediate calculations. Round your answers to the nearest cent. Put value: $ Time premium: $

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts