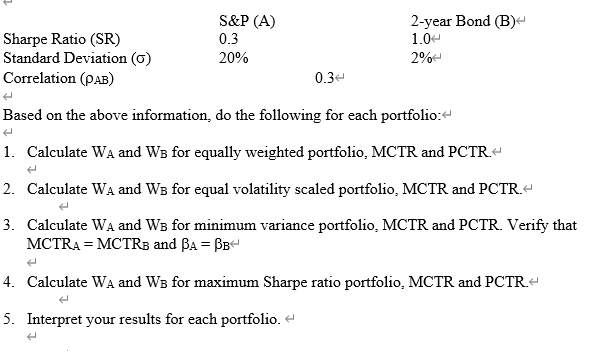

Question: Sharpe Ratio (SR) Standard Deviation (0) Correlation (PAB) S&P (A) 0.3 20% 2-year Bond (B) 1.04 2% 0.34 Based on the above information, do the

Sharpe Ratio (SR) Standard Deviation (0) Correlation (PAB) S&P (A) 0.3 20% 2-year Bond (B) 1.04 2% 0.34 Based on the above information, do the following for each portfolio: 1. Calculate WA and W3 for equally weighted portfolio. MCTR and PCTR- 2. Calculate WA and W3 for equal volatility scaled portfolio, MCTR and PCTR. 3. Calculate WA and W8 for minimum variance portfolio, MCTR and PCTR. Verify that MCTRA = MCTRB and BA = BB 4. Calculate WA and WB for maximum Sharpe ratio portfolio, MCTR and PCTR 5. Interpret your results for each portfolio. el Sharpe Ratio (SR) Standard Deviation (0) Correlation (PAB) S&P (A) 0.3 20% 2-year Bond (B) 1.04 2% 0.34 Based on the above information, do the following for each portfolio: 1. Calculate WA and W3 for equally weighted portfolio. MCTR and PCTR- 2. Calculate WA and W3 for equal volatility scaled portfolio, MCTR and PCTR. 3. Calculate WA and W8 for minimum variance portfolio, MCTR and PCTR. Verify that MCTRA = MCTRB and BA = BB 4. Calculate WA and WB for maximum Sharpe ratio portfolio, MCTR and PCTR 5. Interpret your results for each portfolio. el

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts