Question: SOLVE 7.3 Please. Exercise 7.2 The prices of a certain security follow a geometric Brownian motion with parameters u = .12 and o = .24.

SOLVE 7.3 Please.

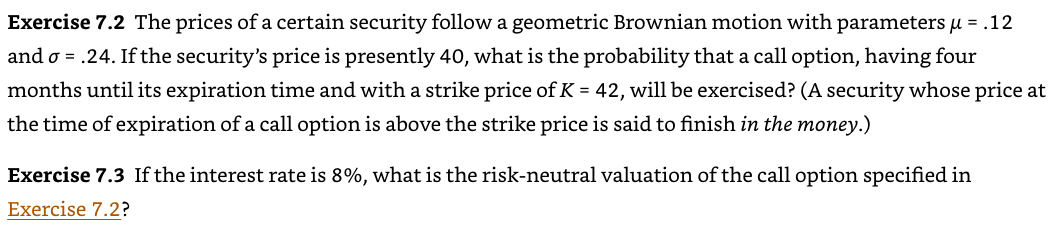

Exercise 7.2 The prices of a certain security follow a geometric Brownian motion with parameters u = .12 and o = .24. If the security's price is presently 40, what is the probability that a call option, having four months until its expiration time and with a strike price of K = 42, will be exercised? (A security whose price at the time of expiration of a call option is above the strike price is said to finish in the money.) Exercise 7.3 If the interest rate is 8%, what is the risk-neutral valuation of the call option specified in Exercise 7.2? Exercise 7.2 The prices of a certain security follow a geometric Brownian motion with parameters u = .12 and o = .24. If the security's price is presently 40, what is the probability that a call option, having four months until its expiration time and with a strike price of K = 42, will be exercised? (A security whose price at the time of expiration of a call option is above the strike price is said to finish in the money.) Exercise 7.3 If the interest rate is 8%, what is the risk-neutral valuation of the call option specified in Exercise 7.2

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts