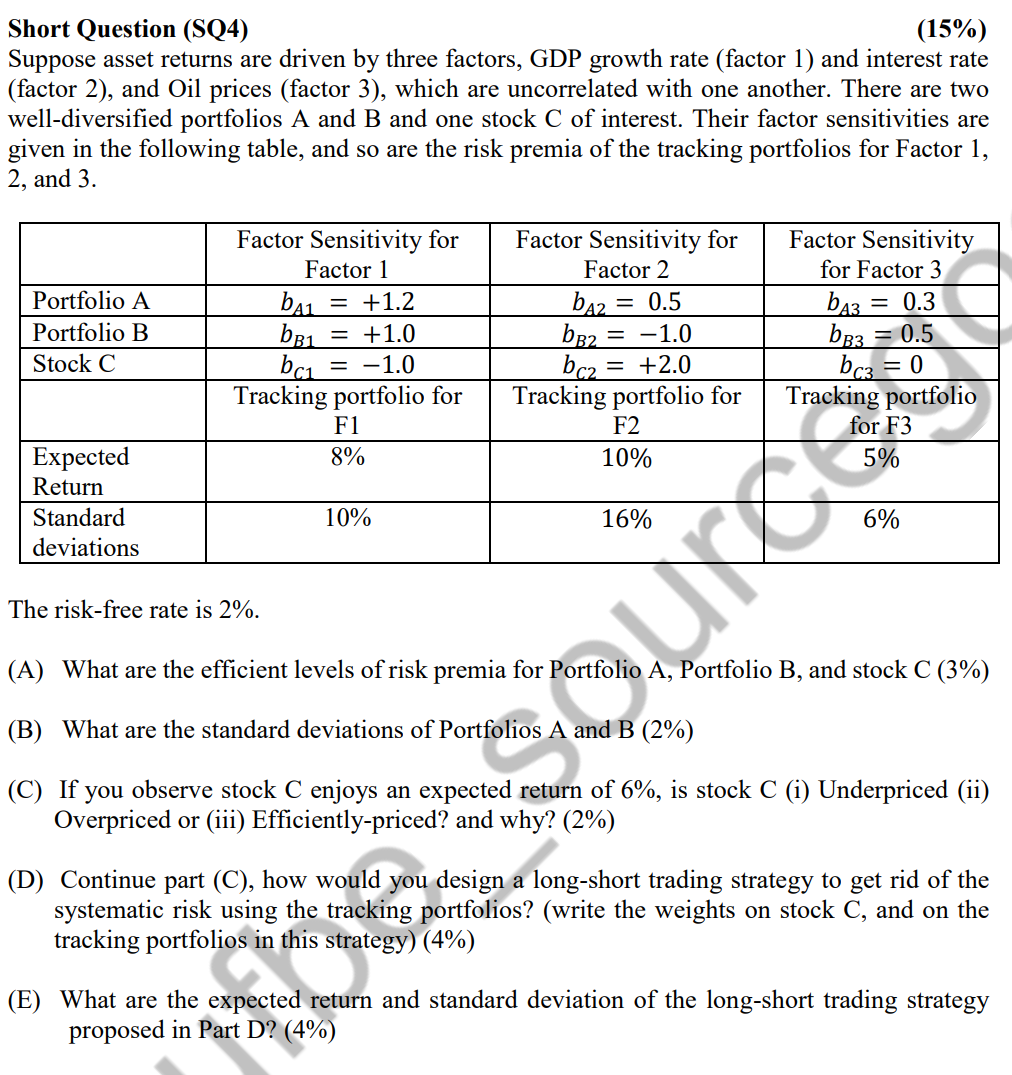

Question: Short Question (SQ4) (15%) Suppose asset returns are driven by three factors, GDP growth rate (factor 1) and interest rate (factor 2), and Oil prices

Short Question (SQ4) (15%) Suppose asset returns are driven by three factors, GDP growth rate (factor 1) and interest rate (factor 2), and Oil prices (factor 3), which are uncorrelated with one another. There are two well-diversified portfolios A and B and one stock C of interest. Their factor sensitivities are given in the following table, and so are the risk premia of the tracking portfolios for Factor 1, 2 , and 3 . The risk-free rate is 2%. (A) What are the efficient levels of risk premia for Portfolio A, Portfolio B, and stock C (3\%) (B) What are the standard deviations of Portfolios A and B (2\%) (C) If you observe stock C enjoys an expected return of 6\%, is stock C (i) Underpriced (ii) Overpriced or (iii) Efficiently-priced? and why? (2\%) (D) Continue part (C), how would you design a long-short trading strategy to get rid of the systematic risk using the tracking portfolios? (write the weights on stock C, and on the tracking portfolios in this strategy) (4\%) (E) What are the expected return and standard deviation of the long-short trading strategy proposed in Part D? (4\%)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts