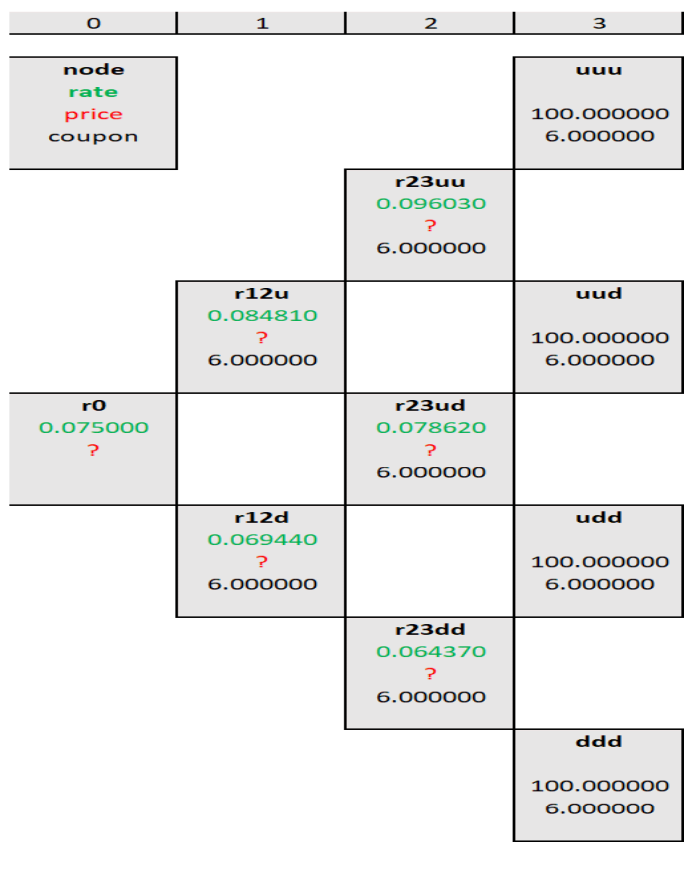

Question: Shown below is a binomial tree for a 6% coupon bond based on an interest rate volatility of 10%. The up moves and down moves

Shown below is a binomial tree for a 6% coupon bond based on an interest rate volatility of 10%. The up moves and down moves have equal probability.

Compute the price of the bond and present your answer by showing the binomial tree above with the required prices of the bond at each node

(b) Suppose the bond above is putable at par from Year 1. Compute the value of the bond at time 0.

(c) Suppose the interest rate volatility increases. Appraise how it affects the value of the putable bond in Part (b).

node rate price coupon ro 0.075000 ? 1 2 3 r12u 0.084810 ? 6.000000 r12d 0.069440 ? 6.000000 r23uu 0.096030 ? 6.000000 r23ud 0.078620 ? 6.000000 uuu 100.000000 6.000000 uud 100.000000 6.000000 udd 100.000000 6.000000 r23dd 0.064370 ? 6.000000 ddd 100.000000 6.000000

Step by Step Solution

There are 3 Steps involved in it

To compute the price of the bond we start at the final nodes and work our way back up the tree applying the formula Price Coupon Payment Price at the ... View full answer

Get step-by-step solutions from verified subject matter experts