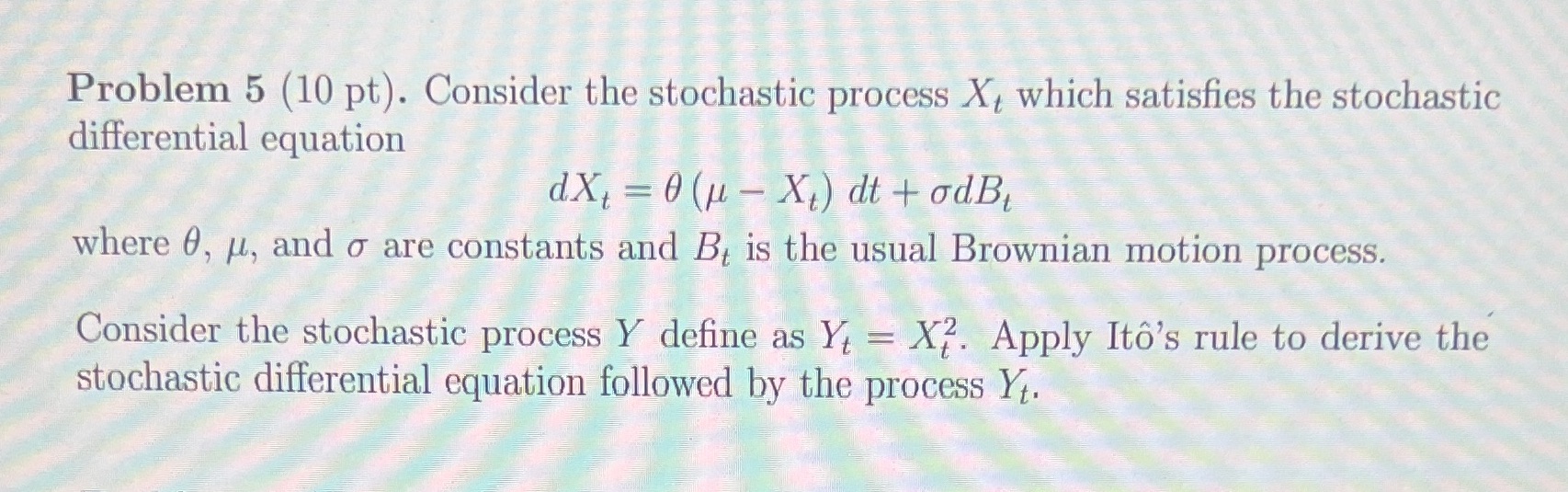

Question: Show all work Problem 5 (10 pt). Consider the stochastic process Xt which satisfies the stochastic differential equation dX1 = 0 (u - X.) dt

Show all work

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock